The latest financial report from Techwing, Inc., a key player in the semiconductor inspection equipment sector, has sent ripples of concern through the market. The highly anticipated Techwing Q3 2025 earnings report revealed a significant shortfall against market expectations, raising critical questions about the company’s current trajectory and future prospects. Is this a temporary dip in a volatile market, or does it signal deeper challenges ahead? This comprehensive analysis will dissect the official figures, explore the potential impact on Techwing’s stock, and outline strategic considerations for investors.

Decoding the Techwing Q3 2025 Earnings Report

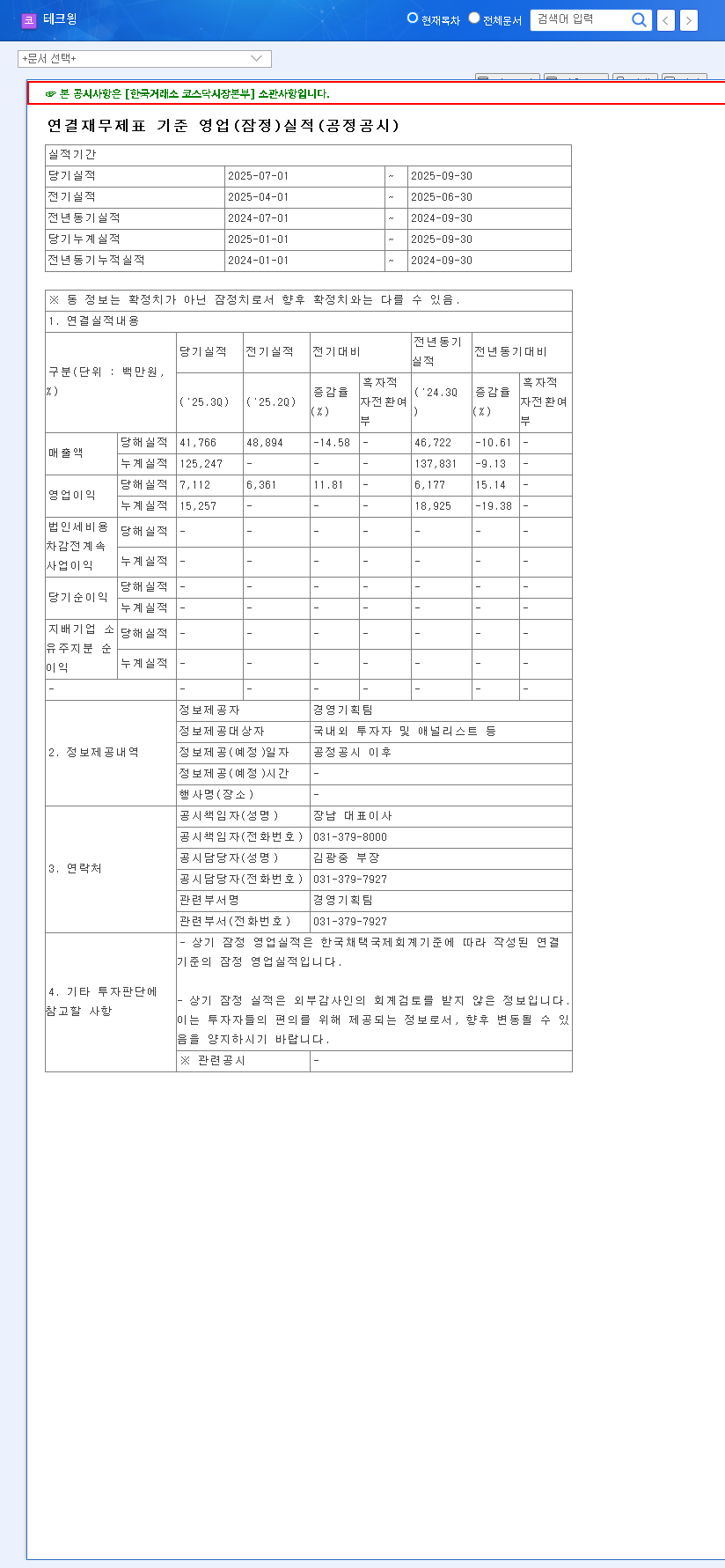

On October 21, 2025, Techwing released its provisional consolidated operating results, which immediately caught the attention of analysts and investors. The numbers, detailed in the company’s Official Disclosure (Source: DART), paint a picture of underperformance that cannot be ignored. Let’s break down the key metrics that fell short.

