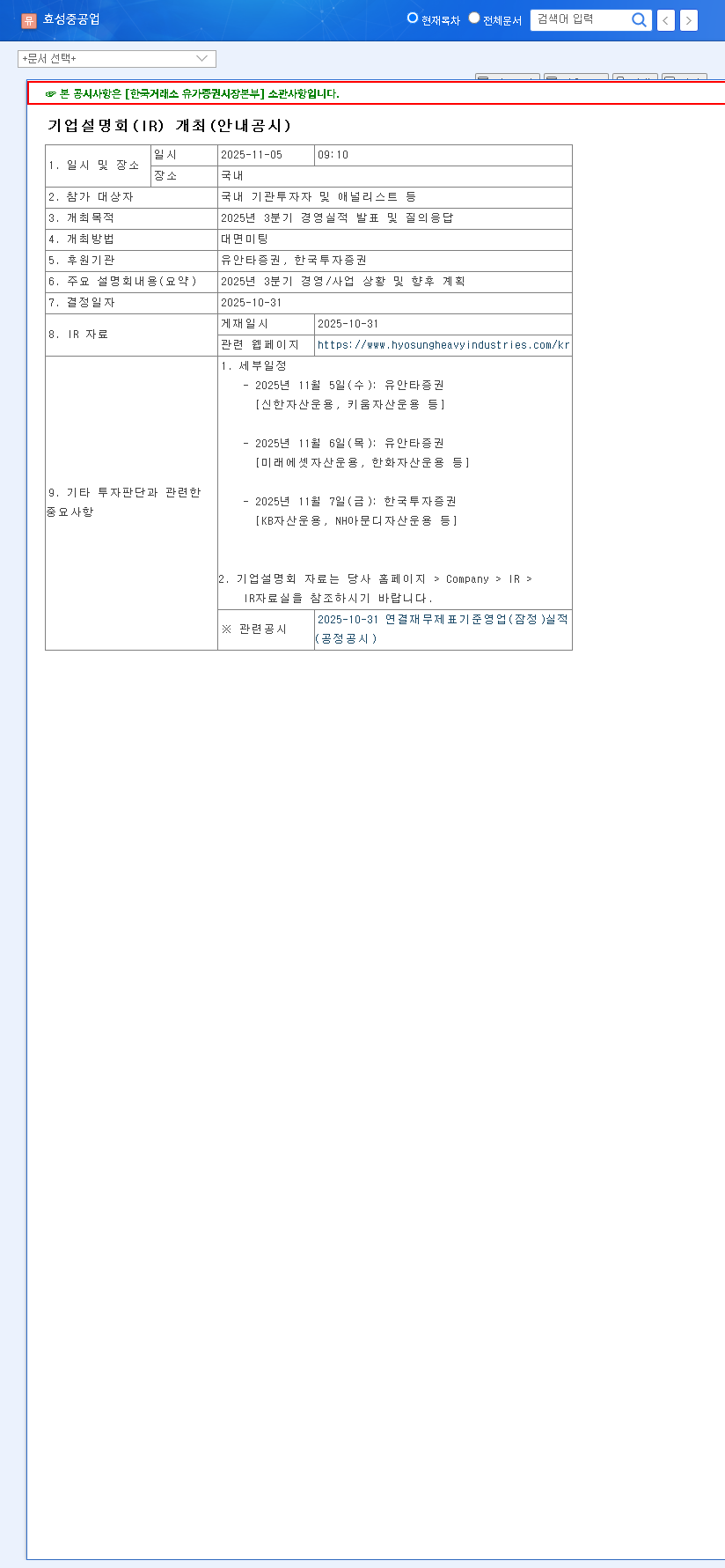

The upcoming Hyosung Heavy Industries Investor Relations (IR) briefing is poised to be a watershed moment for the company and its stakeholders. Scheduled for November 13, 2025, this event comes at a critical juncture, with the industrial giant navigating severe financial headwinds amidst a challenging macroeconomic landscape. For investors, this isn’t just a standard corporate update; it’s a crucial opportunity to gauge whether the company is on the brink of a rebound or facing a prolonged crisis. This deep-dive analysis will unpack the essential details, from financial performance to market expectations, providing a strategic roadmap for interpreting the outcomes of this pivotal event.

