This comprehensive TOVIS stock forecast delves into the recent performance and future potential of global display solutions provider TOVIS Co., Ltd. (051360). With a strong performance in the first half of 2025, fueled by its booming TOVIS automotive display division, the company is capturing significant market attention. Adding to the bullish sentiment, recent disclosures reveal that the company’s major shareholder has increased their stake, a classic sign of insider confidence. This analysis will dissect TOVIS’s fundamentals, the implications of these key events, and provide a detailed outlook for investors considering this burgeoning tech stock.

We’ll examine whether these positive catalysts are enough to propel TOVIS’s corporate value and stock price to new heights, providing the critical information needed for well-informed investment decisions.

Key Catalysts: H1 2025 Performance & Shareholder Confidence

Two major developments have placed TOVIS (051360) in the spotlight: exceptional financial results and a significant vote of confidence from its largest shareholder. These events provide a solid foundation for our TOVIS stock analysis.

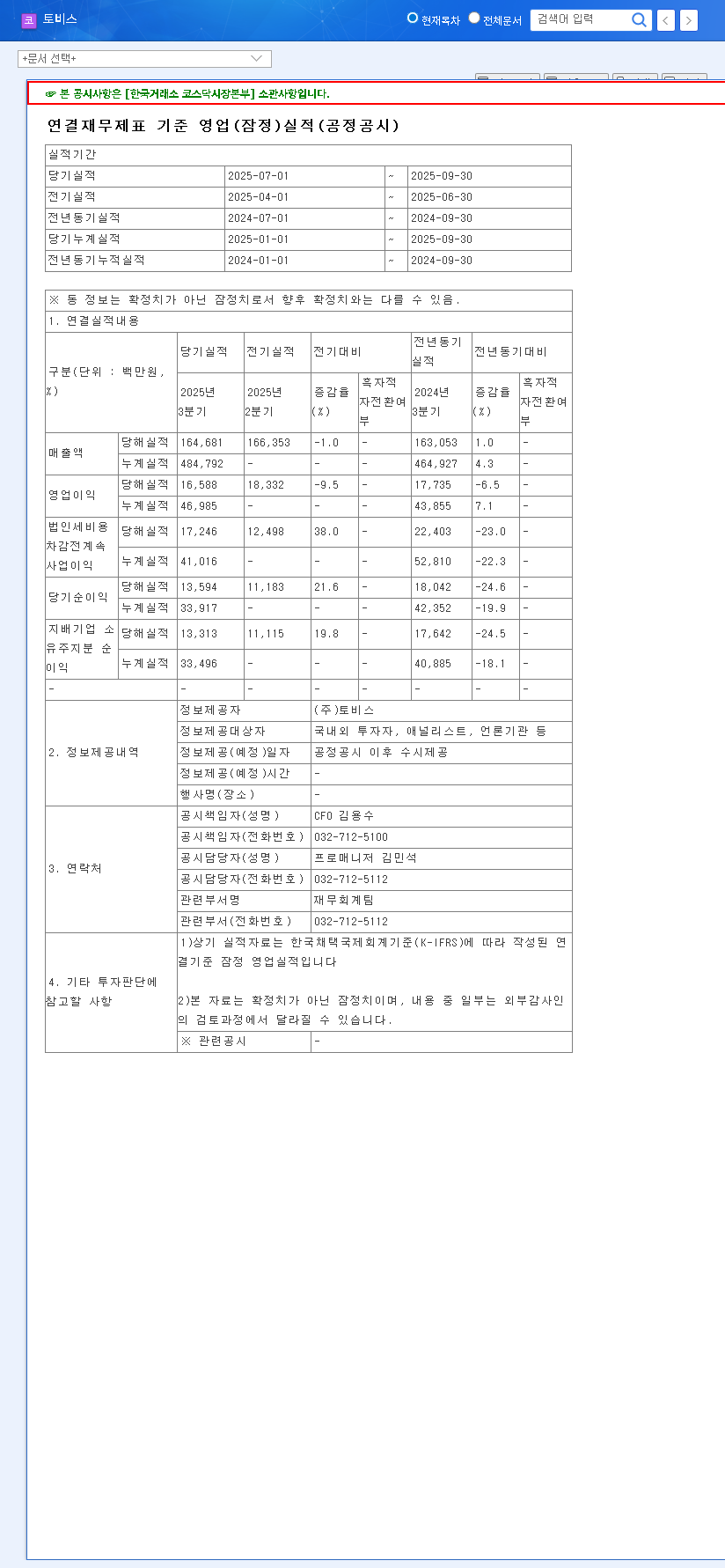

1. Robust H1 2025 Financial Performance

The company’s semi-annual report paints a picture of robust health and strategic success:

- •Impressive Earnings: TOVIS reported revenue of KRW 320.1 billion, an operating profit of KRW 30.4 billion, and a net profit of KRW 20.3 billion, showcasing significant year-over-year growth.

