The upcoming KUKDO CHEMICAL IR for Q3 2025 is poised to be a landmark event for investors and market analysts. As a significant force in the global chemical industry, KUKDO CHEMICAL CO.,LTD will not only unveil its quarterly performance but also provide critical insights into its future growth trajectory and risk management strategies. This deep-dive analysis will explore the key factors influencing the KUKDO CHEMICAL stock, dissect market expectations, and outline actionable strategies for investors ahead of this pivotal announcement.

This IR event transcends a simple earnings report; it’s a litmus test for the company’s resilience amidst global economic shifts and a window into its long-term investment appeal. We will examine both the bullish catalysts and the potential headwinds.

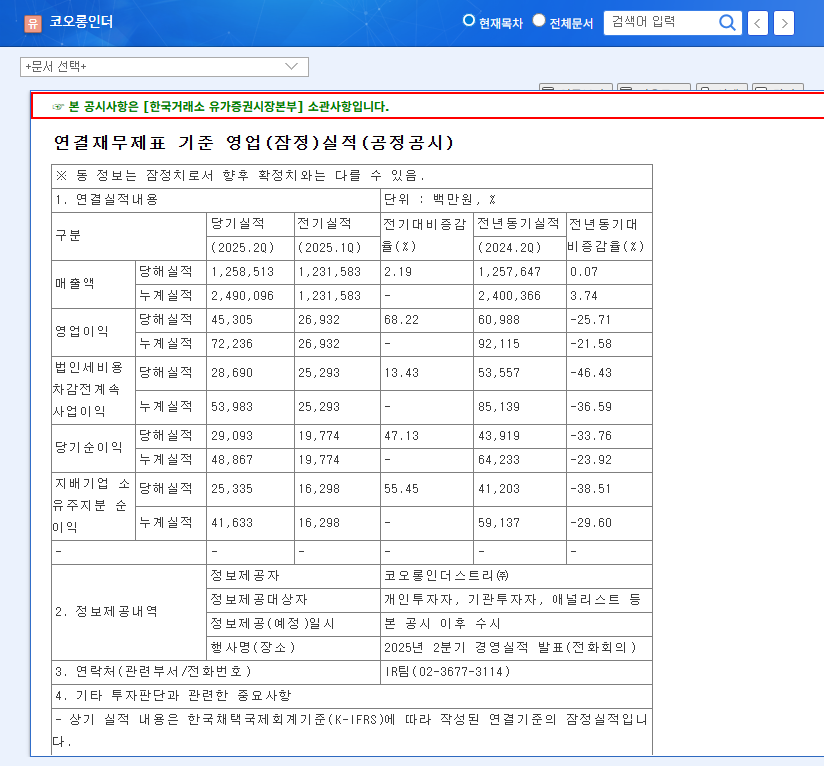

Setting the Stage: Recapping H1 2025 Performance

To understand the expectations for the KUKDO CHEMICAL Q3 2025 results, we must first look at the foundation built in the first half of the year. The semi-annual report for H1 2025 painted a picture of stable fundamentals, highlighted by impressive growth in the high-margin epoxy resin division. This performance was a key driver of positive market sentiment, but it was balanced by ongoing efforts to enhance profitability within the more competitive polyol resin division. The market will be watching closely to see if this momentum has been sustained and if the turnaround strategies for underperforming segments are bearing fruit.

Core Business Analysis: Catalysts and Concerns

Positive Factors Driving Growth

- •Epoxy Resin Strength: This division is expected to be the star performer. Demand is being supercharged by the global shipbuilding boom, requiring robust protective coatings. Furthermore, the expansion of AI and data centers fuels demand for high-performance materials in electronics. A favorable outcome from the U.S. anti-dumping petition could provide an additional, significant boost to the Q3 KUKDO CHEMICAL earnings.

- •Polyol Resin Turnaround: While facing challenges, the strategy to pivot towards higher-value System Polyol products and stabilize operations at the Ningbo, China factory shows promise. Increased global focus on energy efficiency in construction, a key end-market, presents a long-term growth opportunity.

- •Financial Prudence: A manageable debt-to-equity ratio (around 90% as of H1 2025) suggests a solid financial footing. Continued strong operating profit will further de-risk the balance sheet, a key factor for any chemical industry investment.

Negative Factors and Potential Risks

A balanced view requires acknowledging the potential headwinds. The company’s high proportion of overseas sales makes it vulnerable to macroeconomic shifts. Investors should pay close attention to management’s commentary on these points during the KUKDO CHEMICAL IR.

- •Geopolitical & Economic Uncertainty: Increasing protectionism and global economic slowdowns could dampen demand. For more on market trends, review analysis from sources like leading economic forums.

- •Margin Pressure: Intense price competition and over-supply in China’s polyol market, coupled with volatile raw material costs, could squeeze profit margins.

- •Currency and Rate Volatility: As a global exporter, fluctuations in exchange rates and interest rates can have a material impact on earnings. A clear risk management plan is essential.

- •ESG Scrutiny: Past environmental issues mean the company is under a microscope for its ESG (Environmental, Social, and Governance) practices. Proactive and transparent communication on improvements is crucial for maintaining investor trust.

Investment Strategy: What to Watch in the IR Event

For those invested or considering an investment in KUKDO CHEMICAL stock, this IR event is more than just numbers. It’s about the narrative and the forward-looking guidance. Your action plan should involve listening for key details and monitoring the market’s reaction.

Key Focus Points for Investors

- •Segment-Specific Margins: Look beyond top-line revenue. Are margins improving in the polyol division? Are epoxy margins holding strong? This reveals the true health of the core businesses.

- •Management’s Forward Guidance: Pay close attention to the outlook for Q4 2025 and early 2026. Any cautious language could signal impending challenges not yet reflected in the current quarter’s results.

- •R&D and CapEx Plans: Details on investment in high-value, eco-friendly products are a strong indicator of long-term competitiveness. These insights often reveal more than past performance, which you can learn about in our guide to analyzing R&D spending.

- •Q&A Session Tone: The questions from analysts and the conviction in management’s answers are invaluable. Hesitation or evasion on key topics like competition or currency risks can be a red flag.

Ultimately, a strong performance that exceeds market consensus could provide significant upward momentum for the stock. Conversely, a miss on revenue or earnings, or weak guidance, could trigger a sell-off. For the most accurate and direct information, investors should always consult the company’s official filings. The complete report for this period can be found in the Official Disclosure on DART.