The upcoming Samsung SDS Q3 earnings briefing, scheduled for October 30, 2025, is a pivotal event for investors. As a leader in IT services and logistics, Samsung SDS (018260) is increasingly betting its future on high-growth sectors like artificial intelligence and cloud computing. This analysis will dissect the company’s current financial health, explore the potential market impact of the Q3 results, and provide a strategic outlook for those considering a Samsung SDS investment.

We’ll delve into the key growth drivers, identify potential risks, and outline what stakeholders should be listening for during the call to make informed decisions about the future of Samsung SDS stock.

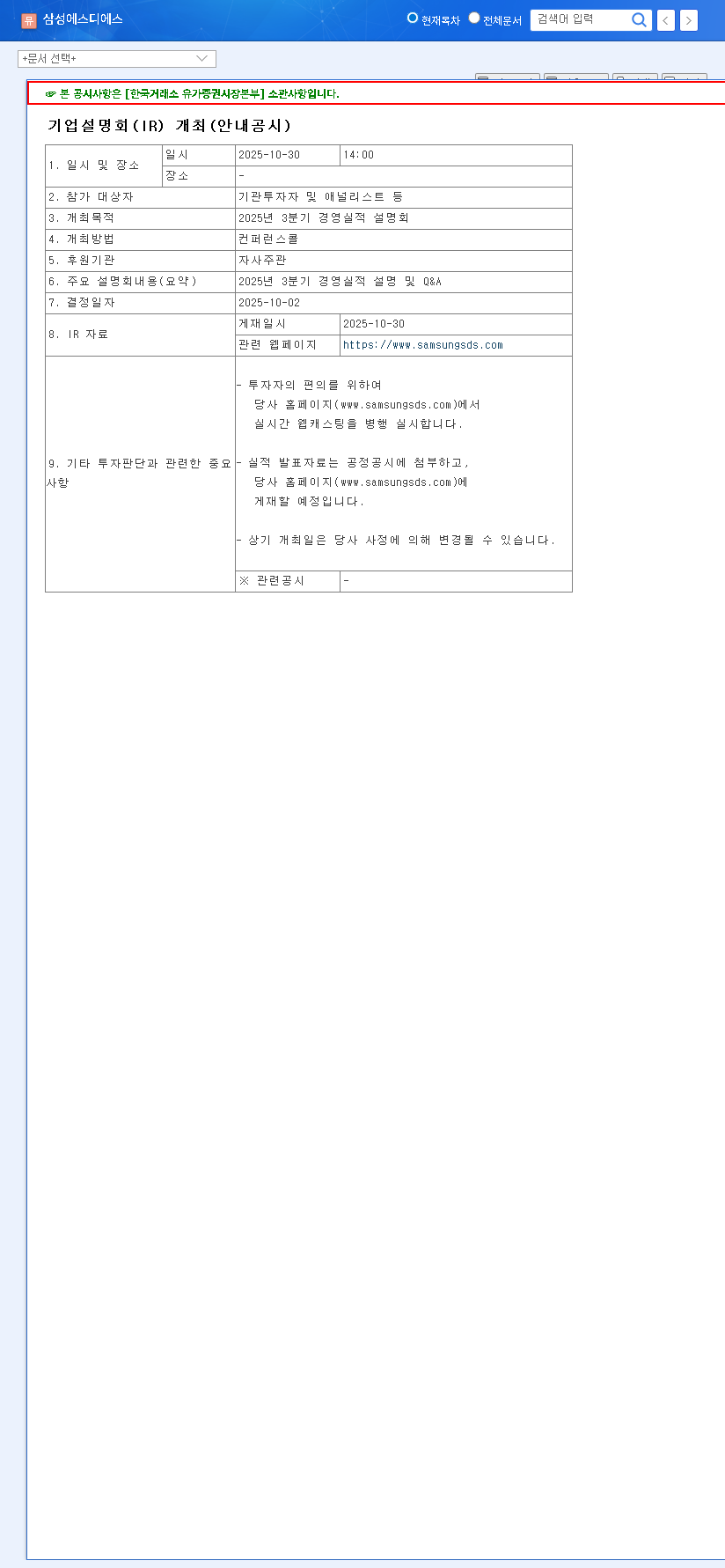

Event Snapshot: Samsung SDS Q3 Earnings Call

Mark your calendars: Samsung SDS will present its Q3 2025 financial results and business outlook on October 30, 2025, at 2:00 PM KST. This briefing is more than just a numbers report; it’s a critical opportunity for management to articulate their strategy, particularly concerning the performance and roadmap for their burgeoning AI and cloud divisions. The subsequent Q&A session will offer invaluable, direct insights into the company’s trajectory.

