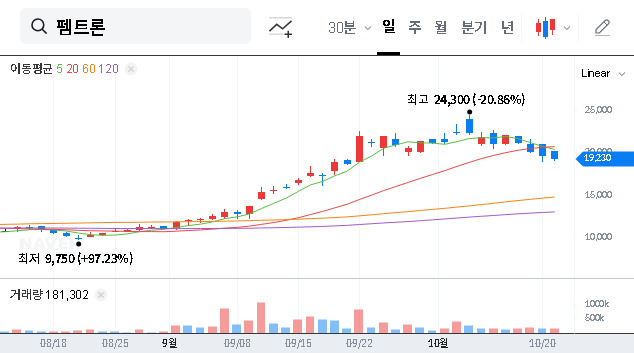

The upcoming PEMTRON IR (Investor Relations) briefing, scheduled for October 22, 2025, is poised to be a pivotal event for investors. As a key player in the advanced inspection equipment industry, PEMTRON Corporation is set to unveil its current performance and future strategic vision. With market anticipation building, this briefing could significantly influence the PEMTRON stock price and redefine its trajectory.

This comprehensive guide will delve into what investors should expect from the PEMTRON IR, analyze potential outcomes, and provide an actionable strategy to navigate the post-event market landscape. We will explore the details, assess the stakes, and help you make informed decisions to protect and grow your investment.

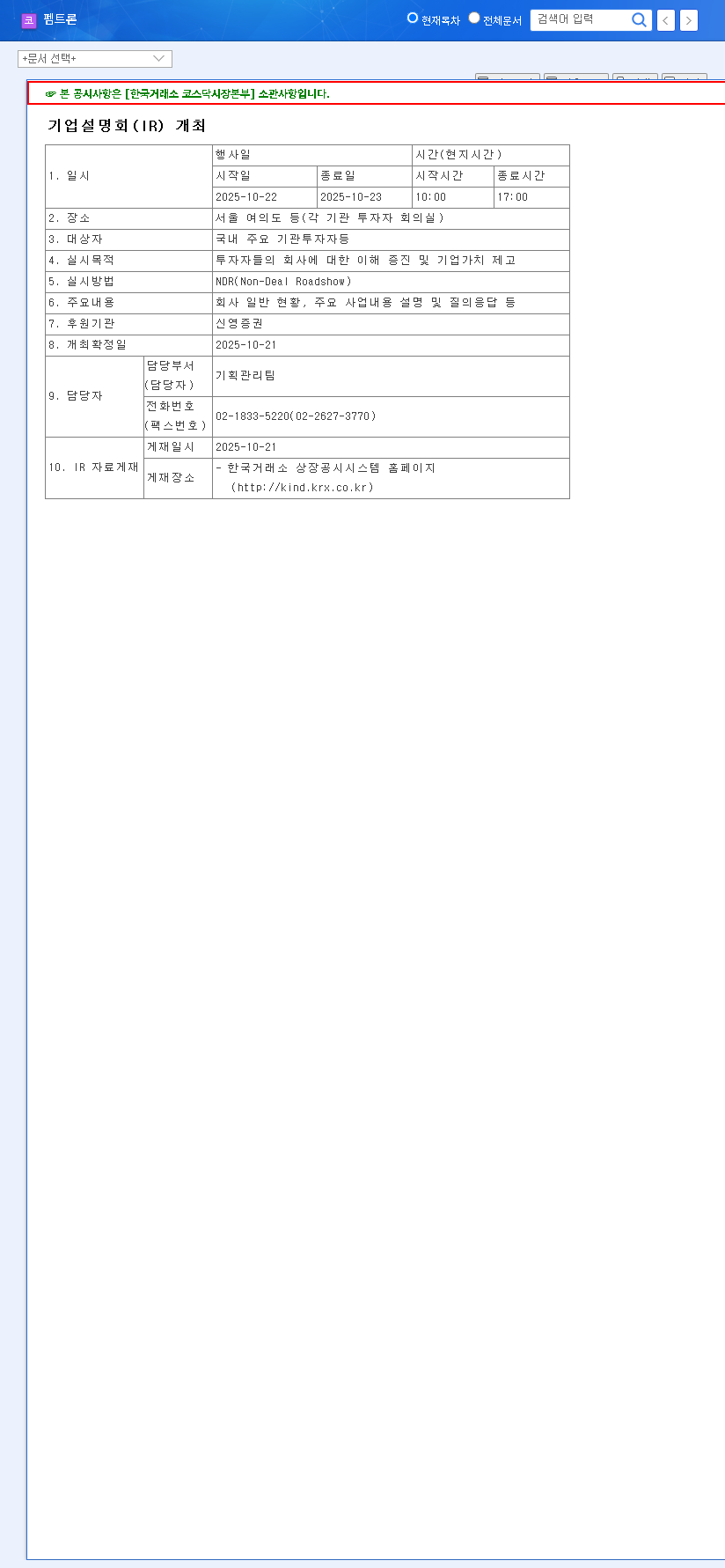

Event Details: The October 2025 PEMTRON IR Briefing

PEMTRON Corporation has formally announced its investor relations event, a critical communication channel between the company’s management and its shareholders. Here are the key details:

