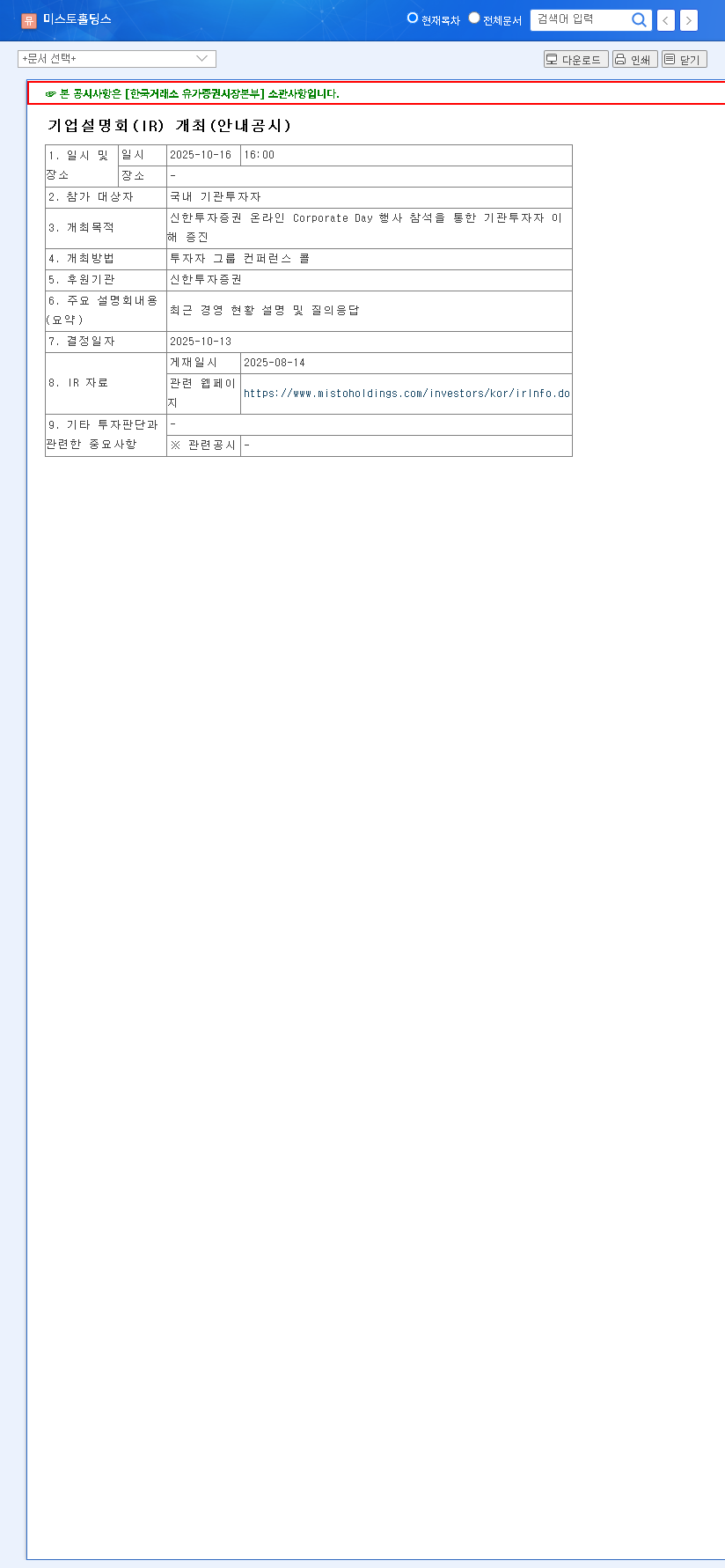

Misto Holdings Corporation is poised for a critical announcement as its Q3 2025 earnings call approaches. Scheduled for November 14, 2025, at 4 PM KST, this Investor Relations (IR) conference will provide vital insights into the company’s recent performance and future trajectory. For investors, this event is more than just a financial update; it’s a key indicator that could significantly influence stock movements. You can view the Official Disclosure on DART for confirmation. This analysis will dissect the company’s strong fundamentals from H1 2025, explore the potential scenarios stemming from the Q3 IR, and highlight the essential points every stakeholder should watch.

