A significant development has unfolded for DAIYANG METAL (009190), sending ripples through the investment community. BB-One Partnership, a major institutional shareholder, has divested a substantial portion of its stake, raising critical questions about the company’s future. While DAIYANG METAL has shown promising signs of a financial turnaround, this large-scale sale creates uncertainty. This comprehensive analysis will delve into the company’s core fundamentals, the external market pressures, and the direct impact of this shareholder change on DAIYANG METAL stock, providing a clear roadmap for investors.

The Catalyst: BB-One Partnership’s Major Stake Sale

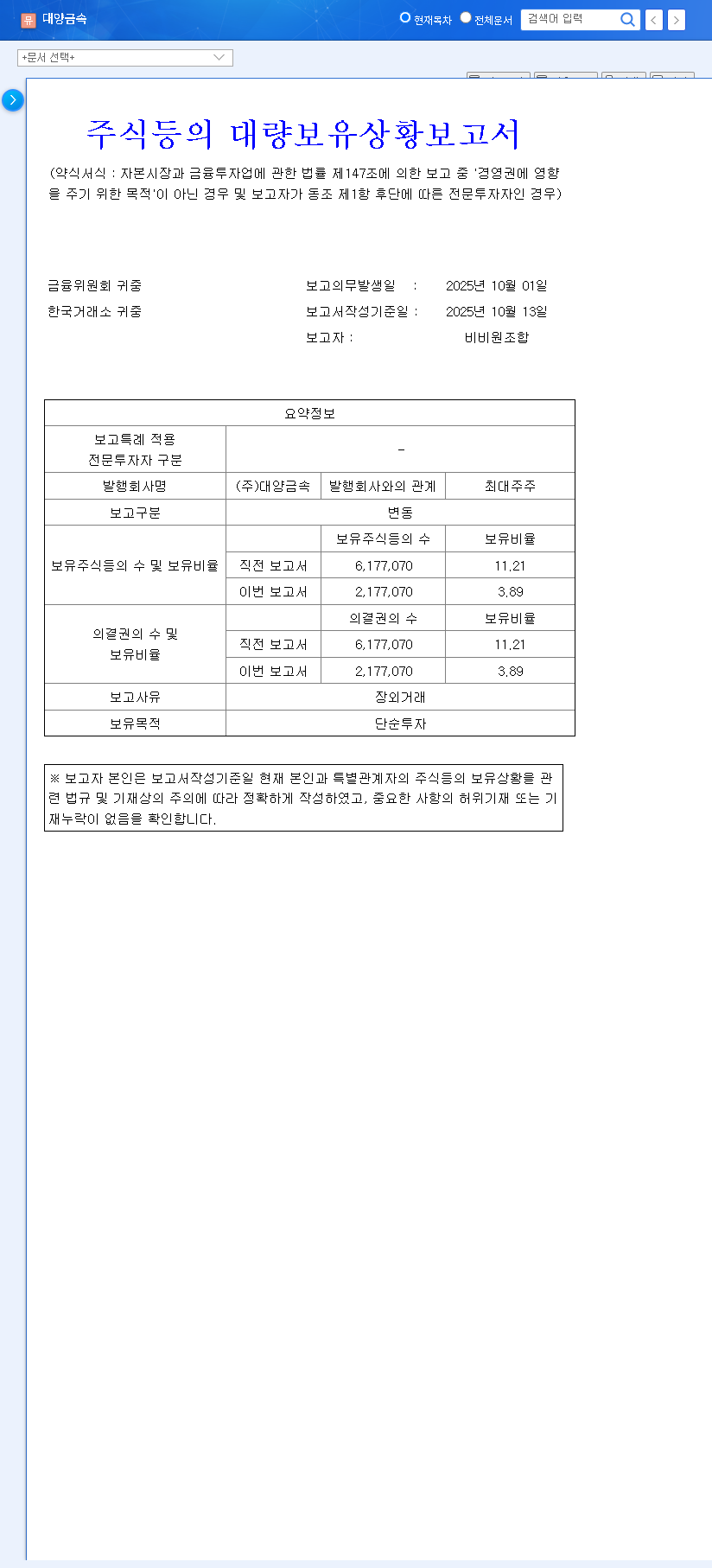

On October 13, 2025, a mandatory disclosure revealed a pivotal shift in the ownership structure of DAIYANG METAL CO., LTD (009190). BB-One Partnership, a key investor, executed a large-scale, off-market sale, drastically reducing its holdings from 11.21% down to just 3.89%. An off-market transaction is a private sale between two parties, and a divestment of this magnitude from a major shareholder is often a signal that warrants careful scrutiny. The details of this transaction were made public through an Official Disclosure on DART. Given DAIYANG METAL’s market capitalization of approximately 67.3 billion KRW, this event represents a significant liquidity event that can impact market dynamics.

