The recent OE Solutions convertible bond call option exercise has sent ripples through the investment community, prompting a closer look at the company’s stock price trajectory and long-term corporate value. This strategic financial maneuver, while common, presents a complex scenario for current and prospective investors. It raises critical questions about short-term stock dilution versus the long-term benefits of capital infusion.

This comprehensive analysis will dissect the event, evaluate the underlying OE Solutions financials, and provide a clear framework for developing a sound investment strategy. We will explore both the immediate pressures and the potential growth catalysts stemming from this decision.

Decoding the Announcement: The Convertible Bond Exercise Explained

What Exactly Happened?

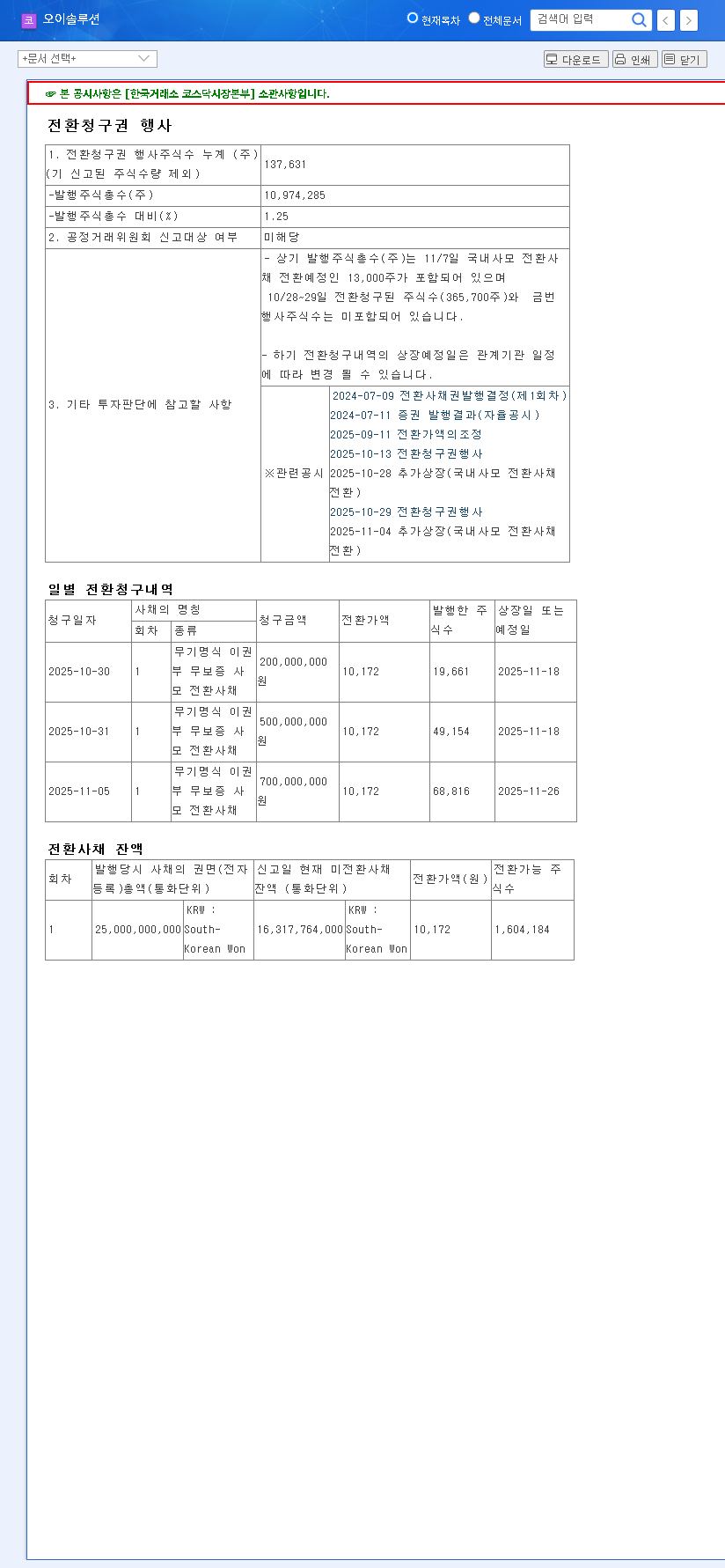

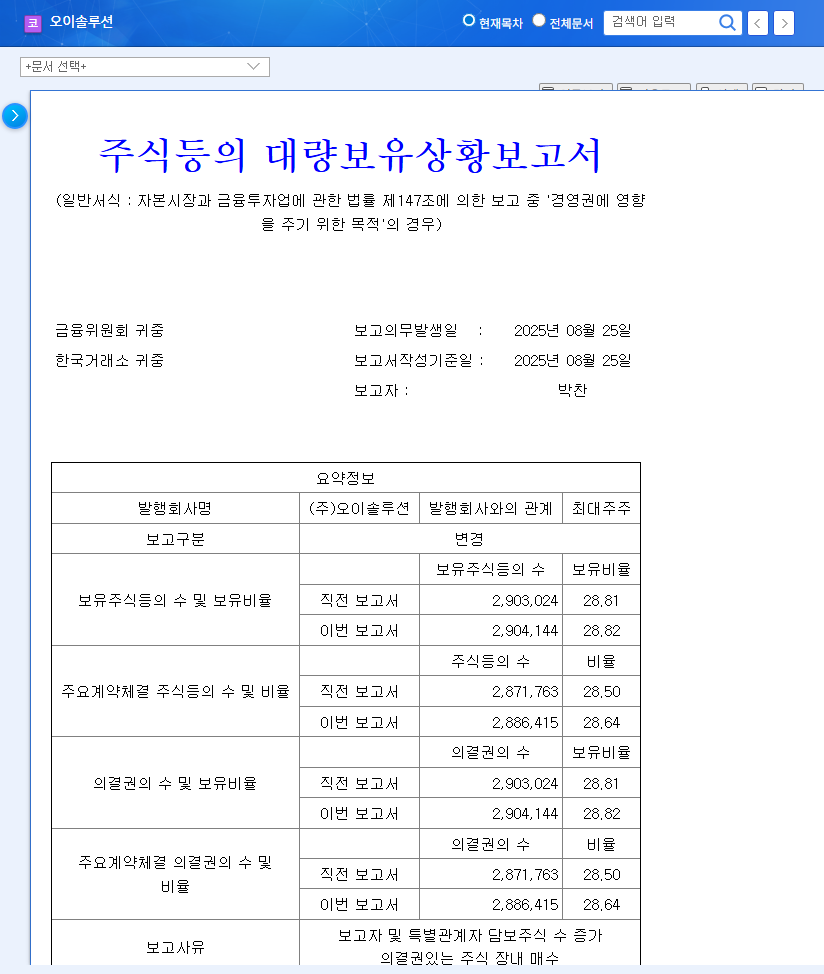

On November 5, 2025, OE Solutions officially announced its decision to exercise call options on its outstanding convertible bonds. In essence, this forces bondholders to either accept a call price for their bonds or convert them into company stock. The key details are as follows:

- •Shares Converted: A total of 137,631 new shares were issued.

- •Conversion Price: The conversion was executed at 10,172 KRW per share.

- •Capital Infusion: This move is projected to inject approximately 1.4 billion KRW into the company.

- •Source: The details were confirmed via an Official Disclosure on DART.

This action is significant because it increases the number of shares outstanding, which has a direct impact on the OE Solutions stock price and the ownership stake of existing shareholders.

A Tale of Two Metrics: Analyzing OE Solutions’ Financials

Explosive Revenue Growth vs. Deepening Losses

An OE Solutions investment analysis reveals a stark contrast. The company has demonstrated impressive top-line growth, with Q1 2025 revenue soaring 92.1% year-over-year to 29.9 billion KRW. This is fueled by aggressive expansion beyond 5G into high-demand sectors like Fiber to the Home (FTTH), Cable TV (CATV/MSO), and Datacenters. However, this growth has come at a significant cost.

Despite revenue doubling, OE Solutions reported an operating loss of 9.7 billion KRW and a net loss of 10.7 billion KRW, primarily due to heavy investment in R&D, which accounts for over 24% of sales.

This dynamic—investing heavily for future dominance at the expense of current profitability—is a critical factor. Furthermore, the company’s debt-to-equity ratio of 113.53% is relatively high, signaling that its financial health requires careful monitoring by investors.

Impact of the OE Solutions Convertible Bond Event

Short-Term Pressure: Dilution and Profit-Taking

