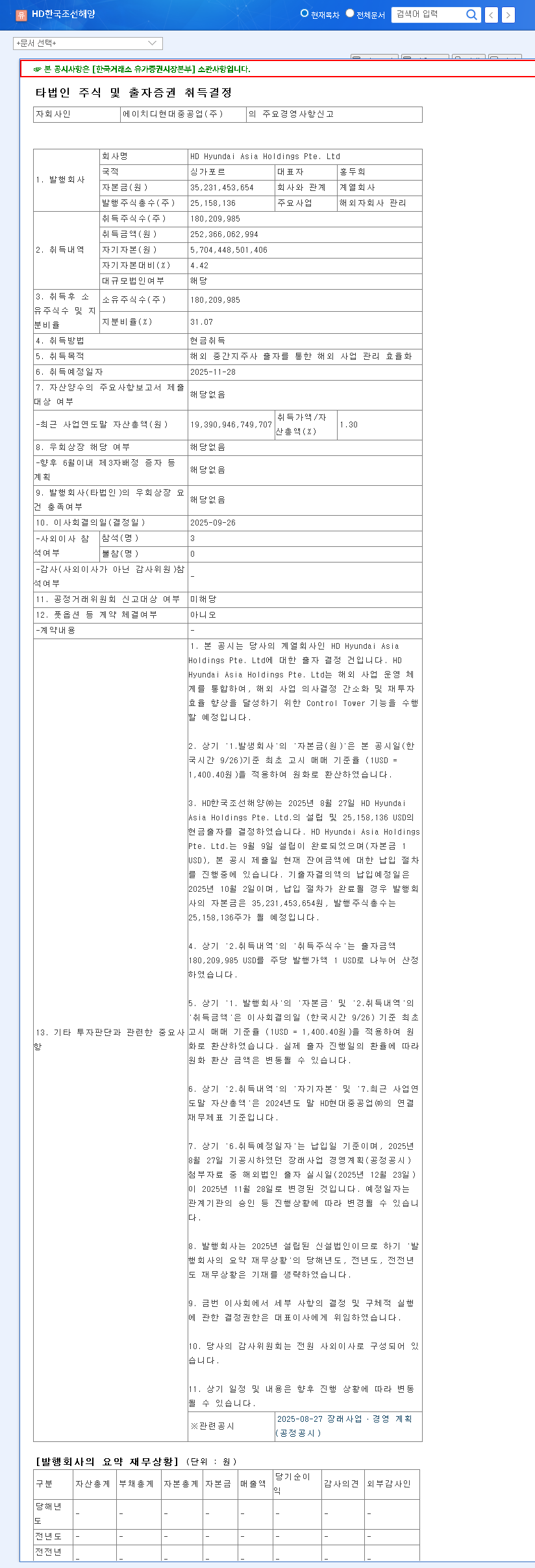

In a significant move that underscores its resilience in a fluctuating global shipping market, HD Hyundai Heavy Industries Co., Ltd. has announced a major new contract. The shipbuilding giant has secured a substantial KRW 256.2 billion agreement for two advanced crude oil tankers. This development is more than just a number on an order book; it’s a critical indicator of the company’s strategic positioning, technological prowess, and future stock performance potential. This analysis will dissect the contract’s details, evaluate the company’s standing amidst industry trends like eco-friendly vessel demand, and provide a comprehensive investment guide for stakeholders monitoring HD Hyundai Heavy Industries stock.

Contract Details: A KRW 256.2 Billion Strategic Win

On November 13, 2025, HD Hyundai Heavy Industries formalized a pivotal agreement with an Oceania-based shipping firm. The contract encompasses the construction and delivery of two 157,000 DWT (deadweight tonnage) crude oil tankers. These vessels, often classified as Suezmax tankers, are crucial assets in global energy logistics, capable of transiting the Suez Canal fully laden.

The total value of this order is KRW 256.2 billion, representing 1.77% of the company’s projected revenue for the first half of 2025. The construction and delivery period is slated to run from the contract date until October 31, 2028. The details of this agreement were confirmed in an Official Disclosure, providing transparency to the market. This order not only bolsters the company’s backlog but also reaffirms its strong relationships with key global shipping partners.

This order for two high-value crude oil tankers is a clear testament to HD Hyundai Heavy Industries’ market leadership and its ability to secure vital contracts even as the global shipbuilding landscape evolves.