- •Automotive Division Shines: The TOVIS automotive display business was the star performer, exhibiting high growth and cementing its role as the company’s primary future growth engine.

- •Stable Industrial Base: The industrial monitor division, a long-standing cash cow, continued its stable growth trajectory thanks to a well-diversified product portfolio.

2. Major Shareholder Increases Stake, Signaling Strong Belief

In a significant move, major shareholder Yong-Beom Kim and related parties acquired an additional 0.46% of the company through on-market purchases in November 2025. This increased their total holding from 15.26% to 15.72%. This action, confirmed in the Official Disclosure, is widely interpreted by analysts as a powerful vote of confidence in the company’s long-term strategy and growth potential.

Insider buying by a major shareholder is one of the strongest positive signals for investors, suggesting that those with the most information are bullish on the company’s future prospects.

Why This Matters: Dissecting TOVIS’s Core Strengths

These events are particularly meaningful because they build upon TOVIS’s already solid business foundation. The synergy between its growth engine and its stable core business creates a compelling investment thesis.

The Power of the Automotive Display Market

The automotive sector is undergoing a massive transformation, often summarized by the MECA trend (Mobility, Electrification, Connectivity, Autonomous). This shift, detailed by leading analysts at top consulting firms, places digital displays at the heart of the modern vehicle. TOVIS is perfectly positioned to capitalize on this, supplying advanced infotainment systems and digital instrument clusters. Continued investment in next-generation technologies like OLED and Scenic View HUDs further solidifies its competitive advantage.

Solid Financials and Reasonable Valuation

TOVIS maintains a healthy balance sheet, with a stable debt-to-equity ratio of 94.6% and improving operating cash flow. Its current valuation, with a PER of 20.3x and a PBR of 0.94x, reflects its growth trajectory while still offering potential for upside as its ROE improves. This financial stability is crucial for navigating market volatility, a topic we cover in our broader analysis of the tech hardware sector.

Potential Risks and Headwinds

Despite the positive outlook, no investment is without risk. Prospective investors in TOVIS should monitor the following factors:

- •Foreign Exchange Volatility: With a high export ratio, fluctuations in the KRW against the USD and EUR can significantly impact net profit. The company estimates a 5% currency change could alter net profit by ~KRW 1.16 billion.

- •Macroeconomic Pressures: A global economic slowdown, persistent inflation, or rising interest rates could dampen consumer demand for new vehicles and affect the industrial sector.

- •Competitive Landscape: The display market is intensely competitive, requiring continuous innovation and R&D investment to stay ahead.

Investor Action Plan: A ‘Buy’ Recommendation for TOVIS

Considering the powerful growth in the TOVIS automotive display segment, strong fundamentals, and the significant vote of confidence from the TOVIS major shareholder, our TOVIS stock forecast concludes with a ‘BUY’ rating.

The company represents an attractive investment with a clear path to continued growth and stock price appreciation. Key points to monitor going forward include order flow for the automotive division, the impact of currency hedging strategies, and the commercialization timeline for its next-generation display technologies.

Frequently Asked Questions (FAQ)

What are the main business segments of TOVIS Co., Ltd.?

TOVIS operates two primary business segments: industrial monitors (used in gaming, medical, and aviation) and automotive displays (for vehicle infotainment systems and instrument clusters).

Why is the TOVIS major shareholder’s stake increase important?

An increase in stake by insiders is a strong positive signal. It enhances management stability and shows that those with the most intimate knowledge of the company are confident in its future growth and stock performance.

What are the primary growth drivers for a positive TOVIS stock forecast?

The key growth drivers are the rapid expansion of the automotive display market due to the MECA trend and the company’s ongoing R&D in next-generation technologies like OLED and Scenic View HUDs.