The initial analysis of the BGF retail Q3 2025 earnings report reveals a significant outperformance of market expectations, sparking conversations about a potential turnaround for the operator of South Korea’s largest convenience store chain, CU. After a challenging first half of the year, BGF Retail (KRX: 282330) has posted robust growth in revenue, operating profit, and net income, suggesting a recovery in its core business fundamentals. This detailed BGF retail analysis will dissect the quarterly results, explore the underlying drivers, evaluate the persistent risks, and offer a strategic outlook for investors monitoring BGF retail stock.

BGF Retail Q3 2025 Earnings: The Key Numbers

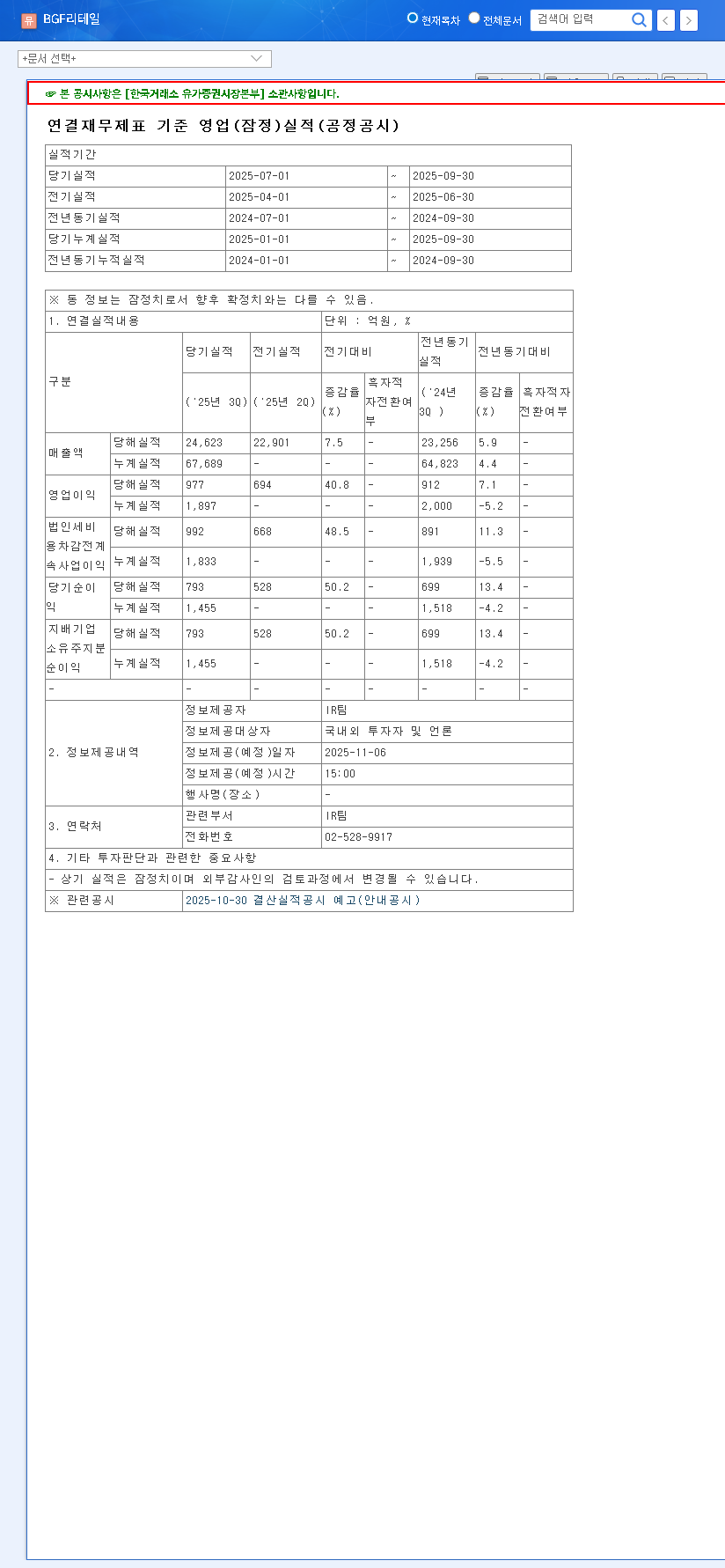

On November 6, 2025, BGF retail CO., LTD. released its preliminary consolidated financials, delivering a pleasant surprise to the market. The results not only showed growth but also confidently surpassed consensus forecasts across the board. You can view the full report directly from the source: Official Disclosure.