Market Position and Future Growth Drivers

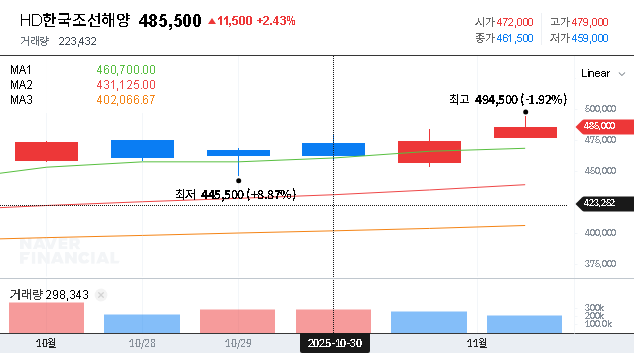

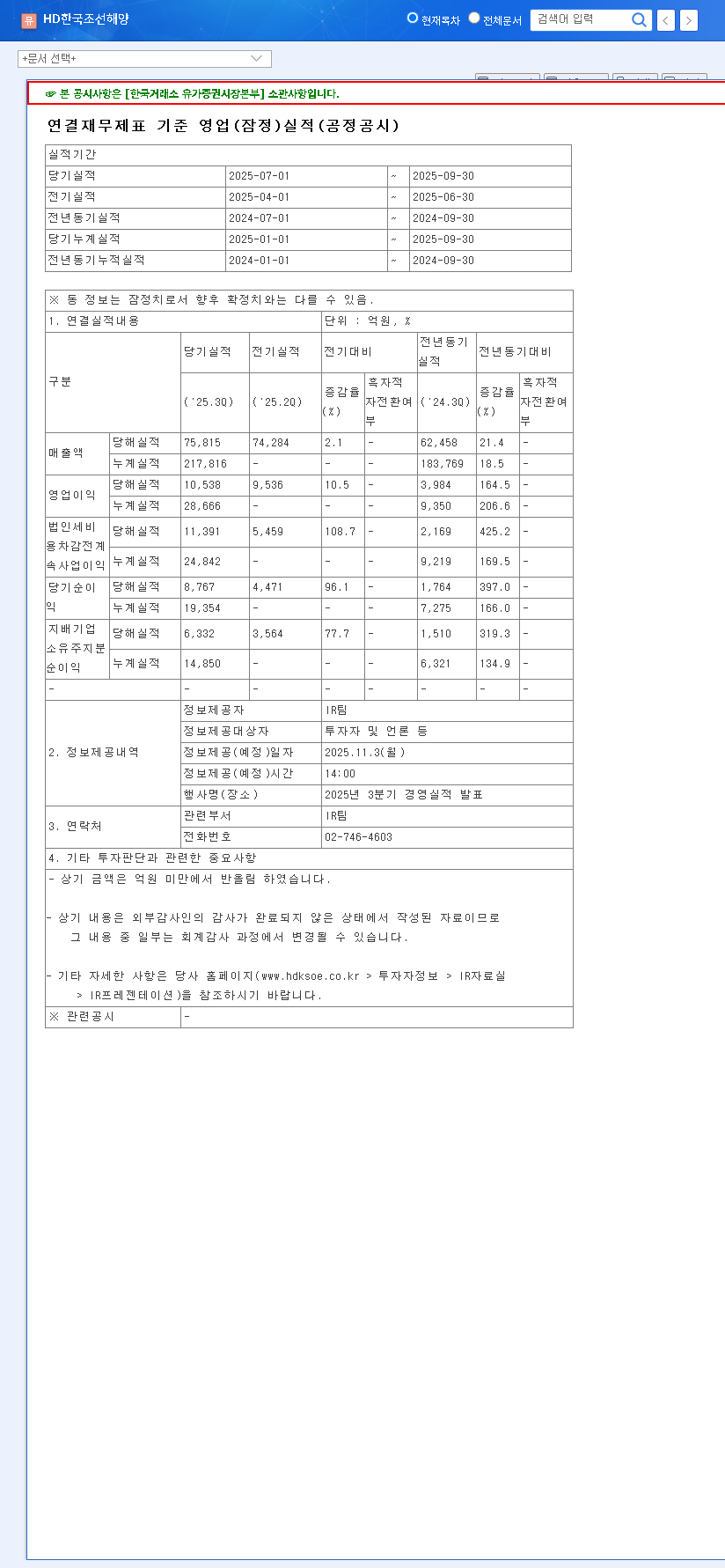

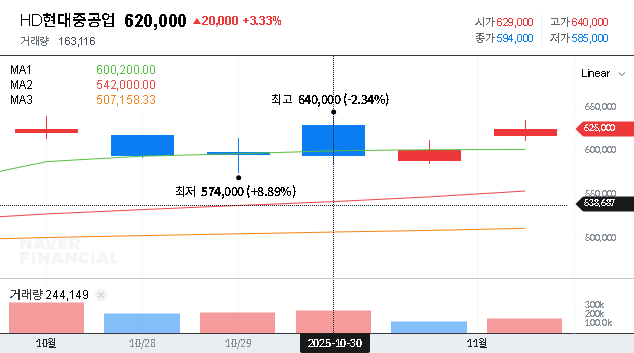

