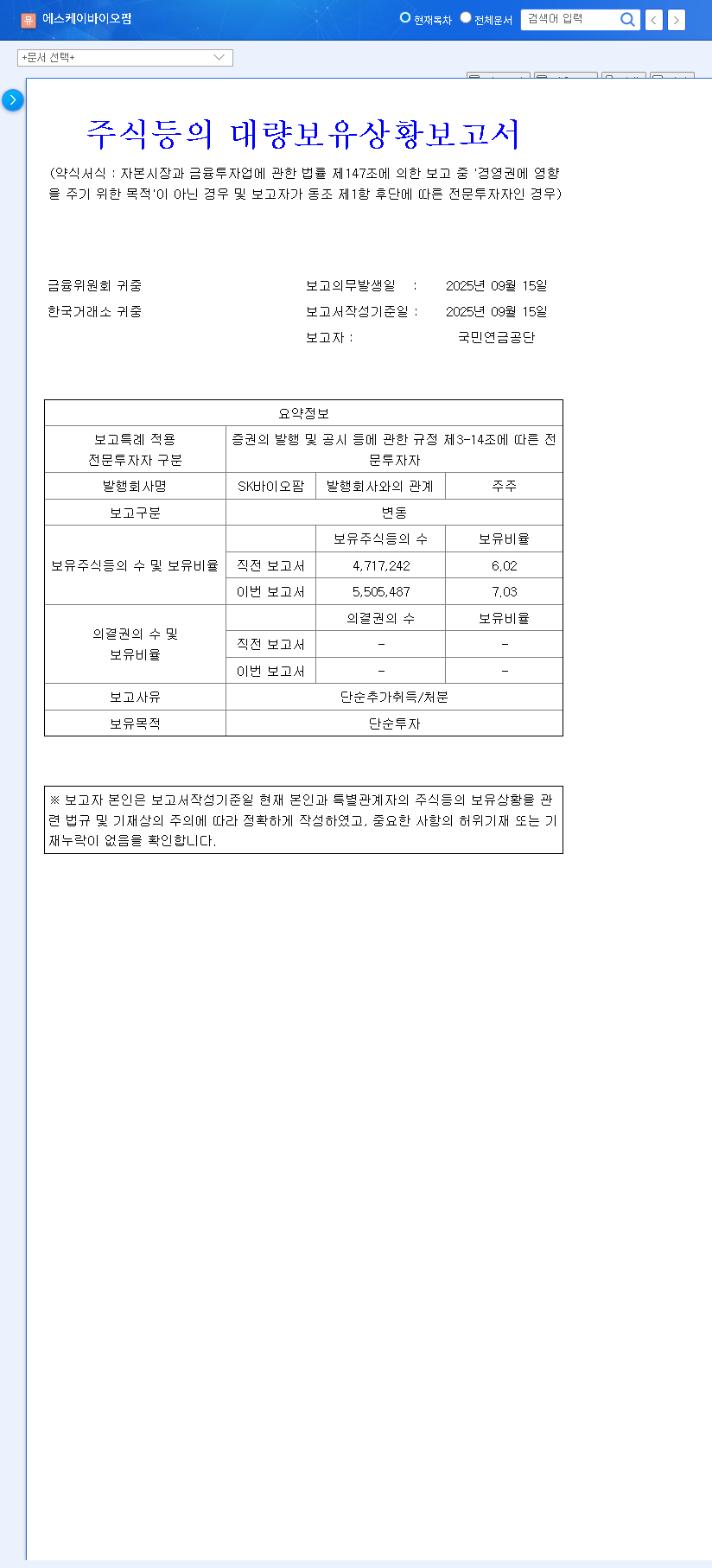

Investors following SK Biopharm stock have taken notice of a pivotal development. According to an Official Disclosure on October 1, 2025, the National Pension Service (NPS) of Korea significantly increased its stake in SK Biopharm (KRX: 326030) to 7.03%. This move, classified as a ‘simple investment,’ is a powerful endorsement from one of the world’s largest pension funds and signals deep confidence in the company’s trajectory.

This article provides an in-depth analysis of the factors underpinning this major SK Biopharm investment. We will meticulously examine the robust fundamental improvements detailed in the H1 2025 report, from explosive financial growth to the success of its flagship drug, Cenobamate, and strategic investments in future growth drivers. This comprehensive review will help clarify the current valuation and future potential of SK Biopharm stock.