A Stark Miss on Key Financials

The provisional Q3 results were substantially below the consensus estimates, signaling issues with both top-line growth and operational efficiency. The deviation from projections was significant:

- •Revenue: Reported at KRW 41.8 billion, a 31.0% miss compared to the KRW 60.7 billion estimate.

- •Operating Profit: Came in at KRW 7.1 billion, a staggering 36.0% below the KRW 11.1 billion forecast.

This dual miss suggests that the company is facing not only challenges in securing sales but also mounting pressure on its profitability. Such a performance often triggers a re-evaluation of a company’s standing within the competitive semiconductor equipment market.

Historical Context: A Pattern of Volatility

A single quarter’s performance rarely tells the whole story. However, examining Techwing’s results over the past year reveals a concerning pattern of instability. After a weak start in Q1 2025, the company showed signs of a rebound in Q2, only to see revenue and profit decline again in Q3. This yo-yo effect points to a business model that is highly sensitive to external market dynamics, such as fluctuating memory chip prices and global macroeconomic headwinds. This lack of consistent, predictable growth is a major red flag for long-term investors seeking stability. A thorough Techwing stock analysis must account for this inherent volatility.

The core challenge for Techwing is to demonstrate whether this Q3 slump is an anomaly or the new normal. The market is now looking for a clear path back to sustainable growth and profitability.

Implications for Techwing Stock and Investment Strategy

The disappointing Techwing Q3 2025 earnings are almost certain to have tangible consequences for its stock price and overall market perception. Investors must prepare for potential short-term turbulence while critically assessing the company’s long-term value proposition.

Short-Term: Expect Increased Volatility

In the immediate aftermath, expect downward pressure on Techwing’s stock. The significant miss will likely trigger sell-offs from institutional and retail investors alike. Increased stock price volatility is a given as the market digests this negative news. Short-term traders may exploit this volatility, but long-term investors should resist making knee-jerk decisions.

Long-Term: Structural Concerns Emerge

The most critical question is whether this underperformance stems from structural problems. Are competitors gaining market share? Is there a fundamental slowdown in demand for Techwing’s specific product lines? According to market reports from sources like Reuters, the entire semiconductor sector is facing cyclical challenges, but a miss of this magnitude could suggest company-specific issues. A sound Techwing investment strategy requires separating industry-wide trends from internal weaknesses.

Strategic Actions for Stakeholders

In light of these results, both investors and the company’s management must adopt a prudent and strategic approach to navigate the path forward.

Recommendations for Investors

- •Exercise Caution: Avoid hasty buying or selling. A ‘wait-and-see’ approach is advisable until management provides a clear explanation and recovery plan.

- •Conduct Deeper Research: Look beyond the headline numbers. Analyze competitor performance, industry forecasts, and upcoming product cycles for Techwing.

- •Monitor Communications: Pay close attention to the company’s upcoming earnings call and any subsequent press releases for insights into the root causes of the miss.

Imperatives for Techwing’s Management

- •Transparent Communication: The company must proactively and transparently communicate the reasons for the shortfall to rebuild investor confidence.

- •Present a Clear Recovery Plan: Articulating a concrete, actionable plan to address the performance issues is crucial for stabilizing the stock and reassuring the market.

In conclusion, the Techwing Q3 2025 earnings serve as a critical wake-up call. While the results are undoubtedly disappointing, they also present an opportunity for a strategic reset. The company’s next moves will be pivotal in determining whether this quarter was a stumble or the beginning of a fall.