The recent move by the National Pension Service (NPS) to increase its stake in the KC Tech stock (281820) has sent a significant signal across the market. As Korea’s largest and most influential institutional investor, the NPS’s actions are scrutinized for deeper meaning. While officially labeled a ‘simple investment,’ such a move from an entity managing the nation’s retirement funds often foreshadows a strong belief in a company’s long-term value. This analysis will dissect this pivotal event, explore KC Tech’s underlying fundamentals, and provide a strategic outlook for current and potential investors.

The Catalyst: NPS Boosts KC Tech Stake

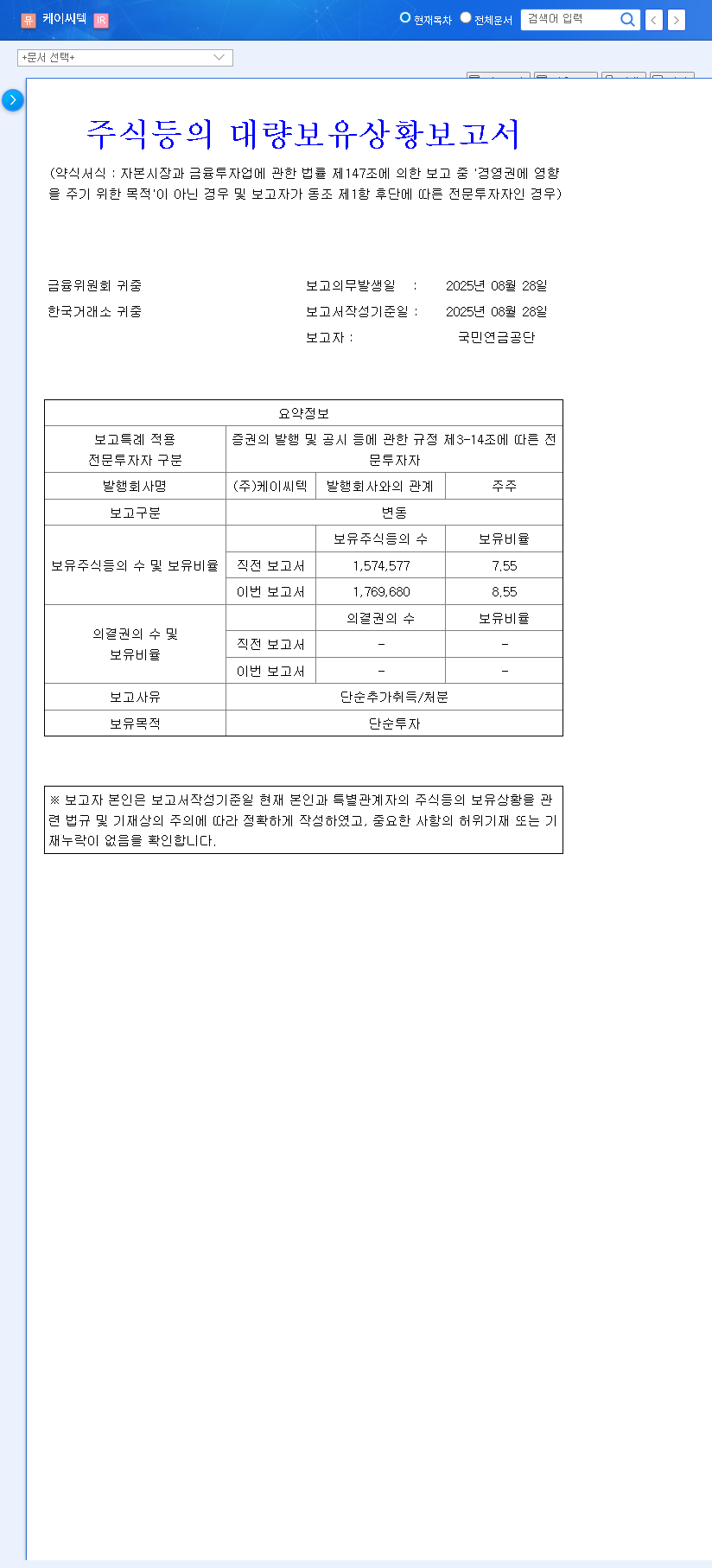

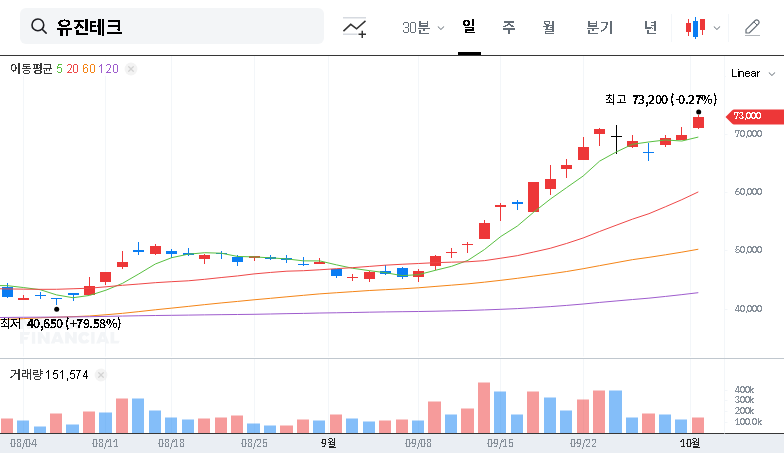

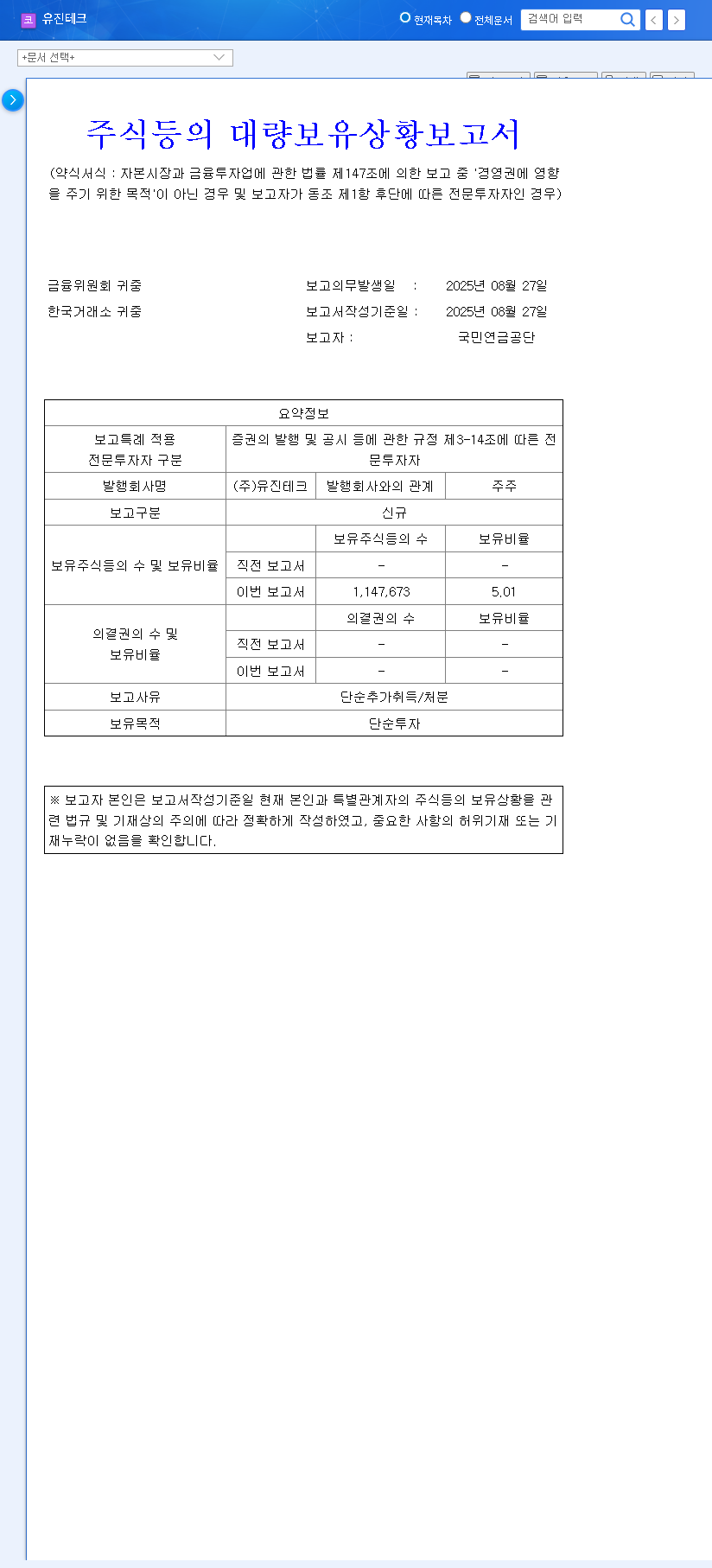

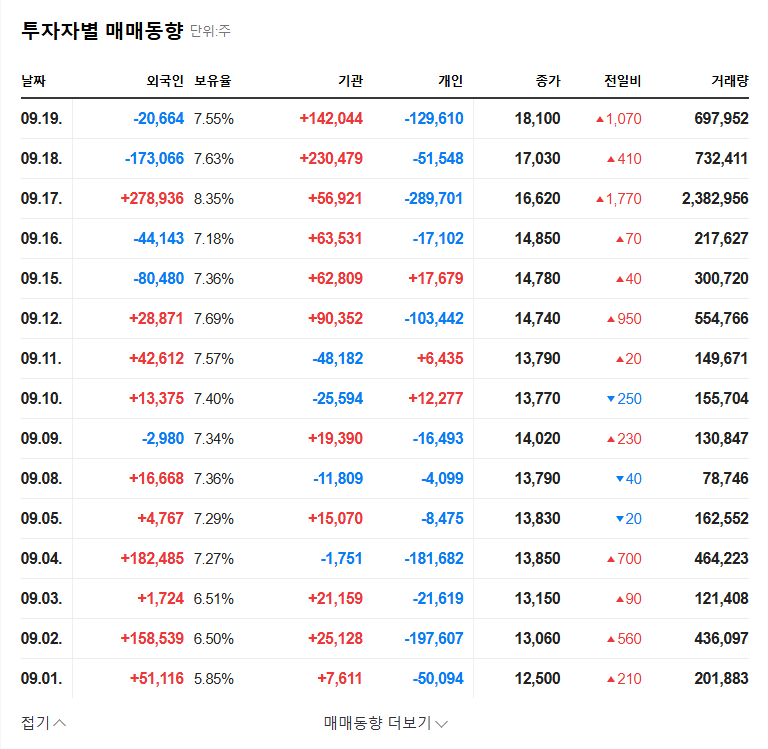

On October 1, 2025, KC Tech, a key player in the semiconductor and display equipment sector, disclosed that the National Pension Service had increased its ownership from 7.55% to 8.55%. This 1%p increase, detailed in an Official Disclosure with the Financial Supervisory Service, represents a multi-million dollar vote of confidence. For investors analyzing the KC Tech stock, understanding the ‘why’ behind this investment is crucial for forecasting its future trajectory.

Deep Dive Analysis: The Fundamentals Driving the Investment

The NPS’s decision wasn’t made in a vacuum. It’s rooted in a thorough analysis of KC Tech’s core business strengths and financial health, weighed against its challenges.

The Growth Engine: A Booming Semiconductor Segment

The primary driver for optimism is KC Tech’s semiconductor business. The insatiable global demand for chips, fueled by the expansion of AI, cloud computing, and big data infrastructure, has created a super-cycle for equipment and materials suppliers. KC Tech is well-positioned to capitalize on this trend. Its continuous R&D investment into next-generation technologies ensures its relevance as chipmakers push the boundaries of fabrication. This robust growth in its core segment likely forms the bedrock of the NPS’s positive long-term outlook on the KC Tech stock.

