The AMOREPACIFIC Value Enhancement Plan for 2025 has been presented as a bold roadmap to future growth, expanded shareholder returns, and improved governance. While the company paints a compelling picture, a closer look at its financial forecasts reveals a stark and worrying contradiction. With projected annual earnings on a sharp decline, despite positive first-half results, investors are left to question the plan’s feasibility. This comprehensive AMOREPACIFIC 2025 analysis will dissect the promises, scrutinize the financial data, and outline a prudent AMOREPACIFIC investment strategy to navigate the uncertainty ahead.

Deconstructing the Value Enhancement Plan

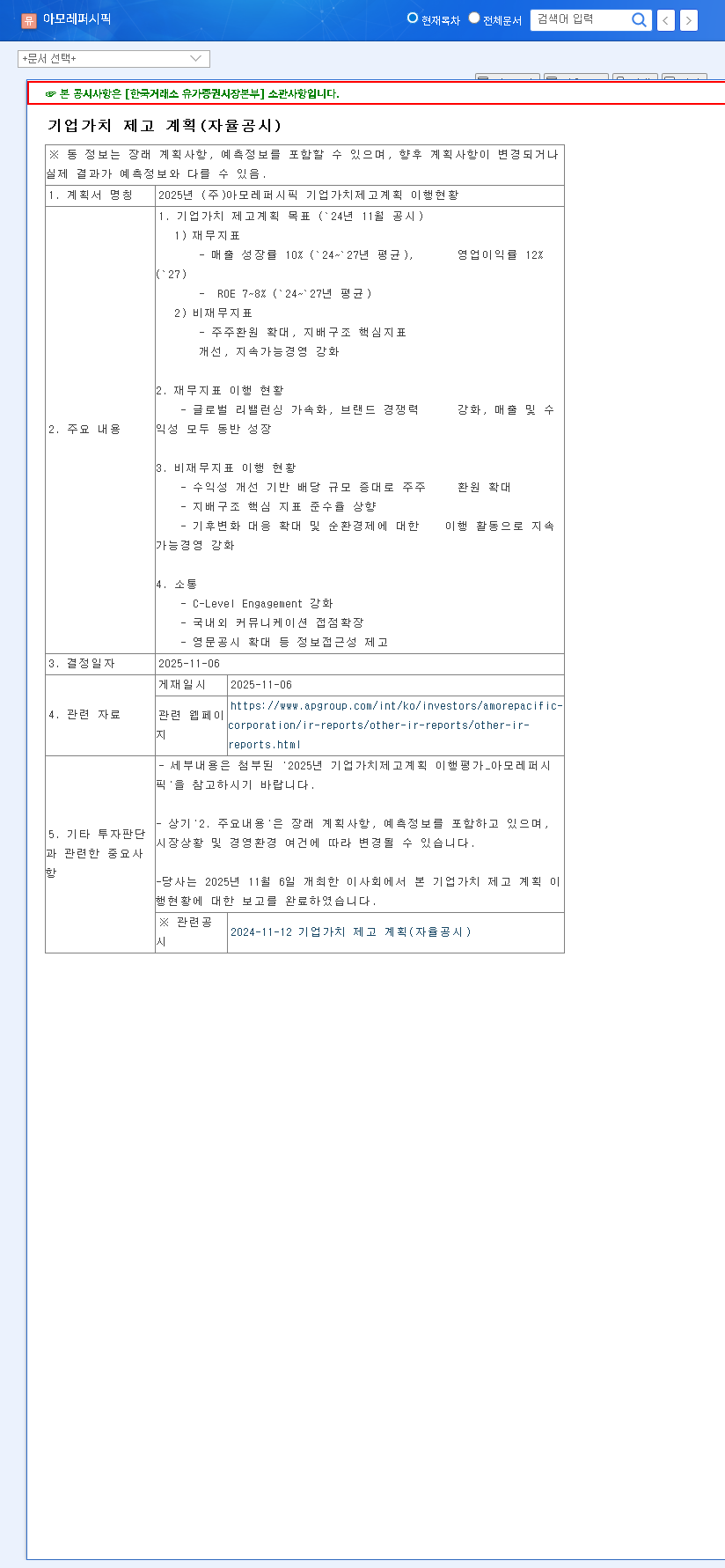

First unveiled in late 2024, AMOREPACIFIC’s plan is built on ambitious financial and non-financial pillars. The company is committing to tangible targets designed to bolster corporate value and investor confidence. You can view the complete details in the Official Disclosure filed with DART. The core objectives include:

- •Financial Targets: Achieving 10% annual revenue growth, a 12% operating profit margin, and a 7-8% Return on Equity (ROE).

