As November 4th approaches, the global gaming industry and financial markets are laser-focused on the upcoming KRAFTON Q3 earnings announcement. This event is more than a routine financial update; it’s a critical barometer for the health of the PUBG: BATTLEGROUNDS empire, a litmus test for the company’s diversification strategies, and a key indicator for KRAFTON stock performance. For investors, understanding the nuances of this report is essential for making informed decisions.

This in-depth analysis will break down the core fundamentals, market dynamics, and critical points to watch during the KRAFTON earnings call. We’ll explore both the immense potential and the significant risks, providing a clear action plan for navigating the results.

Event Overview: The KRAFTON Q3 Earnings Announcement

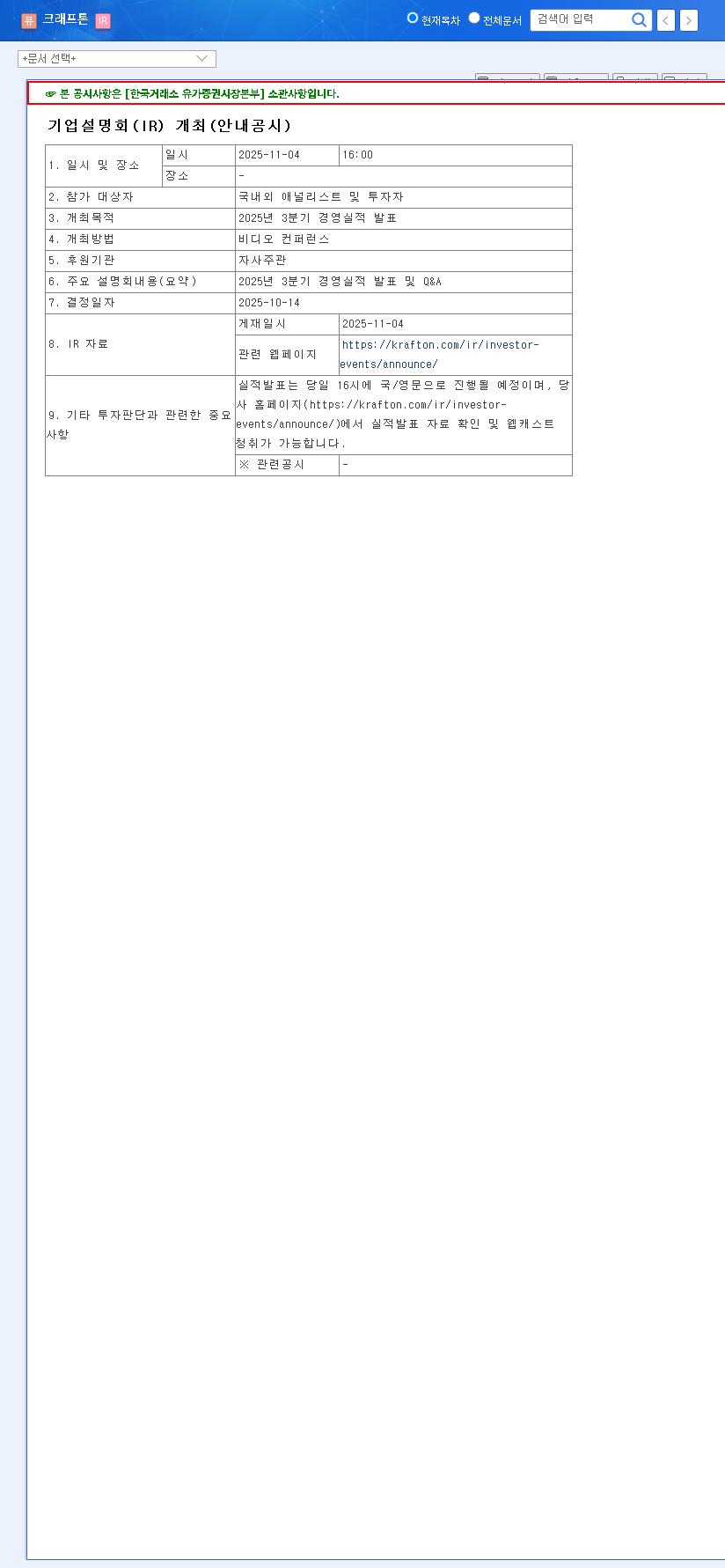

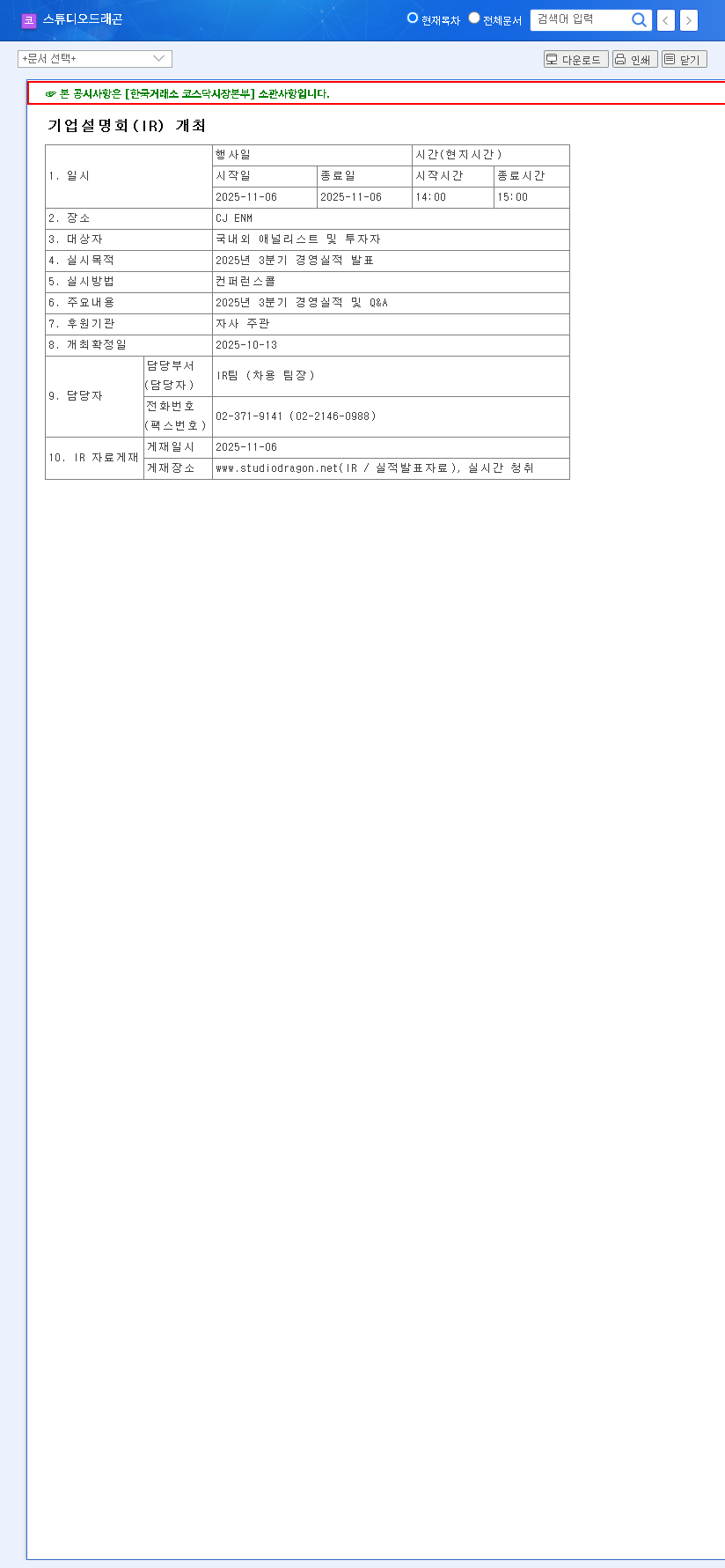