NPS Boosts Stake: A Major Vote of Confidence

The decision by the National Pension Service to increase its ownership from 6.02% to 7.03% is more than just a routine portfolio adjustment. An increase of a full percentage point represents a substantial capital allocation and serves as a strong market signal. Institutional investments of this scale are typically preceded by exhaustive due diligence, suggesting the NPS sees significant long-term value and stability in the company’s future.

The NPS’s ‘simple investment’ classification, far from being trivial, indicates a belief that the current market price does not fully reflect SK Biopharm’s intrinsic value and growth potential. It is a clear bet on the company’s core fundamentals.

Deep Dive: The Robust Fundamentals Driving Value

The NPS’s confidence is well-founded. The H1 2025 report paints a picture of a company firing on all cylinders, with impressive financial performance, a powerful core product, and a clear vision for future innovation.

Explosive Financial Performance

The numbers speak for themselves, showcasing a company in a high-growth phase with improving efficiency.

- •Revenue Growth: H1 2025 revenue soared to KRW 320.7 billion, a remarkable 29.3% increase year-over-year, driven primarily by the strong performance of Cenobamate.

- •Operating Profit Surge: Profitability skyrocketed, with operating profit hitting KRW 87.6 billion—a 141.3% jump from the previous year. This demonstrates exceptional operational leverage and cost management.

- •Improved Financial Health: The company’s debt-to-equity ratio has dramatically improved to 55.2%, signifying a much stronger and more resilient balance sheet.

Cenobamate: The Blockbuster Growth Engine

Cenobamate (marketed as XCOPRI®/ONTOZRY®) is the cornerstone of SK Biopharm’s success. This anti-seizure medication continues to expand its market share within the highly competitive U.S. epilepsy treatment market. Its steady sales growth is complemented by increasing royalty revenues from licensing partners in Europe and other global regions, solidifying its status as a true blockbuster drug and providing a stable foundation for the company’s financial strength.

Innovating for the Future: RPT and TPD

A forward-looking SK Biopharm investment thesis must account for its future pipeline. The company is strategically expanding beyond its core CNS portfolio into cutting-edge oncology fields:

- •Radiopharmaceutical Therapy (RPT): This modality uses radioactive compounds to precisely target and destroy cancer cells, offering a highly potent treatment approach. Explore more about the potential of RPT in oncology.

- •Targeted Protein Degradation (TPD): TPD technology harnesses the body’s natural cellular disposal systems to eliminate disease-causing proteins that were previously considered ‘undruggable’.

These strategic moves, including the acquisition of SK Life Science Labs, signal a commitment to securing long-term growth engines and diversifying the R&D pipeline beyond Cenobamate.

Investment Thesis: Is SK Biopharm Stock a Buy?

Considering the powerful endorsement from the NPS, stellar financial growth, and a promising R&D strategy, the outlook for SK Biopharm stock appears highly favorable. The combination of a proven commercial product and investment in next-generation therapeutic modalities creates a compelling case for long-term investors.

Investment Highlights (Pros)

- •Institutional Confidence: The NPS’s increased stake enhances credibility and may stabilize long-term stock performance.

- •Proven Growth Driver: Continued strong sales and market expansion of Cenobamate provide a reliable revenue stream.

- •Future-Proofing: Strategic entry into high-potential fields like RPT and TPD secures future growth avenues.

- •Solid Financials: Rapidly improving profitability and a strengthened balance sheet reduce investment risk.

Key Risk Factors (Cons)

No investment is without risk. Prospective investors should remain aware of the following challenges:

- •R&D Uncertainty: Clinical trials are long, expensive, and carry no guarantee of success. Failures in the pipeline could impact future valuation.

- •Market Competition: The pharmaceutical landscape is highly competitive, with risks from new rival drugs and eventual patent expirations.

- •Macroeconomic Headwinds: As a global company, SK Biopharm is exposed to foreign exchange rate fluctuations and broader economic shifts.

Overall Opinion: Buy. The positive catalysts, strong financial momentum, and institutional backing currently outweigh the inherent risks, presenting a compelling opportunity for investors with a long-term horizon. As always, this analysis is for informational purposes, and investment decisions should be made based on your own research and risk tolerance.