The AK Holdings Aekyung Industrial sale has sent shockwaves through the Korean investment market. In a landmark move, AK Holdings, Inc. announced the complete divestment of its majority stake in its core subsidiary, Aekyung Industrial. This strategic transaction, valued at a staggering ₩470 billion, promises to fundamentally reshape AK Holdings’ financial landscape and unlock new avenues for growth and investment. For investors, this deal presents both significant opportunities and critical questions about the future of both companies.

This comprehensive analysis will delve into the specifics of the acquisition, the profound impact on AK Holdings’ balance sheet, the dawn of a new era for Aekyung Industrial under private equity leadership, and a strategic action plan for investors navigating this pivotal event.

Anatomy of the ₩470 Billion Divestment

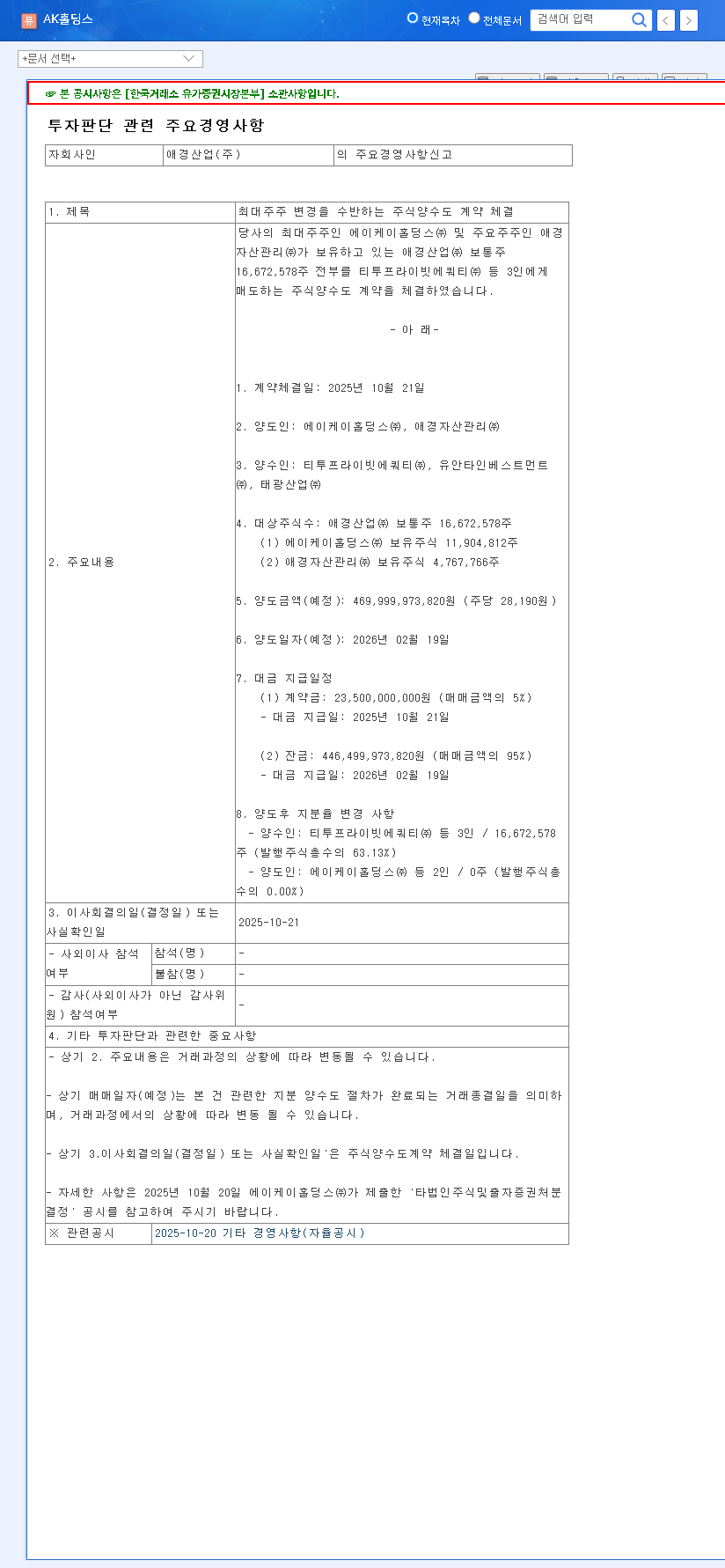

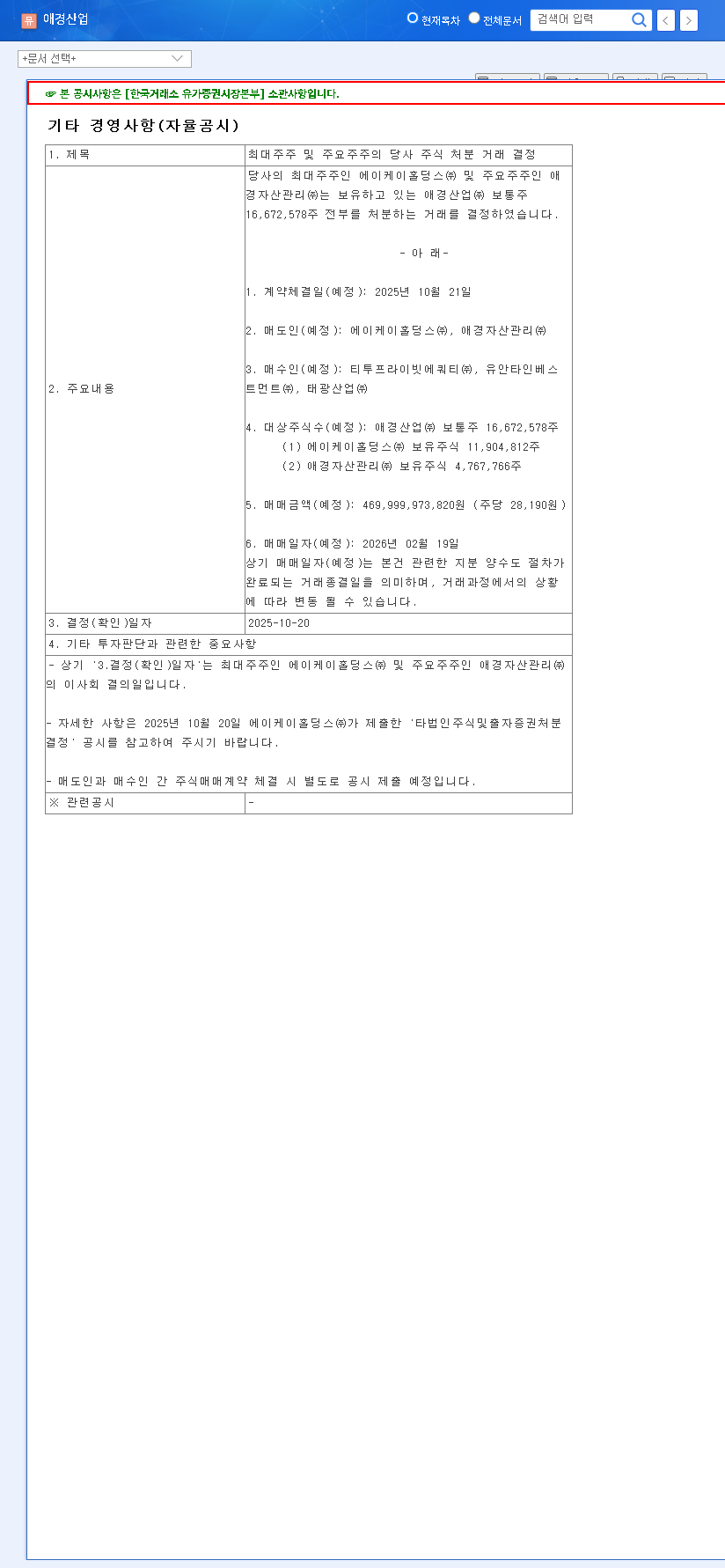

AK Holdings has formally entered into a stock transfer agreement to sell its entire 63.13% stake in Aekyung Industrial. This move signals a complete exit from its long-held subsidiary, transferring control to a consortium of new majority shareholders. For full transparency, the official filing can be reviewed directly from the source.

