The gaming industry is at a crossroads, and the recent news surrounding the Kakao Games Kakao VX deal has sent ripples through the market. Kakao Games Corp. announced its decision to divest its entire stake in subsidiary Kakao VX for a substantial ₩259.5 billion. This isn’t just a simple asset sale; it represents a critical strategic pivot that could redefine the company’s future trajectory, financial structure, and growth prospects.

For investors, the key question is whether this move is a masterstroke to secure future growth or a reactive measure to patch up a deteriorating balance sheet. Will this divestment act as the catalyst for a comeback, pulling the company out of its H1 2025 financial slump? Or are there more fundamental challenges that this cash infusion can’t solve? This comprehensive analysis provides a deep dive into the Kakao Games stake sale and offers a clear investment strategy for 2025.

The Landmark Deal: Deconstructing the Kakao VX Divestment

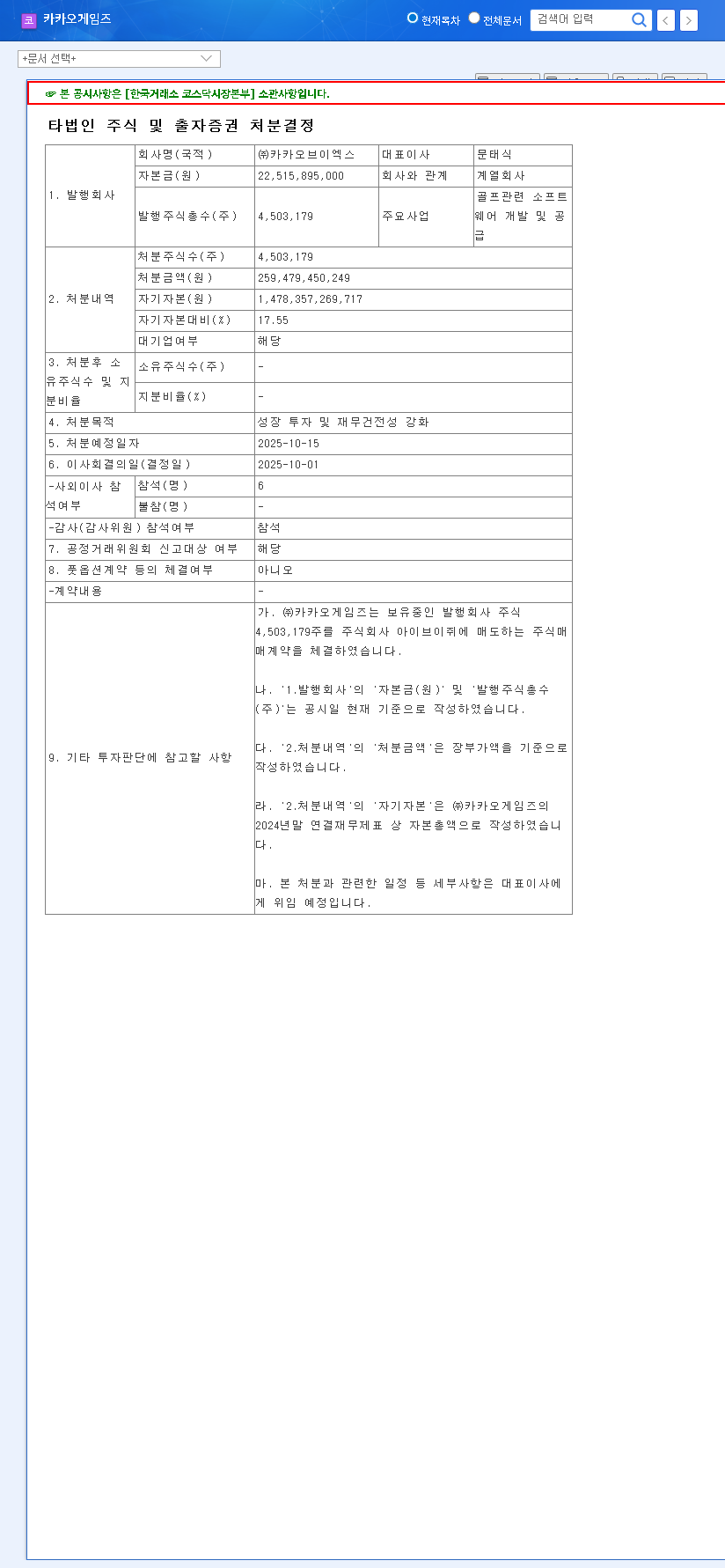

On October 1, 2025, Kakao Games confirmed its board’s resolution to dispose of its entire holding in Kakao VX Co., Ltd., a subsidiary known for its golf-related software and screen golf technology. This transaction, scheduled for completion by October 15, 2025, is valued at ₩259.5 billion (approximately $190 million USD), a figure that represents a significant 17.55% of Kakao Games’ total capital.

- •Disposal Target: Full stake in Kakao VX Co., Ltd.

- •Disposal Amount: ₩259.5 billion.

- •Ratio to Equity Capital: 17.55%.

- •Official Disclosure: The transaction details were formally registered, and you can view the filing here: Source.

Why Now? Analyzing Kakao Games’ Financial Health

The official reasoning provided by Kakao Games for this significant move is to secure funds for ‘growth investment and to strengthen financial soundness.’ A closer look at the company’s H1 2025 financial report reveals why this action was not just strategic, but necessary.

The first half of 2025 painted a grim picture for Kakao Games, marked by declining revenue, a swing to an operating loss, and a concerning surge in debt.

Key Financial Red Flags from H1 2025

- •Plummeting Revenue: Consolidated revenue fell by a sharp 27.9% year-over-year to ₩238.66 billion.

- •Operating Loss: The company recorded an operating loss of ₩21.05 billion, a stark reversal from the profit seen in the previous year, driven by high R&D spending and other costs.

- •Soaring Debt: Long-term borrowings ballooned from ₩147 billion to ₩626.7 billion, pushing the debt-to-equity ratio to an alarming 119.55%.

