The latest RAYENCE 228850 earnings report for Q3 2025 has captured the attention of the market, presenting a complex picture for investors. While top-line revenue growth faltered, the company delivered a significant ‘earnings surprise’ with profitability metrics that far outpaced analyst expectations. This development marks a potential turning point after several challenging quarters.

Is this rebound in profit a sustainable sign of a fundamental recovery, or a temporary bright spot? This comprehensive analysis breaks down the RAYENCE Q3 2025 performance, explores the underlying causes, and outlines a strategic action plan for both short-term traders and long-term investors. We aim to provide the critical insights needed for your informed investment decisions regarding RAYENCE stock.

RAYENCE Q3 2025 Earnings: The Detailed Breakdown

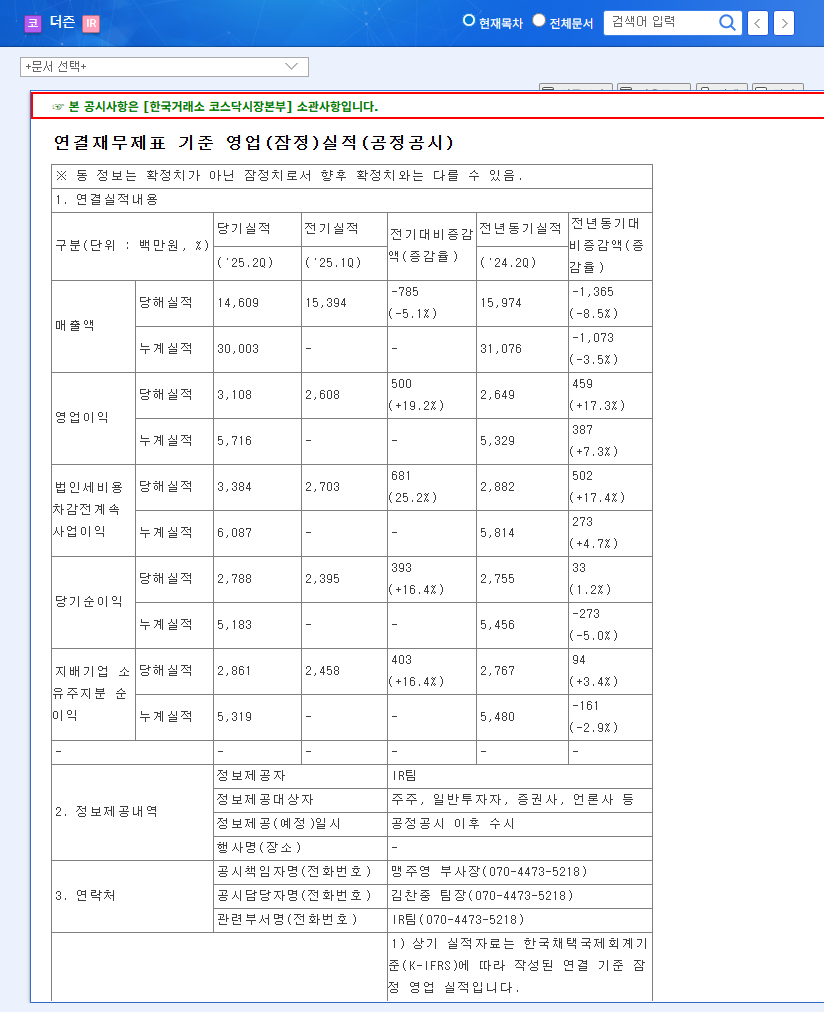

On November 10, 2025, RAYENCE CO.,LTD. (228850) released its preliminary Q3 earnings, revealing a notable divergence between its revenue and profit figures. According to the Official Disclosure, the key metrics were as follows:

- •Revenue: KRW 29.3 billion, which was a 3.3% miss compared to the market consensus of KRW 30.3 billion.

- •Operating Profit: KRW 1.0 billion, a significant 25.0% beat over the forecast of KRW 0.8 billion.

- •Net Profit: KRW 2.5 billion, more than doubling expectations with a massive 108.3% beat over the KRW 1.2 billion forecast.

This performance indicates that while the company struggled with sales volume or pricing, it managed its operational efficiency and cost structure exceptionally well during the quarter. The positive surprise in profitability is a crucial signal that management’s strategic initiatives may be taking hold.

Analysis: The ‘Why’ Behind the Numbers

A Break from a Negative Trend

The Q3 results represent a vital inflection point. RAYENCE had been grappling with a period of decline, posting operating losses from Q4 2024 through Q2 2025. The return to profitability is the first concrete sign of a potential turnaround. This shift is likely attributable to aggressive cost-cutting measures, improved supply chain management, and potentially favorable foreign exchange movements, rather than a rebound in its core detector business segments (TFT and CMOS), which have faced stiff competition and pricing pressure.

While the revenue decline remains a concern, the impressive leap in profitability demonstrates strong operational discipline. This is a critical first step in rebuilding investor confidence in the RAYENCE investment strategy.

Macroeconomic Tailwinds

The broader economic environment may have provided some support. A rising KRW/USD exchange rate can boost the value of international sales when converted back to Korean Won. Furthermore, as noted in recent global economic reports, stabilizing interest rates and declining freight costs help alleviate pressure on borrowing and logistics expenses, directly benefiting the bottom line. These external factors, combined with internal efforts, created a powerful combination for profit recovery in Q3.

Future Outlook and Investor Action Plan

The key question following the RAYENCE 228850 earnings report is whether this momentum is sustainable. A sound investment strategy requires a nuanced view, balancing short-term opportunities with long-term risks.

Short-Term Strategy (1-3 Months)

The positive earnings surprise is likely to generate favorable investor sentiment and could trigger a technical rebound in the stock price. Traders might look for short-term gains, but should remain cautious. The underlying revenue weakness has not been resolved. A prudent approach would be to capitalize on any upward momentum while setting strict stop-loss orders to manage the inherent volatility.

Mid-to-Long-Term RAYENCE Investment Strategy (6-18+ Months)

For a long-term investment, profitability must be paired with growth. The focus now shifts to whether RAYENCE can address its fundamental challenges. Investors should monitor the following:

- •Revenue Growth: Watch for a stabilization and subsequent increase in sales in the upcoming quarterly reports. This is non-negotiable for long-term health.

- •Innovation Pipeline: Assess the company’s R&D efforts. Are they developing new, high-value-added products to regain a competitive edge in the detector market?

- •Market Diversification: Look for evidence that RAYENCE is reducing its dependence on specific large customers and expanding into new geographic or industrial markets. For more on this, see our guide to diversification in tech portfolios.

A long-term RAYENCE stock analysis suggests a cautious but watchful stance. A phased buying approach could be considered if the company demonstrates consistent progress on these fundamental fronts over the next two to three quarters.

Conclusion: A Cautious Optimism

RAYENCE’s Q3 2025 earnings report is a story of two halves: concerning revenue trends offset by stellar profitability. While the short-term outlook has brightened, the long-term success of the company hinges on its ability to reignite top-line growth and strengthen its competitive position. Investors should closely monitor upcoming quarters for signs that this operational turnaround is translating into genuine, sustainable business momentum.

Disclaimer: This analysis is for informational purposes only and is based on publicly available data. Investors are responsible for their own investment decisions.