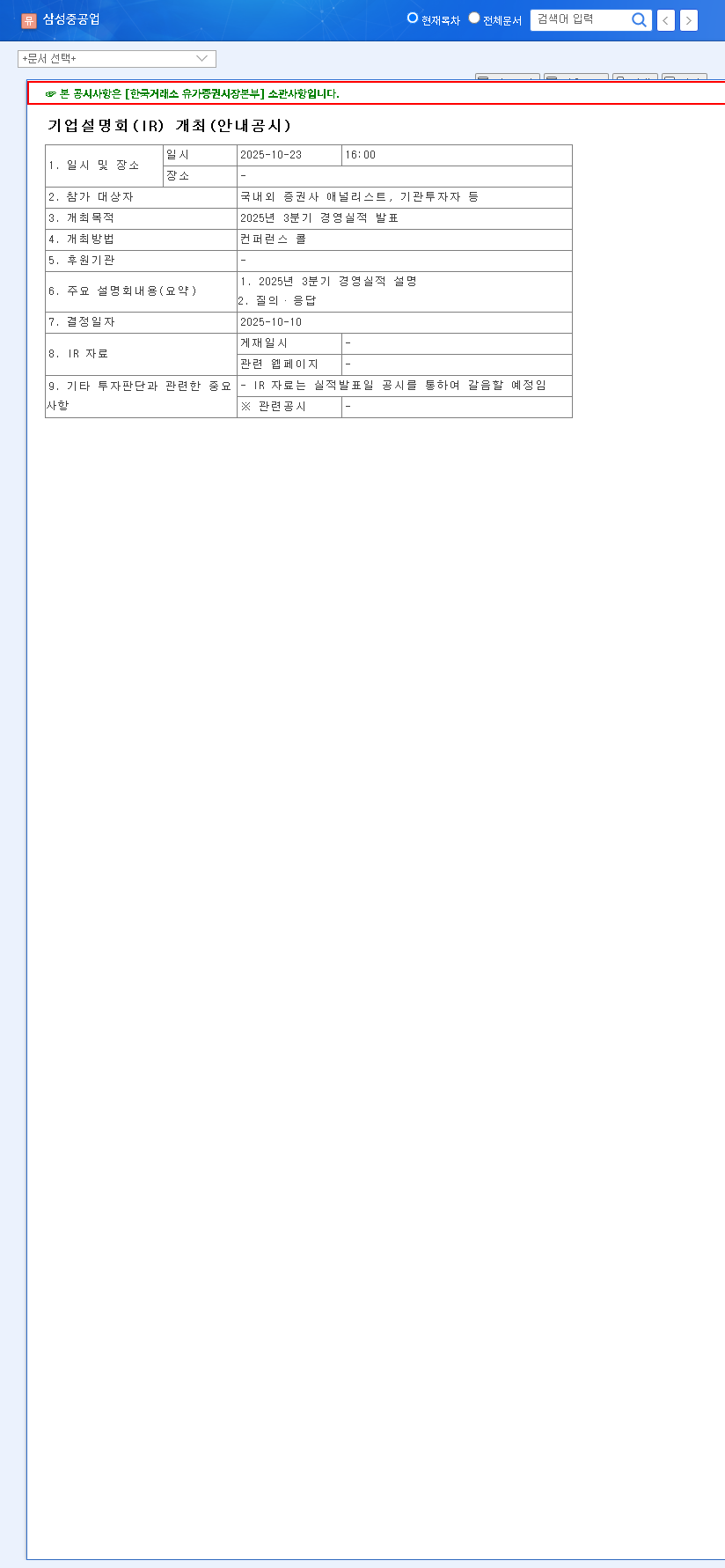

KRAFTON, Inc. has officially scheduled its Q3 2025 earnings presentation and subsequent investor Q&A session for November 4, 2025, at 16:00 KST. During this pivotal event, the company’s leadership will disclose its comprehensive KRAFTON financial results for the third quarter and provide forward-looking guidance. For official documentation, investors can reference the public filing. Official Disclosure: Click to view DART report.