Given this context, the sale of Kakao VX, a non-core asset, is a clear attempt to inject vital liquidity, pay down debt, and refocus capital on the primary gaming business, which has faced headwinds in a competitive market. For more on market trends, see this analysis from leading industry reports.

Investment Impact: The Pros and Cons of the Kakao Games Stake Sale

The divestment of the Kakao VX stake will have a multifaceted impact on Kakao Games’ stock and long-term outlook.

The Upside: A Path to Recovery?

- •Strengthened Balance Sheet: The ₩259.5 billion cash infusion provides immediate liquidity to reduce debt and alleviate financial pressure, which the market should view favorably.

- •Capital for Core Business: These funds can be reinvested into developing promising new titles and expanding the global publishing footprint, fueling future growth engines.

- •Strategic Focus: Shedding the non-core golf business allows management to concentrate exclusively on its core competency: game development and publishing.

The Downside: Lingering Headwinds

- •No Quick Fix for Performance: The sale does not immediately solve the underlying issue of declining revenue from existing titles like ‘Odin: Valhalla Rising’. Core business recovery is still paramount.

- •Execution Risk: The success of this move hinges on how effectively the new capital is deployed. A failure to produce hit titles or successful blockchain initiatives (BORA) would negate the benefits.

- •Persistent Financial Burden: Even with the cash injection, the company’s high debt load and significant R&D expenses remain considerable challenges that require ongoing management.

2025 Investor Action Plan & Outlook

While the Kakao Games Kakao VX deal is a step in the right direction, significant uncertainties remain. A prudent approach is necessary. Investors should closely monitor several key performance indicators before making a decision.

- •New Title Pipeline: Watch the launch and market reception of upcoming games like ‘Goddess Order’. Success here is crucial. Explore our analysis of upcoming game releases for more context.

- •Debt Reduction: Track how the funds are used and whether there is a measurable improvement in the debt-to-equity ratio in the coming quarters.

- •Profitability Metrics: Look for signs of improved operational efficiency and a return to operating profit.

Given the balance of positive potential and persistent risks, a “Hold” rating is appropriate. This event creates potential upside, but the company must still prove it can execute on its recovery plan. A wait-and-see approach is recommended.

Disclaimer: This content is for informational purposes only and does not constitute investment advice. All investment decisions should be made with the consultation of a qualified financial professional.