Here’s a breakdown of the performance against market expectations:

- •Revenue: KRW 2.4623 trillion, which is 1.0% above the market expectation of KRW 2.4375 trillion.

- •Operating Profit: KRW 97.7 billion, standing 2.2% above the market expectation of KRW 95.6 billion.

- •Net Income: KRW 79.3 billion, a significant 6.2% above the market expectation of KRW 74.7 billion.

The impressive beat in net income is particularly noteworthy, as it suggests stronger-than-anticipated operational efficiency and profitability management during the quarter.

The Q3 2025 results serve as a crucial data point, potentially marking an inflection point for BGF Retail. The strong bottom-line performance indicates that the company’s strategic initiatives may be starting to bear fruit, alleviating earlier concerns about margin compression.

Analysis: Why This Earnings Beat Matters

A Clear Reversal from H1 Weakness

The first half of 2025 was a period of concern for BGF Retail investors. A sequential comparison highlights the magnitude of the Q3 recovery:

- •Q3 2025 Operating Profit: KRW 97.7 billion

- •Q2 2025 Operating Profit: KRW 69.4 billion

- •Q1 2025 Operating Profit: KRW 22.6 billion

This sharp upward trend in profitability demonstrates a powerful recovery, moving the company past the operational hurdles seen earlier in the year. This provides a strong foundation for a potential re-rating of the CU convenience store earnings power and, by extension, BGF retail stock.

Strengthening Fundamentals and Core Business Health

Delivering results beyond market predictions in a competitive environment validates BGF Retail’s strong business foundation and adaptability. While specific segment results were not detailed in the preliminary report, the overall profit jump suggests encouraging signs. This likely includes improved performance in the high-margin food manufacturing and distribution segment, a key area that had previously faced profitability challenges. A healthier food sector is vital for long-term growth.

Navigating the Headwinds: Key Risks for Investors

Despite the positive BGF retail Q3 2025 earnings, a prudent investor must remain aware of the potential risks that could impact future performance.

Internal Financial Health and Governance

The company’s balance sheet requires continued monitoring. The debt-to-equity ratio saw an increase to 113.53% in late 2023 from 92.27% the prior year. While manageable, a high debt load can become a significant burden in a high-interest-rate environment, constraining flexibility and pressuring profits. Furthermore, while recent audits have been clean, any history of audit-related issues can make some institutional investors cautious.

External Macroeconomic Pressures

The broader economic climate poses several challenges. The sustained high benchmark interest rates from central banks like the U.S. Federal Reserve and the Bank of Korea increase borrowing costs. Moreover, a volatile currency exchange rate, particularly a weak Korean Won against the US Dollar, can inflate the cost of imported raw materials essential for many in-store products. These factors are critical to watch, as they directly impact the company’s cost structure. For more on this, you can read about the global economic outlook on Reuters. Understanding the broader South Korean retail market is also essential context.

Investment Outlook: Strategic Path Forward

The strong Q3 results are a bullish signal that could provide a short-term boost to the BGF retail stock price. It effectively counters the narrative of decline from the first half of the year. However, a long-term investment decision requires a more nuanced view.

Investors should look for confirmation of this recovery in the upcoming Q4 2025 and Q1 2026 reports. Key factors to monitor will be the sustainability of profit margin improvements, management’s strategy for debt reduction, and tangible progress in new growth areas, such as overseas expansion and digital initiatives. A long-term perspective, combined with diligent monitoring of these key performance indicators, will be the most effective strategy for making sound investment decisions regarding BGF Retail.