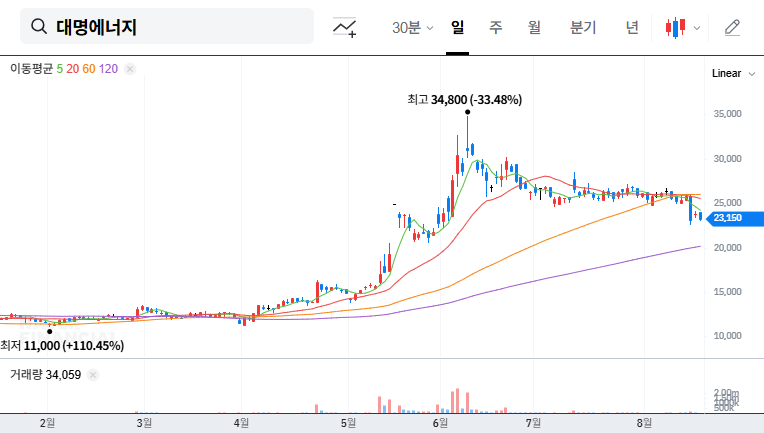

In a significant development for the renewable energy sector, Dae Myoung Energy Co. Ltd. (389260) has secured a landmark contract that promises to reshape its growth trajectory. The announcement of a ₩13.9 billion solar installation project with the prestigious Incheon International Airport Corporation is not just a major revenue boost; it’s a powerful validation of the company’s capabilities and a critical event for investors. This deep-dive analysis will unpack the contract details, evaluate the impact on Dae Myoung Energy stock, and provide a comprehensive forecast for potential investors.

The Landmark Incheon Airport Solar Project Deal

Dae Myoung Energy has officially announced a single sales and supply contract for the ‘North Breakwater Solar Power Installation Project’ with Incheon International Airport Corporation. The deal, valued at a substantial ₩13.9 billion, represents a remarkable 20.52% of the company’s total revenue from 2022. This development was confirmed in an Official Disclosure. The project’s timeline is set from November 7, 2025, to July 7, 2027, spanning approximately one year and eight months of strategic development and execution.

This isn’t just another contract. Partnering with a national infrastructure giant like Incheon International Airport elevates Dae Myoung Energy’s profile significantly, demonstrating its trusted capacity for executing large-scale, high-stakes projects. This achievement will serve as a powerful reference, potentially unlocking further opportunities in public-sector renewable energy initiatives across the nation.

Why This Contract is a Game-Changer

The significance of the Incheon Airport solar project extends far beyond its immediate monetary value. It acts as a powerful catalyst for both short-term performance and long-term strategic positioning.

Immediate Financial Injection and Profitability

The contract is poised to directly enhance revenue and profitability between late 2025 and mid-2027. This influx of capital is crucial, especially following a reported revenue decrease in H1 2025. Despite lower revenues, the company managed to increase its operating and net profits, signaling improved operational efficiency. This project will supercharge that trend, providing a stable, high-value revenue stream.

Strengthening Core Business Divisions

Dae Myoung Energy’s fundamentals are rooted in several key areas. This project positively impacts its primary renewable energy EPC division and solidifies its market leadership.

- •EPC Division (55% of Revenue): With a robust order backlog of ₩284.4 billion, this new contract adds another layer of security and growth potential. It reinforces the company’s expertise in both solar and wind power construction.

- •Power Generation (38% of Revenue): While this division provides stable income from long-term contracts, it remains exposed to REC (Renewable Energy Certificate) price volatility. Successful EPC projects help fund and expand these generation assets.

- •O&M Services (5% of Revenue): High-profile projects like the Incheon Airport one often lead to long-term operations and maintenance contracts, feeding this growing, high-margin business segment.

This contract is a clear signal of market confidence in Dae Myoung Energy. Securing a project of this scale with a public entity like Incheon Airport validates their technical expertise and solidifies their role as a key player in South Korea solar power development.

Dae Myoung Energy Stock: Outlook & Investment Strategy

For investors, this news presents a compelling, multi-faceted opportunity. The announcement is expected to create significant positive short-term momentum for the Dae Myoung Energy stock as the market digests the news of secured future revenues. Historically, such large contract announcements lead to increased investor interest and stock price volatility.

Mid-to-Long-Term Growth Drivers

Beyond the initial spike, the long-term outlook is enhanced. The successful completion of this project will be a powerful case study, positioning Dae Myoung Energy favorably for future large-scale tenders. This aligns perfectly with the South Korean government’s supportive policies for renewable energy expansion, a key tailwind for the entire industry. The global trend towards clean energy, as documented by authorities like the International Energy Agency, provides a stable backdrop for sustained growth.

Key Risks and Considerations

Despite the overwhelmingly positive news, prudent investors must remain aware of potential risks. The company’s long-term debt and financial liabilities require careful monitoring. Efficient cash flow management will be critical during the project’s execution phase. Furthermore, macroeconomic factors such as interest rate hikes (increasing debt servicing costs) and currency volatility (affecting the cost of imported components) remain external risks. For those new to this area, understanding the fundamentals is key; consider reading our Guide to Investing in Renewable Energy Stocks.

In conclusion, this contract is a highly positive catalyst for Dae Myoung Energy. We maintain a positive outlook, but recommend investors closely track project milestones, quarterly financial reports, and the company’s efforts to improve its overall financial structure. The successful execution of the Incheon Airport solar project could mark the beginning of a new era of growth for the company.