The Pivotal 2025 Investor Relations Briefing

Hyosung Heavy Industries Corporation will present its performance and future outlook as a key participant in the Yuanta Securities Corporate Day. The primary goal is to restore investor confidence by transparently addressing recent challenges and outlining a clear path forward. This is more than a formality; it’s a strategic communication effort to redefine the company’s narrative.

Event Details at a Glance

- •Event: Hyosung Heavy Industries IR Briefing

- •Host: Yuanta Securities Corporate Day

- •Date & Time: November 13, 2025, at 3:30 PM KST

- •Source: Details confirmed in the Official Disclosure (DART).

Decoding the Financial Storm: A Deep Dive into Performance

Recent financial reports paint a concerning picture for Hyosung Heavy Industries. A sharp decline in revenue and a plunge into significant operating losses in 2024 have understandably shaken investor sentiment. The IR briefing must directly confront these figures.

The core challenge lies not just in explaining the past but in presenting a credible, data-backed plan for future profitability and growth. Investors will be scrutinizing every detail for signs of a genuine turnaround.

The Unsettling Numbers: Revenue and Profitability

The downward trend is stark when looking at key performance indicators:

- •Revenue: Plummeted from KRW 673 billion (2022) to KRW 334 billion (2024).

- •Operating Income: Shifted from a KRW 9 billion profit (2022) to a staggering KRW -594 billion loss (2024).

- •Return on Equity (ROE): Collapsed from 5.12% to -46.01%, indicating significant value destruction for shareholders.

These figures are attributed to a perfect storm of project delays, rising material costs, and a broader slowdown in the construction and heavy industry sectors, a trend seen across many global industrial markets.

A Silver Lining? Analyzing Financial Stability

Despite the grim profitability metrics, there are positive developments in the company’s balance sheet. The debt-to-equity ratio dramatically improved from 166.40% to a very healthy 38.67% in 2024. Simultaneously, the current ratio surged from 48.45% to 220.61%. These changes suggest a successful deleveraging strategy and a much stronger short-term liquidity position, giving management crucial breathing room to execute a turnaround.

The Macroeconomic Gauntlet: External Pressures

Hyosung Heavy Industries does not operate in a vacuum. Persistent high interest rates in Korea and the U.S., coupled with a weak Korean Won (KRW 1,466/USD as of Nov 2025), create significant headwinds. These factors inflate the cost of imported raw materials and increase the burden of foreign currency-denominated debt. The company’s strategy for mitigating these external risks will be a key focus of the IR briefing. For more insights, you can review our guide to analyzing industrial stocks.

Investor Action Plan & Key Questions

This IR event could be a major catalyst for the Hyosung Heavy Industries stock price. A convincing presentation could spark a rally, while a lack of clarity could lead to further decline. Investors should focus on the substance of the presentation, seeking answers to critical questions.

Key Questions for the Briefing:

- •Profitability Roadmap: What are the specific, actionable steps to reverse the massive operating losses of 2024?

- •New Growth Engines: What is the status of investments in high-growth areas like renewable energy infrastructure, and what is the timeline for revenue generation?

- •Order Backlog & Pipeline: Can management provide concrete details on the current order backlog and the outlook for securing new contracts in 2026 and beyond?

- •Capital Management: How will the improved liquidity be deployed? Will it be used for strategic investments, debt reduction, or shareholder returns?

In conclusion, the upcoming Hyosung Heavy Industries IR is a must-watch event. By carefully analyzing the company’s strategic responses to its current challenges, investors can make more informed decisions about its long-term potential.