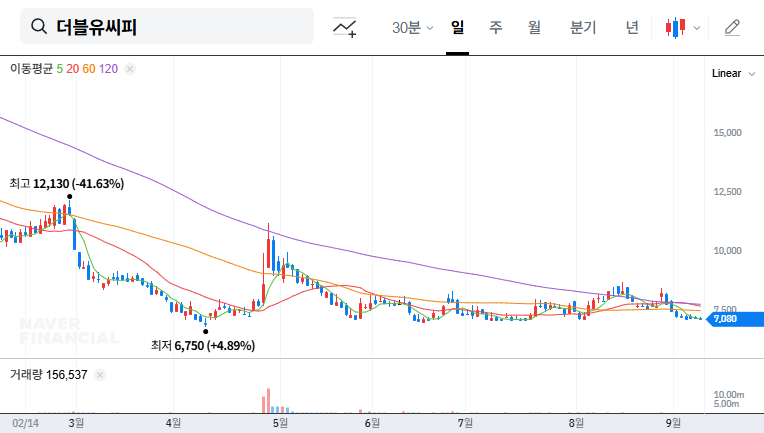

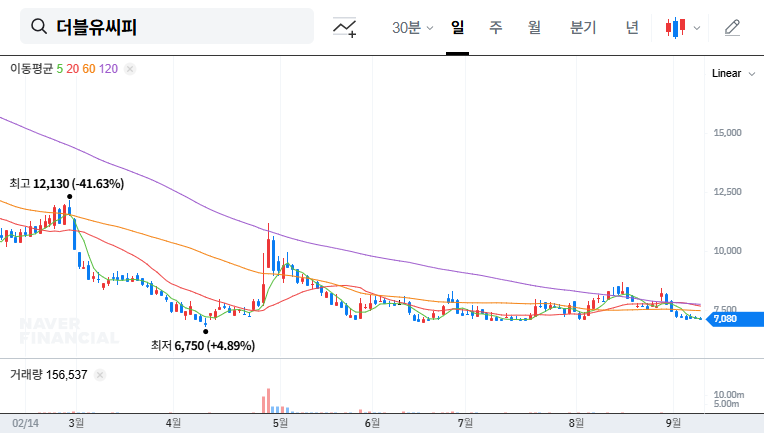

The recent Q3 2025 earnings report for W-SCOPE CHUNGJU PLANT has cast a significant shadow over the WCP stock outlook, sending ripples of concern through the investment community. With sales figures falling drastically short of estimates and operating losses widening, stakeholders are questioning the company’s path forward. Can WCP navigate these turbulent waters and capitalize on its long-term growth drivers? This in-depth WCP stock analysis dissects the disappointing quarterly results, evaluates the underlying fundamentals, and outlines a prudent investment strategy for the challenging period ahead.

WCP Q3 2025 Earnings: A Disappointing Reality

W-SCOPE CHUNGJU PLANT (WCP) officially disclosed its provisional earnings for the third quarter of 2025, confirming performance that was significantly below market consensus. This report, available via the Official Disclosure (DART), unfortunately extends the trend of sluggish performance seen since the second half of 2024, amplifying investor anxiety about the company’s trajectory and the immediate future of WCP stock.

Unpacking the Underwhelming Q3 Financials

The numbers paint a stark picture of the current operational challenges:

- •Revenue: KRW 29.1 billion, a significant 24.0% miss compared to the KRW 38.4 billion estimate.

- •Operating Profit: A loss of KRW -31.0 billion, expanding 59.0% beyond the anticipated KRW -19.5 billion loss.

- •Net Profit: A continued loss, recorded at KRW -46.1 billion.

This sharp quarterly revenue decline and the deepening operating losses are direct results of a dual-pronged problem: a widespread slowdown in the secondary battery market combined with WCP’s specific business and financial vulnerabilities.

Core Challenges vs. Long-Term Potential

To formulate a sound WCP investment strategy, investors must weigh the severe short-term headwinds against the company’s foundational strengths and long-term market opportunities.

Negative Headwinds Impacting WCP Stock

- •EV Market ‘Chasm’: The global EV market is experiencing a temporary but impactful slowdown, often referred to as ‘crossing the chasm,’ where growth stalls between early adopters and the mass market. This directly curtails demand for WCP’s battery separators.

- •High Fixed Costs: Despite falling revenue, the company’s high fixed costs associated with large-scale manufacturing facilities have exacerbated operating losses, creating a significant barrier to profitability.

- •Policy & Financial Risks: Uncertainty surrounding U.S. policies like the IRA Act could hinder North American expansion, while significant foreign currency liabilities (USD 3.77B, EUR 0.875B) expose the company to exchange rate volatility.

Positive Drivers for Future Growth

Despite the gloom, WCP’s long-term value proposition remains intact, anchored by several key strengths.

- •Inevitable EV Expansion: The long-term trend is undeniable. Projections for global EV market growth of ~20% in 2025 will fundamentally drive demand for essential components like battery separators.

- •Technological Edge: WCP’s proprietary 5.5m wide-format production and low trimming ratio are significant competitive advantages, enabling higher efficiency and quality for top-tier battery manufacturers.

- •Strategic European Entry: The planned Hungarian subsidiary is a critical move to capture Europe’s burgeoning EV market and establish a local supply chain, which could be a major catalyst for future W-SCOPE CHUNGJU PLANT earnings.

Investment Opinion and Go-Forward Strategy

The Q3 2025 earnings release has undeniably re-calibrated the short-term outlook for WCP stock. The severity of the revenue miss and expanded losses makes a bullish stance untenable at this time.

Given the current operational and financial pressures, our official investment opinion on W-SCOPE CHUNGJU PLANT (WCP) is a ‘Cautious Neutral.’ A wait-and-see approach is recommended until clear signs of a turnaround emerge.

Key Monitoring Points for Investors

Investors considering or holding WCP stock should adopt a vigilant monitoring strategy focused on these catalysts:

- •Performance Turnaround Signals: Scrutinize Q4 2025 and H1 2026 reports for any stabilization in revenue and a narrowing of losses. The successful ramp-up of the Hungarian plant and new customer supply agreements are critical proof points.

- •Macro & Industry Shifts: Keep a close watch on the recovery pace of the global EV market. For more context, you can read our guide on understanding the secondary battery market. Policy changes and raw material price trends are also key risk factors.

- •Financial Health Metrics: Monitor the company’s debt-to-equity ratio (currently 109.5%) and any new initiatives aimed at deleveraging or improving its financial structure.

Frequently Asked Questions (FAQ)

What were WCP’s provisional earnings for Q3 2025?

For Q3 2025, WCP reported revenue of KRW 29.1 billion, an operating loss of KRW -31.0 billion, and a net loss of KRW -46.1 billion. These results were significantly below market expectations.

What are the main reasons for WCP’s poor performance?

The underperformance is primarily due to a slowdown in global EV demand, a high fixed-cost structure that magnifies losses during revenue downturns, and general weakness in the secondary battery sector.

Does WCP still have long-term growth potential?

Yes. Despite short-term pain, its long-term drivers include the continued global adoption of EVs, superior production technology, strategic expansion into the European market, and the potential to apply its technology to new industries.

What is the current investment recommendation for WCP stock?

The current investment opinion for WCP stock is ‘Cautious Neutral’. This advises investors to exercise patience and wait for concrete evidence of a performance and financial turnaround before committing new capital.