Rock-Solid Financials: A Foundation of Stability

In a volatile market, stability is a premium. KC Tech boasts an exceptionally strong balance sheet, highlighted by a very low debt-to-equity ratio of just 11%. This financial prudence means the company is not heavily burdened by interest payments and has significant flexibility to navigate economic downturns or invest strategically in growth opportunities. Its substantial liquid assets provide a further cushion, making it a resilient choice for a risk-conscious institutional investor like the NPS.

The Headwind: Navigating the Display Sector Slump

However, the picture is not entirely rosy. The company’s display equipment segment has faced significant headwinds. Intense competition, particularly from Chinese manufacturers, and a cyclical reduction in capital expenditures by major panel makers have led to a noticeable decline in sales. This underperformance has been a drag on the company’s overall net profit and is a key risk factor that investors must monitor closely.

While the semiconductor segment soars, the sluggish display business remains a critical variable. A strategic turnaround or stabilization in this area could unlock significant upside for KC Tech stock.

The Bull vs. Bear Case: What’s Next for KC Tech Stock?

The NPS investment sharpens the debate between the bullish and bearish outlooks for KC Tech.

- •The Bull Case: The ‘smart money’ has spoken. The NPS stake increase provides powerful institutional validation, which can attract other investors and lead to a positive re-rating of the stock. Bulls argue that the market is undervaluing the high-growth semiconductor business by focusing too heavily on the struggling display segment. The long-term secular trends in AI and data firmly support KC Tech’s core competency.