- •Date: October 22, 2025

- •Time: 10:00 AM

- •Agenda: A comprehensive overview of the company’s current business status, strategic initiatives, financial health, and a forward-looking vision, followed by a live Q&A session.

The primary purpose of this investor briefing is to bridge the information gap, enhance transparency, and ultimately boost long-term corporate value. For official details, investors can refer to the company’s filing. Source: Click to view DART report.

Given the current lack of detailed brokerage reports and defined market expectations, this IR event is not just an update; it’s a critical moment that could set the tone for PEMTRON’s valuation for months to come.

Potential Scenarios for the PEMTRON Stock Price

The market’s reaction to the PEMTRON IR will hinge on the substance and clarity of the information presented. Here are three potential scenarios that could unfold, impacting the PEMTRON stock price.

Positive Impact Scenarios

A successful IR could lead to a significant uptick. This might be triggered by:

- •Visionary Growth Strategy: Unveiling a clear, ambitious plan for new market entry, technological innovation (e.g., next-gen 3D inspection tech), or major R&D breakthroughs.

- •Major Contract Wins: Announcing new, high-value partnerships or contracts with industry leaders, validating their competitive edge.

- •Strong Financial Outlook: Presenting better-than-expected earnings guidance or a robust financial position that resolves investor uncertainty.

- •Confident Q&A Session: Management’s ability to answer tough questions with clarity and confidence can build immense trust.

Negative Impact Scenarios

Conversely, the IR could disappoint the market if it reveals:

- •Underwhelming Guidance: A cautious or downwardly revised forecast for future revenue or profitability could trigger a sell-off.

- •Unexpected Challenges: Disclosure of operational issues, competitive threats, or supply chain disruptions that were not previously priced in by the market.

- •Evasive Q&A Responses: Vague or ambiguous answers from leadership can erode investor confidence and be interpreted as hiding negative information.

Neutral Impact Scenarios

It’s also possible for the event to have a muted short-term effect on the PEMTRON Corporation stock if the content is largely procedural. This occurs when the presentation simply reiterates publicly known information without providing any new, substantive insights or failing to address the core questions investors have. While not negative, it represents a missed opportunity to build positive momentum.

Investor Action Plan: What to Do Before and After the IR

Preparation is key. Here’s a strategic plan for investors to maximize their understanding and make sound decisions based on the outcome of the PEMTRON IR.

- •Analyze the Presentation Deeply: Don’t just skim the slides. Scrutinize the details of the business model, financial projections, and growth levers presented. Compare the new information against previous statements.

- •Evaluate the Q&A Session: The questions from analysts and investors often highlight key market concerns. Pay close attention to the tone, confidence, and specificity of the management’s responses.

- •Monitor Market Reaction: Observe trading volume and price action immediately following the IR. Also, watch for new reports from financial analysts. For context, you can compare this to general market analysis from authoritative sources like Bloomberg.

- •Re-evaluate Company Fundamentals: Use the newly disclosed information to update your investment thesis. Does the IR reinforce or challenge your reasons for holding the stock? To learn more, read our guide on How to Analyze a Tech Company’s Fundamentals.

Frequently Asked Questions (FAQ)

Q1: When is the PEMTRON Corporation IR event?

A1: The investor relations briefing is scheduled for October 22, 2025, at 10:00 AM.

Q2: What is the main goal of this PEMTRON IR?

A2: The primary objective is to improve investor understanding of the company’s operations, strategy, and financial health, thereby enhancing corporate value and transparency.

Q3: What are the key factors that could positively affect the PEMTRON stock price?

A3: Positive catalysts include the announcement of a strong growth vision, new major contracts, better-than-expected financial guidance, and a confident, transparent Q&A session with management.

Q4: What should I focus on immediately after the investor briefing concludes?

A4: Immediately after, you should analyze the presentation content, review the Q&A for underlying sentiment, monitor the market’s initial reaction (price and volume), and begin re-evaluating PEMTRON’s fundamental value based on the new data.