The latest Q3 2025 provisional YEONGHWA METAL CO.,LTD earnings report presents a complex picture for investors. On one hand, a decline in revenue signals persistent headwinds from a volatile automotive market. On the other, a resilient defense of operating profit and net income suggests strong internal management and cost controls. This duality raises critical questions: Is this a sign of sustainable profitability, or a temporary reprieve before further downturns?

This comprehensive analysis will dissect the YEONGHWA METAL CO.,LTD (012280) financial results, evaluate its underlying corporate fundamentals, and assess the broader market environment. We aim to provide investors with a clear, actionable perspective on the challenges and opportunities facing the company and what it could mean for the YEONGHWA METAL stock price.

Q3 2025 YEONGHWA METAL CO.,LTD Earnings at a Glance

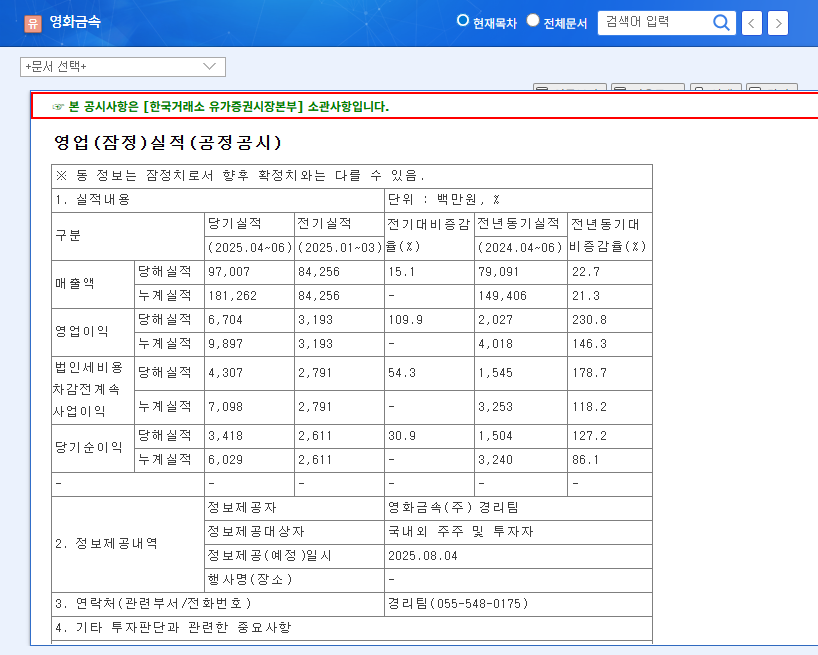

On November 10, 2025, YEONGHWA METAL CO.,LTD released its provisional earnings for the third quarter. The report, detailed in the company’s Official Disclosure (DART), revealed the following key metrics:

Key Financial Figures (Q3 2025):

• Revenue: KRW 85.4 billion (a 12.0% decrease from Q2)

• Operating Profit: KRW 3.2 billion (a 52.2% decrease from Q2, but stable vs. Q1)

• Net Income: KRW 2.8 billion (a 17.6% decrease from Q2, but slightly up from Q1)

While the quarter-over-quarter declines in revenue and operating profit are notable, the ability to maintain profitability at levels comparable to the first quarter, despite lower sales, is the central theme of this report. This performance indicates a robust effort to manage the bottom line amidst external pressures.

Why Did It Happen? Analyzing the Core Drivers

The Revenue Headwind: Automotive Industry & Macro-Economic Pressure

The primary cause for the 12.0% sequential revenue decline is the persistent global economic slowdown, which has directly impacted the automotive sector. As a key supplier of cast metal components, YEONGHWA METAL’s fortunes are intrinsically linked to the production volumes and sales of major vehicle manufacturers. With consumer demand softening and supply chains still normalizing, the entire industry is facing a period of reduced activity, directly impacting the company’s top-line growth.

The Profitability Shield: Cost Management and Efficiency Gains

Despite falling sales, the company’s ability to defend its profitability is commendable. This resilience is attributed to several key factors first highlighted in its H1 2025 report, which continued to bear fruit in Q3:

- •Aggressive Cost Reduction: Proactive measures to streamline operations and reduce overhead have played a crucial role.

- •Improved Production Efficiency: Enhancements in manufacturing processes have likely lowered the cost per unit, protecting margins even on lower volumes.

- •Favorable Raw Material Prices: A decline in the cost of key raw materials, such as scrap iron, has provided a significant tailwind, directly boosting the gross profit margin.

Financial Health and Future Outlook

Balance Sheet Under Scrutiny

While profitability management is a positive, the balance sheet reveals areas that require careful monitoring. As of mid-2025, total assets increased, but so did accounts receivable and inventories. This could indicate slowing sales cycles or potential issues with collecting payments. Concurrently, total liabilities and borrowings have risen, pushing the debt-to-equity ratio to 203.88%. This elevated leverage makes the company more vulnerable to interest rate fluctuations and economic shocks, making disciplined financial management a critical priority moving forward.

Pivoting to New Growth Engines?

Looking to the future, YEONGHWA METAL has added new business objectives to its articles of incorporation, including ventures into secondary batteries, semiconductors, and software. This signals a strategic intent to diversify away from its heavy reliance on the traditional automotive industry. However, these initiatives are still in their infancy with no specific business activities commenced. The market will be watching closely for concrete investment plans and tangible progress in these high-growth sectors, which could serve as powerful long-term catalysts for the YEONGHWA METAL stock.

Investor Action Plan & Final Verdict

The YEONGHWA METAL CO.,LTD earnings report for Q3 2025 reinforces a ‘wait-and-see’ approach. The company is successfully navigating a tough market but faces clear risks.

Investment Opinion: Neutral

At present, there is no compelling catalyst to justify a strong buy or sell rating. The positive operational management is balanced by negative external pressures and financial leverage. Therefore, our investment opinion remains ‘Neutral’. A reassessment will be warranted upon the release of the full 2025 annual report and clearer signals regarding the automotive market’s recovery and the company’s new business ventures.

Key Monitoring Points for Investors

Investors should keep a close watch on the following developments, which will be critical in shaping the future of YEONGHWA METAL (012280):

- •Revenue Trajectory: Is the Q3 decline a blip or the start of a sustained downturn? Q4 results will be crucial.

- •New Business Materialization: Any announcement of capital expenditure, partnerships, or initial contracts in the battery or semiconductor spaces would be a significant positive catalyst. For more on this, see our deep dive into the secondary battery market.

- •Financial Health Indicators: Monitor changes in the debt-to-equity ratio and levels of accounts receivable in the upcoming reports. Improvement here would reduce risk.

- •Macro-Economic Factors: Keep an eye on global automotive sales data, raw material price trends, and currency exchange rate volatility (KRW/USD).