Official Disclosure: Click to view the DART report.

Key Transaction Details

- •Sellers: AK Holdings, Inc. & Aekyung Asset Management Co., Ltd.

- •Buyers: A consortium led by T2 Private Equity, Yuanta Investment Co., Ltd., and Taekwang Industrial Co., Ltd.

- •Target Shares: 16,672,578 common shares (63.13% of total).

- •Transfer Amount: Approximately ₩470 billion (₩28,190 per share).

- •Estimated Closing Date: February 19, 2026.

Analyzing the Profound Impact of the Sale

This divestment is not merely a financial transaction; it’s a strategic pivot that will have lasting consequences for all parties involved, as well as the broader market.

The infusion of ₩470 billion provides AK Holdings with an unprecedented war chest, enabling a fundamental restructuring of its corporate identity and investment thesis for the next decade.

For AK Holdings: A New Financial Chapter

The most immediate outcome for AK Holdings is a dramatic enhancement of its financial flexibility. This cash influx can be deployed in several strategic ways: deleveraging the balance sheet by repaying debt, launching aggressive new business ventures, funding R&D in emerging technologies, or increasing shareholder returns through dividends and buybacks. The sale of Aekyung Industrial will force a re-evaluation of AK Holdings’ role as a holding company, shifting its focus towards identifying and nurturing new growth engines. This strategic ambiguity is where both risk and opportunity lie for the AK Holdings stock.

For Aekyung Industrial: New Ownership, New Direction

With private equity firms at the helm, Aekyung Industrial is poised for significant operational changes. PEF ownership typically brings a sharp focus on efficiency, cost optimization, and aggressive market expansion. This could unlock new value and streamline operations. However, this often comes with pressure for short-term profitability, which could potentially conflict with long-term brand building and R&D investment. The involvement of a strategic player like Taekwang Industrial suggests a hybrid approach, blending financial discipline with industry expertise. For more on this dynamic, you can explore our guide on Understanding Private Equity in Corporate Acquisitions.

Investor Action Plan & Key Considerations

While the AK Holdings Aekyung Industrial sale is largely seen as a positive catalyst, prudent investors must weigh the uncertainties. The long-term success hinges entirely on the execution of AK Holdings’ subsequent investment strategy.

Strategic Questions to Monitor

- •Capital Deployment Strategy: Where exactly will the ₩470 billion be invested? Will it be a single large acquisition or a series of smaller bets in high-growth sectors?

- •Execution Risk: Can the deal close smoothly by the February 2026 deadline without regulatory hurdles or changes in market conditions?

- •Market Reaction: How will institutional investors and analysts, like those at Bloomberg, react as more details about AK Holdings’ future plans emerge?

- •Growth Engine Void: Can AK Holdings successfully replace the stable earnings previously generated by Aekyung Industrial? Failure to do so could negatively impact long-term corporate value.

Frequently Asked Questions (FAQ)

Why did AK Holdings sell its stake in Aekyung Industrial?

While not explicitly stated, the AK Holdings divestment is a strategic move to secure nearly half a trillion won in cash. This enhances financial health and provides capital to pivot towards new, potentially higher-growth business areas.

What is the short-term outlook for AK Holdings’ stock price?

In the short term, the stock price may see a positive impact due to the improved financial structure and anticipation of future investments. However, long-term performance will depend entirely on how effectively management utilizes the newly acquired funds.

What changes can be expected at Aekyung Industrial?

The Aekyung Industrial acquisition by private equity suggests a future focused on maximizing operational efficiency and aggressive growth. This could involve new product launches, market entries, or restructuring efforts to boost profitability.

Disclaimer: This analysis is based on publicly available information and should not be considered direct investment advice. All investment decisions should be made based on individual research and discretion.