The first half of 2025 set a positive tone, with consolidated revenue reaching KRW 1.5362 trillion. This growth was overwhelmingly powered by the mobile segment, which contributed 62.5% of total revenue. Furthermore, with 95% of sales generated internationally, KRAFTON’s global footprint remains a core strength.

The central question for investors is whether the mobile segment’s phenomenal growth can continue to offset the headwinds facing the PC/console division and fuel the company’s ambitious expansion into new technologies like AI.

Fundamental Analysis: Strengths and Weaknesses

Core Strengths Fueling Growth

- •Dominant Mobile Performance: The mobile ecosystem built around the Battlegrounds IP is a juggernaut, consistently driving revenue and user engagement across the globe.

- •Global IP Powerhouse: KRAFTON’s strategy to expand its core IP into new games, media, and entertainment verticals presents significant long-term upside potential.

- •Future-Proofing with AI: Proactive investments in artificial intelligence and deep learning are not just buzzwords; they represent a tangible competitive advantage for future game development and operational efficiency. You can explore more on our internal analysis of KRAFTON’s technology investments.

- •Rock-Solid Financials: A strong balance sheet with substantial cash reserves gives KRAFTON the flexibility to pursue strategic M&A and weather economic downturns.

Key Risks and Headwinds

- •PC & Console Segment Decline: This is a critical concern. Intense global competition has led to sagging revenue in this segment, placing immense pressure on the upcoming slate of new titles to perform.

- •Forex Volatility: With 95% of revenue coming from overseas, fluctuations in foreign exchange rates can have a direct and material impact on the bottom line.

- •Legal and M&A Risks: Ongoing litigation and contingent considerations from past acquisitions introduce an element of financial uncertainty that cannot be ignored.

Market Outlook & Potential Scenarios

The global gaming market continues its growth trajectory, with projections from sources like Newzoo showing mobile gaming as the dominant force. This macro trend is a powerful tailwind for KRAFTON. However, macroeconomic factors like inflation and interest rates could temper consumer spending on in-game items. The KRAFTON Q3 earnings report will provide a crucial data point on how these forces are impacting the company.

The Bull Case (Positive Scenario)

If Q3 earnings decisively beat analyst expectations, particularly with sustained high-margin growth in mobile, the market will react positively. Other catalysts include concrete updates on new IP development, evidence of successful AI integration, and optimistic forward guidance. In this scenario, KRAFTON stock could see a significant upward re-rating.

The Bear Case (Negative Scenario)

Conversely, a miss on revenue or earnings, coupled with a deeper-than-expected slump in the PC/console segment, would likely trigger a sell-off. Further negative factors could include delays in the game pipeline, unforeseen legal costs, or conservative guidance that signals future weakness. This would put significant downward pressure on the stock price.

Investor Action Plan: 4 Questions to Answer

When analyzing the KRAFTON earnings call, investors should seek answers to these four critical questions:

- •1. Is Mobile Growth Sustainable? Look beyond the headline revenue. Are user acquisition and engagement metrics (DAU/MAU) healthy? Is average revenue per user (ARPU) increasing?

- •2. What is the PC/Console Turnaround Plan? Management must provide a clear, credible strategy for reviving this segment. Vague promises won’t suffice; investors need to see a plan for new titles and enhanced live service operations.

- •3. Are New Ventures Delivering ROI? Has the investment in AI started to yield tangible results, such as reduced development costs or new gameplay features? How is the expansion of IP into other media progressing?

- •4. How is Management Handling Macro Risks? Listen for commentary on their hedging strategies against currency fluctuations and their outlook on consumer spending habits in key markets.

Ultimately, investing in KRAFTON requires a long-term perspective. While the Q3 results will cause short-term volatility, the company’s powerful IP, technological prowess, and strong financial position present a compelling case for future growth. Careful analysis of this report is the key to a sound investment strategy.