- •The Bear Case: Bears caution that the display segment’s continued weakness could cap profit growth and offset gains from the semiconductor side. Furthermore, the semiconductor industry itself is notoriously cyclical. A global economic slowdown or geopolitical tensions could disrupt demand. Therefore, the stock’s performance is tied not only to company execution but also to broader macroeconomic conditions.

Action Plan: Key Metrics for Investors to Watch

For those considering an investment in KC Tech stock, a proactive monitoring approach is essential. Here are the key points to focus on:

- •Display Segment Strategy: Watch for any company announcements regarding restructuring, new technology, or market share gains in the display business. A turnaround here is a major bullish catalyst.

- •Semiconductor Industry Health: Follow reports from authoritative bodies like SEMI (Semiconductor Equipment and Materials International) on global chip demand and capital expenditure forecasts.

- •Quarterly Earnings Reports: Scrutinize margin performance in both business segments. Strong and sustained profitability in the semiconductor division is crucial to the investment thesis.

- •Broader Market Context: To make a fully informed decision, it’s helpful to understand how to analyze semiconductor stocks within the wider industry landscape.

In conclusion, the National Pension Service’s increased investment in KC Tech stock is a compelling, positive signal backed by the company’s strong semiconductor business and solid financials. While the challenges in the display sector should not be ignored, the long-term growth trajectory appears promising. Careful monitoring of the key metrics outlined above will be essential for navigating this investment opportunity successfully.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. All investment decisions should be made based on your own research and risk tolerance.