Fundamental Analysis: Growth Drivers & Key Risks

Powering Growth with Samsung SDS AI and Cloud

The core of the investment thesis for Samsung SDS revolves around its successful transition into a next-generation technology provider. The company’s focus on Samsung SDS AI and Samsung SDS cloud services is not just a talking point; it’s a significant revenue driver. The IT Services division’s growth, which outpaced the logistics arm in H1 2025, was largely fueled by cloud adoption.

Key platforms to watch are the generative AI offerings: FabriX (an enterprise collaboration platform) and Brity Copilot (an AI-powered work assistant). Their adoption rates and monetization strategies will be a focal point of the Q3 earnings call.

Furthermore, the expansion of its GPU-as-a-Service (GPUaaS) offering positions Samsung SDS to capitalize on the insatiable demand for AI-driven computational power. Investors should look for concrete metrics on customer acquisition and revenue contribution from these new technology ventures. To understand the broader market, you can explore market trends in cloud computing for more context.

Financial Stability vs. Profitability Challenges

Financially, Samsung SDS stands on solid ground. A consolidated debt-to-equity ratio of 33.23% indicates low leverage and a resilient balance sheet. Consistent investment in R&D (1.54% of sales) further reinforces its commitment to innovation. For a complete financial overview, investors can review the Official Disclosure on DART.

However, headwinds exist that could affect the Samsung SDS stock price:

- •Logistics Margin Pressure: The logistics division’s operating profit margin (13.8%) lags behind the IT services unit. Any failure to present a clear path to improving profitability could weigh on investor sentiment.

- •Regional Disparities: A reported 8.2% revenue decrease in China highlights geopolitical and economic risks. The company must address its strategy for navigating these challenging markets.

- •Macroeconomic Factors: Global economic slowdowns, persistent high-interest rates, and currency fluctuations are external risks that require savvy management and hedging strategies.

Potential Scenarios Following the Q3 Earnings Call

Positive Scenario (Bull Case)

If Q3 results significantly beat expectations, showcasing accelerated growth in the Samsung SDS cloud and AI divisions, the stock could see a substantial rally. A positive surprise would be concrete evidence of FabriX and Brity Copilot gaining major enterprise clients, coupled with a clear, actionable plan to boost logistics profitability. This would signal strong execution and validate the company’s long-term growth narrative.

Neutral Scenario (Base Case)

An in-line earnings report that meets market consensus would likely keep the stock price stable. In this scenario, the company demonstrates steady, continued growth in its core businesses. The focus would be on management’s forward-looking guidance. Positive commentary on the AI pipeline and a stable outlook for the logistics sector would reinforce confidence, preventing any significant sell-off.

Negative Scenario (Bear Case)

Downward pressure on the Samsung SDS stock is likely if Q3 results miss expectations or if guidance is weak. Key triggers for a negative reaction would include a slowdown in cloud revenue growth, an admission of slower-than-expected adoption of AI platforms, or a further deterioration in logistics margins without a credible solution. This would raise concerns about the company’s ability to navigate the competitive landscape and macroeconomic challenges.

Investor Action Plan & Strategic Outlook

The Samsung SDS Q3 earnings report is a critical data point. For long-term investors, the key is to look beyond a single quarter’s results and focus on the strategic trajectory. The company’s push into generative AI is a high-potential area; to learn more about generative AI platforms, see our related analysis.

Investment Opinion: Neutral with a Positive Long-Term Bias. While short-term volatility is expected around the earnings release, the company’s solid financial footing and strategic investments in AI and cloud create a compelling long-term growth story. We recommend that investors carefully analyze the Q3 report and management’s commentary before making new investment decisions. Pay closest attention to the growth rate of high-margin IT services and any specific progress on improving logistics profitability.

Disclaimer: This analysis is for informational purposes only and is based on publicly available information. Investment decisions should be made based on individual research and consultation with a financial advisor.