This comprehensive analysis of the S-Oil Corporation earnings for the third quarter of 2025 unpacks a complex financial story. While the South Korean refining giant surpassed revenue expectations, its bottom-line profitability came under significant pressure, falling short of market consensus. This raises critical questions for investors: Is this a temporary setback or a sign of deeper structural issues? We will explore the macroeconomic headwinds, segment-specific performance, and long-term strategic projects to provide a clear outlook and an actionable S-Oil investment thesis.

S-Oil Q3 2025 Results: The Official Numbers

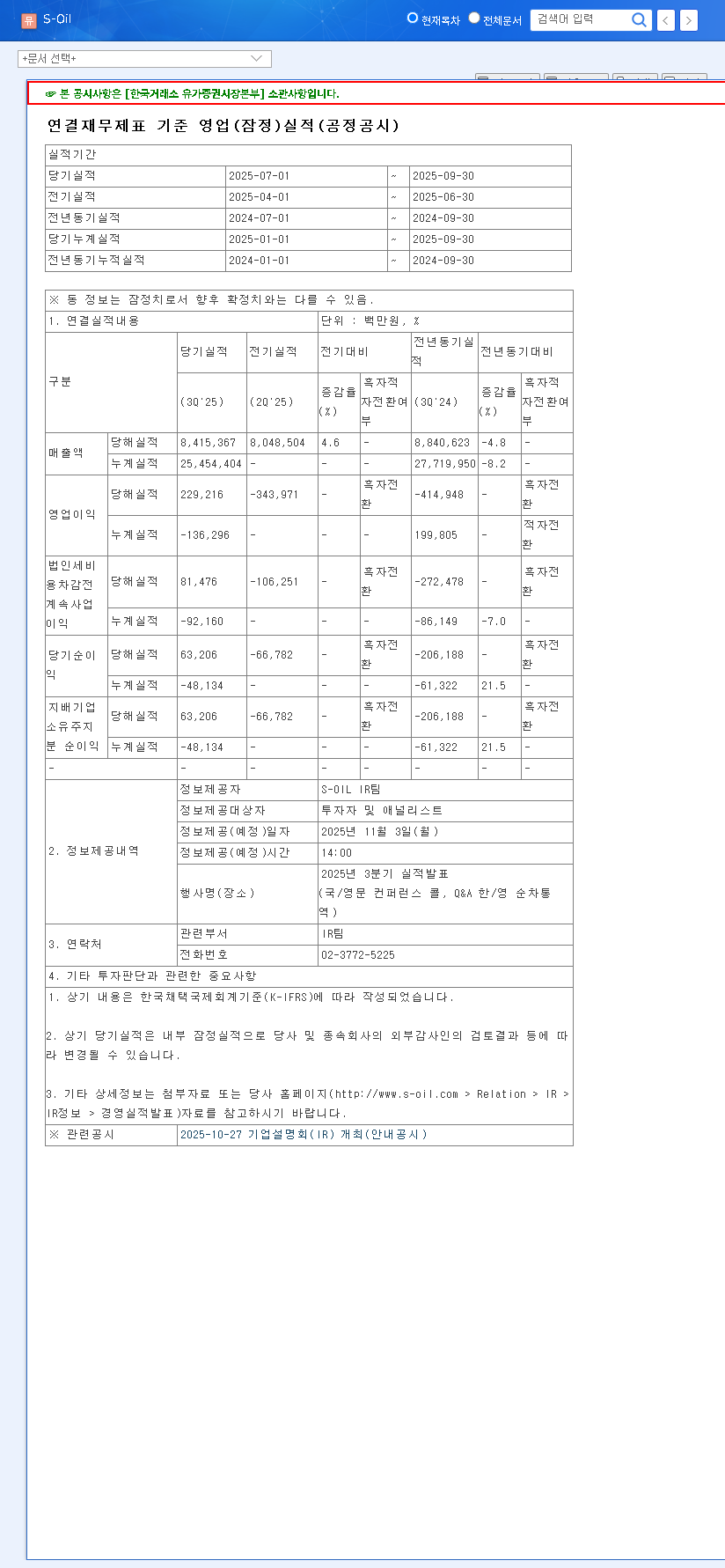

On November 3, 2025, S-Oil Corporation released its provisional Q3 earnings, painting a mixed picture. The company successfully swung back to profitability after a substantial loss in the second quarter, but key metrics reveal ongoing challenges in the operating environment. The full details can be verified in the Official Disclosure (DART).