Strong Fundamentals: A Recap of H1 2025 Performance

To understand the context for the Q3 announcement, it’s crucial to look at the robust foundation Misto Holdings Corporation built in the first half of 2025. The company demonstrated impressive resilience and growth, driven by a strategic balance between its two core business segments. The consolidated financial performance paints a picture of a healthy, growing enterprise.

Revenue for H1 2025 reached KRW 2,465.2 billion, a solid 4.5% increase year-over-year. This growth was primarily fueled by the Acushnet segment’s outstanding performance, which successfully compensated for a minor decline in the Misto fashion segment. Operating profit saw an even more significant jump, rising 13.6% to KRW 344.6 billion, showcasing enhanced profitability. This was largely due to the Acushnet segment’s high operating margin and the successful turnaround of the Misto segment, which returned to profitability. Consequently, net profit surged by an impressive 29.9% to KRW 290.7 billion.

Segment Deep Dive: The Two Pillars of Misto

Misto Holdings Corporation’s success lies in its diversified structure, balancing the dynamic world of fashion with the stable growth of the golf industry.

The Acushnet Segment: Driving Growth

The Acushnet segment, featuring world-renowned golf brands like Titleist and FootJoy, remains the company’s growth engine. It benefits immensely from the structural expansion of the global golf industry, a trend that has seen sustained participation and interest post-pandemic. According to industry analysis from sources like leading market research firms, the sport’s appeal continues to broaden. Acushnet has capitalized on this by strengthening its market dominance through continuous R&D and strategic marketing, ensuring its products remain the top choice for both professional and amateur golfers.

The Misto Segment: A Strategic Turnaround

The Misto segment, which encompasses fashion and lifestyle brands, has faced a more challenging environment due to weakening global consumer sentiment and trade uncertainties. However, the segment has shown remarkable agility. By leveraging strong brand competitiveness and implementing region-specific strategies, it successfully returned to profitability in H1 2025. Key initiatives include expanding its licensing and distribution business in Greater China and broadening its portfolio into high-growth sports and outdoor categories, positioning it for future growth.

Financial Health and Shareholder Commitment

Beyond strong profits, Misto Holdings Corporation has demonstrated a commitment to financial stability and shareholder value. The company’s debt-to-equity ratio improved to 106.7%, and efficient inventory management led to a 14.1% decrease in inventory levels from the end of the previous year. This indicates a lean, efficient operation. Furthermore, the company has bolstered its shareholder-friendly policies.

The company plans to implement shareholder returns of up to KRW 500 billion over three years (2025-2027) and is actively considering special dividends and share repurchases, signaling strong confidence in its long-term financial health.

Potential Scenarios for the Q3 IR Announcement

With no clear market consensus on Q3 results, the upcoming IR could swing the stock price significantly. Investors should be prepared for several potential outcomes.

The Positive Scenario (Bull Case)

- •Acushnet Exceeds Expectations: If the golf segment reports growth beyond forecasts, it would reaffirm its market leadership and drive positive sentiment.

- •Misto Segment Accelerates: Concrete results from the expansion in emerging markets could signal a new growth phase for the fashion segment.

- •Aggressive Shareholder Returns: An announcement of a specific share repurchase or special dividend could significantly boost investment attractiveness.

The Negative Scenario (Bear Case)

- •Macroeconomic Headwinds: A continued slowdown in global consumer spending could disproportionately affect the Misto segment, leading to missed targets.

- •Currency and Cost Pressures: Unfavorable exchange rate movements (KRW/USD) or rising raw material costs could erode the profitability of the Acushnet segment.

- •Slowing Growth Narrative: Any indication that the Acushnet segment’s rapid growth is decelerating could dampen investor enthusiasm.

Conclusion: Key Points for Investors to Watch

The Misto Holdings Corporation Q3 IR will be a pivotal event. The core narrative will revolve around whether the Acushnet segment can maintain its powerful momentum and how quickly the Misto segment can transition from recovery to robust growth. Investors should pay close attention to the Q&A session for management’s outlook on 2026.

Before making any decisions, it’s wise to review how to analyze quarterly earnings reports to be fully prepared. The market’s reaction in the hours and days following the announcement will be telling. Cautious and informed decision-making based on a thorough analysis of the released data will be paramount.