A Deep Dive into DAIYANG METAL (009190) Fundamentals

To understand the context of the stake sale, we must analyze the company’s recent performance and financial health. The first half of 2025 presented a mixed but cautiously optimistic picture for DAIYANG METAL.

The Bright Side: A Return to Profitability

- •Revenue Growth: A modest year-on-year revenue increase to 111.392 billion KRW was achieved, driven largely by stronger export performance.

- •Operating Profit Turnaround: The company successfully shifted from an operating loss to a profit of 2.597 billion KRW, a testament to improved operational efficiency and reduced administrative expenses.

- •Net Profit Turnaround: Similarly, net income turned positive at 2.661 billion KRW, bolstered by non-operating gains.

- •Stronger Balance Sheet: An increase in total equity and cash equivalents suggests improving financial soundness and better short-term liquidity.

Headwinds and Hurdles: Critical Risks to Consider

- •Raw Material Costs: Rising prices for imported stainless steel Hot Coil pose a direct threat to profit margins.

- •Debt Burden: The upcoming maturity of convertible bonds (CB) on November 10, 2025, is a major financial hurdle that requires a clear refinancing or repayment strategy to avoid potential shareholder dilution.

- •Production Decline: A sharp 50% year-on-year drop in stainless steel cold rolled sheet production is a significant red flag, indicating falling market demand or internal operational issues.

- •Receivables Management: An increase in accounts receivable requires proactive credit risk management to ensure healthy cash flow.

Market & Industry Analysis: The External Pressures

DAIYANG METAL does not operate in a vacuum. The broader economic environment presents its own set of challenges. The global steel market is currently experiencing a downturn, characterized by weak demand and volatile raw material prices. Competition within the stainless steel sector is fierce, putting constant pressure on pricing and quality. Furthermore, macroeconomic factors like fluctuating interest rates and currency exchange rates (KRW/USD, KRW/EUR) directly impact borrowing costs, import expenses, and export revenues for DAIYANG METAL.

Analyzing the Ripple Effect: How the Stake Sale Impacts DAIYANG METAL Stock

The exit of a major shareholder like BB-One Partnership can have several immediate and mid-term consequences for the stock price:

In the short term, the primary impact will likely be negative. The perception of a key investor losing confidence, combined with a potential oversupply of shares, can create significant downward pressure on the DAIYANG METAL stock price.

- •Selling Pressure: A large block of shares changing hands can lead to increased selling in the open market, creating a supply-demand imbalance.

- •Deteriorated Investor Sentiment: Despite the positive earnings turnaround, a major shareholder’s exit can be interpreted as a lack of faith in the company’s long-term prospects, spooking retail and institutional investors alike.

- •Weakened Shareholder Activism: With its stake below 5%, BB-One’s ability to influence management or advocate for shareholder rights is significantly diminished, which could be a negative for corporate governance.

Investment Outlook & Recommendation

Given the conflicting signals—improving profits versus a major stake sale and underlying operational risks—a cautious approach is essential. For the mid-to-long-term trajectory of DAIYANG METAL stock, investors should closely monitor the company’s ability to address its fundamental challenges. Key performance indicators will be the recovery of production volume, sustained cost management, and a successful resolution to the convertible bond maturity. Until these uncertainties are resolved and a pattern of sustained improvement is confirmed, the investment risk remains elevated.

Overall Opinion: We are issuing a ‘Sell-Hold‘ recommendation. Existing investors may consider holding but should be wary of short-term volatility. New investors are advised to wait on the sidelines until there is clearer evidence of structural improvements in the company’s fundamentals and the market has fully absorbed the impact of this stake sale.

Frequently Asked Questions (FAQ)

Q1: What was the major shareholder change for DAIYANG METAL (009190)?

A1: BB-One Partnership, a major shareholder, sold a large portion of its shares, reducing its stake in DAIYANG METAL from 11.21% to 3.89% through off-market transactions.

Q2: How will this stake sale impact DAIYANG METAL’s stock price?

A2: It is expected to create short-term downward pressure on the stock due to increased selling volume and negative investor sentiment. The mid-to-long-term impact will depend on the company’s fundamental performance.

Q3: What are the key fundamentals for DAIYANG METAL right now?

A3: The company achieved a positive turnaround in operating and net profit in H1 2025. However, it still faces significant risks, including rising raw material costs, a heavy debt burden with maturing convertible bonds, and a sharp decline in production volume.