Here is a summary of the key performance indicators from the S-Oil Corporation earnings report:

- •Revenue: KRW 8.4154 trillion, which was 3% above the market estimate of KRW 8.1879 trillion.

- •Operating Profit: KRW 229.2 billion, falling 2% below the market estimate of KRW 233.7 billion.

- •Net Profit: KRW 63.2 billion, a significant 10% miss compared to the market estimate of KRW 70.2 billion.

The revenue beat suggests resilient demand, but the disappointing profit figures highlight the severe impact of external market forces on the company’s margins and overall S-Oil profitability.

Why the Disconnect? Analyzing the Headwinds

S-Oil’s Q3 performance was shaped by a confluence of challenging macroeconomic conditions and mixed results across its core business units. Understanding these factors is crucial for any accurate S-Oil stock analysis.

Macroeconomic Volatility: A Perfect Storm

The global economic environment in Q3 2025 was far from stable. Fluctuations in oil prices, currency exchange rates, and interest rates created significant headwinds. International oil prices, a primary driver of S-Oil’s costs and revenue, exhibited high volatility, making profitability forecasts difficult. As tracked by agencies like the U.S. Energy Information Administration (EIA), such price swings directly impact refining margins. Furthermore, the Korean Won’s depreciation against the US Dollar (from 1,354.00 to 1,439.70 KRW/USD) inflated the cost of importing crude oil, directly squeezing profit margins. Rising shipping costs, indicated by the Baltic Dry Index, further compounded these cost-side pressures.

A Segment-by-Segment Performance Breakdown

- •Refining: This core segment faced a mixed reality. While demand for light petroleum products remained strong, a global economic slowdown weakened demand for diesel, and overseas market margins were poor.

- •Lubricants: Despite solid demand for high-grade lube base oils, margins were compressed due to industrial slowdowns and an oversupply situation. A slight rebound in Group III products was not enough to offset the broader weakness.

- •Petrochemicals: This segment continues to be a weak point. The startup of new facilities in China has created intense competition and a supply glut for key products like polypropylene (PP) and propylene oxide (PO), severely impacting profitability.

Future Outlook: The Shaheen Project and Long-Term Strategy

Despite the short-term struggles, S-Oil is making massive long-term investments designed to transform its business. The Shaheen Project and the Gas to Gas (GTG) project are central to this strategy. These initiatives will significantly increase the company’s production of high-value petrochemicals, reducing its reliance on the volatile and cyclical refining market. However, these large-scale investments come with increased debt and financial costs, which are expected to weigh on net profit and depreciation expenses in the near term until they become operational in 2026-2027.

While S-Oil’s short-term profitability is under pressure from macroeconomic factors, its long-term strategic investments in petrochemicals aim to create a more resilient and profitable business model for the future.

S-Oil Investment Action Plan

Given the latest S-Oil Q3 2025 results, investors must weigh the immediate challenges against the potential long-term rewards. The stock’s current valuation and deteriorating profitability metrics suggest a cautious approach. The estimated 2025 Price-to-Earnings (PER) ratio of 64.67x is historically high, and the Return on Equity (ROE) is forecast at a very low 1.23%. For context, you can compare these metrics with others in our complete guide to investing in the energy sector.

Positive Factors (Long-Term Upside)

- •Revenue resilience indicates continued strong end-market demand.

- •Successful return to operating profit after a significant Q2 loss.

- •Strategic investments (Shaheen, GTG) provide a clear path to long-term growth.

Negative Factors (Short-Term Risks)

- •Operating and net profits missed estimates, signaling deep margin pressure.

- •Persistent external pressures from oil prices and currency exchange rates.

- •High valuation (PER) and low profitability (ROE) diminish short-term appeal.

The most prudent approach for a potential S-Oil investment at this time appears to be a ‘wait-and-see’ strategy. Investors should closely monitor macroeconomic indicators and the progress of its major projects before committing capital.

Disclaimer: This report is based on publicly available information and is for informational purposes only. All investment decisions are the sole responsibility of the investor.