- •Shareholder Returns: Expanding returns through mechanisms like increased dividend payouts.

- •Governance & ESG: Improving compliance with core governance indicators and strengthening sustainable management through climate change and circular economy initiatives.

- •Global Growth: Accelerating global rebalancing with a focus on brand competitiveness in new markets.

On paper, these initiatives signal a strong commitment to long-term growth and transparent communication. However, the plan’s success is entirely dependent on the company’s underlying financial health, which is where significant concerns arise.

A Tale of Two Halves: 2025 Financial Performance

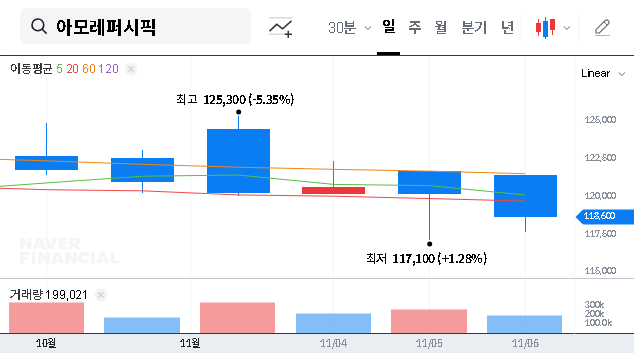

The primary source of confusion and risk for investors is the dramatic disconnect between the company’s reported first-half performance and its grim full-year forecast.

Positive First-Half Momentum

AMOREPACIFIC’s Q2 2025 report showed impressive growth, with consolidated revenue rising 14.1% and operating profit soaring by 149.1%. This was fueled by strong overseas expansion in the Americas and EMEA, coupled with the successful integration of the acquired brand COSRX. Core brands like Sulwhasoo and Laneige also demonstrated robust performance.

An Alarming Full-Year Forecast

Despite the positive start, long-term projections tell a different story. Financial estimates indicate a continuous decline in revenue since 2022 and, most critically, a projected operating loss for the full year of 2025. This downturn points to severe challenges that could intensify in the second half of the year, including:

- •Sluggish China Market: The slow recovery in China, a historically vital market, highlights vulnerability to intense local competition and shifting consumer preferences.

- •Financial Strain: The acquisition of COSRX has increased the debt-to-equity ratio to 114.65%, requiring meticulous financial management to ensure stability.

- •Economic Volatility: Global uncertainties, including fluctuating exchange rates, could impact profitability despite some potential gains from a weaker Korean Won. For more on market trends, see this global economic outlook report.

The core issue is the severe discrepancy between the company’s ambitious Value Enhancement Plan and the projected deterioration in its financial performance. The market will ultimately prioritize actual results over stated intentions.

Crafting a Prudent AMOREPACIFIC Investment Strategy

Given the conflicting signals, a cautious and analytical approach is essential. The disclosure of the AMOREPACIFIC Value Enhancement Plan is a positive step in shareholder communication, but it cannot mask the underlying financial headwinds.

Key Recommendations for Investors:

- •Adopt a Cautious Stance: Aggressive investment at this time is inadvisable. The risk of earnings deterioration in the second half of 2025 is significant and must be carefully weighed.

- •Monitor Key Performance Indicators: Closely track future quarterly earnings reports. Pay special attention to the pace of recovery in China, concrete growth figures from other overseas markets, and the company’s cost management efficiency.

- •Re-evaluate Valuation: The current market capitalization may not accurately reflect the anticipated decline in earnings. As new data becomes available, it will be crucial to reassess if the stock’s valuation remains attractive. To learn more, read our guide on analyzing beauty stock fundamentals.

In conclusion, while AMOREPACIFIC is making efforts to enhance corporate value, it faces a fundamental challenge in bridging the gap between its strategic goals and its current financial trajectory. Investment decisions should be deferred until there is concrete evidence that the company can navigate its business slump and effectively execute its ambitious plan. The focus must remain on performance, not promises.

Disclaimer: This analysis is for informational purposes only and is based on publicly available data. It does not constitute investment advice. All investment decisions should be made based on your own research and judgment.