The most immediate consequence of the convertible bond exercise is shareholder dilution. With more shares in circulation, each existing share represents a smaller piece of the company. Given that the current stock price (13,540 KRW) is significantly higher than the conversion price (10,172 KRW), there is a strong incentive for converting bondholders to sell their new shares for a quick profit. This potential wave of selling can create downward pressure on the OE Solutions stock price in the short term.

Long-Term Signal: A Bet on Future Growth

Conversely, the capital raised is a strategic asset. These funds can be used to strengthen the balance sheet and, more importantly, fuel further development of next-generation technologies like Co-Packaged Optics (CPO) and coherent optical transceivers. Success in these areas could secure OE Solutions’ long-term competitive advantage. This move can be interpreted as a signal of management’s confidence in their growth pipeline. For more on market trends, investors often consult sources like Bloomberg’s technology sector reports.

Investment Thesis & Strategic Outlook

The OE Solutions convertible bond exercise is a pivotal event, not a simple positive or negative signal. Investors must weigh the immediate risks against the long-term strategic vision.

- •Short-Term Cautious Approach: Expect potential volatility and downward price adjustments due to increased share supply.

- •Long-Term Focus: The key is whether the company can translate its R&D spending into improved profitability. Monitor upcoming earnings reports for a clear path to positive cash flow.

A successful investment hinges on the company’s ability to execute its growth strategy effectively. Investors should supplement this analysis by understanding broader principles of long-term tech investing. The ultimate test will be if the new capital can generate returns that far outweigh the initial shareholder dilution.

Frequently Asked Questions (FAQ)

What is the main takeaway from the OE Solutions convertible bond exercise?

The company is raising capital to fund future growth, which it believes will create long-term value. However, this action creates short-term risk for the stock price due to dilution and potential selling pressure from new shareholders.

Is OE Solutions a good investment right now?

It depends on your risk tolerance and investment horizon. OE Solutions is a high-growth, high-risk company. If you believe in its technology and market expansion strategy, the current volatility could be an opportunity. If you are risk-averse, the ongoing losses and high debt are significant concerns.

What key metrics should I watch for in OE Solutions’ next earnings report?

Look beyond revenue growth. Focus on improvements in operating profit margin, a reduction in the rate of cash burn, and any specific updates on the monetization of their new ventures in the Datacenter and FTTH markets. A clear strategy for achieving profitability is the most important factor to monitor.