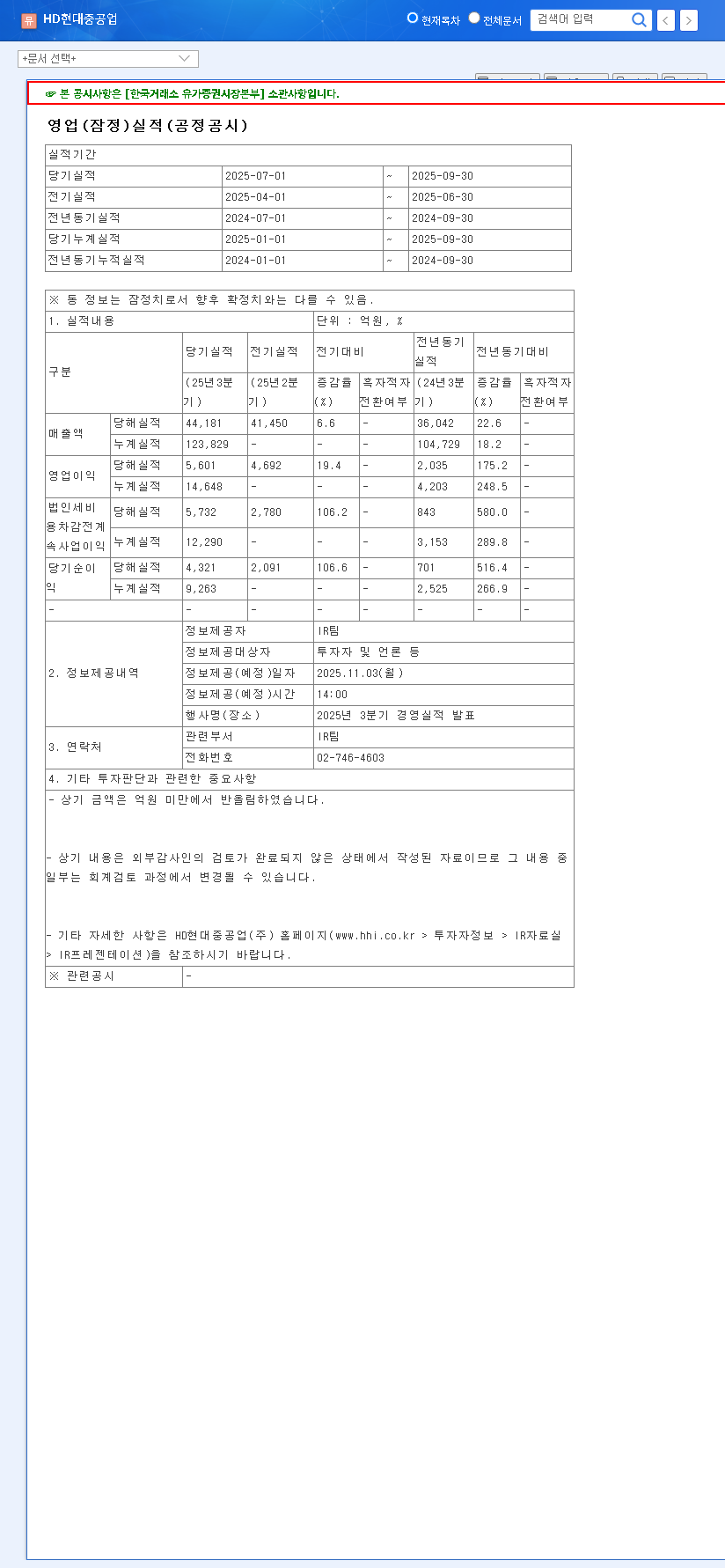

While the first half of 2025 saw a performance dip with revenue at KRW 7.97 trillion (down 9.6% YoY) and operating profit at KRW 905.2 billion (down 25.1% YoY) due to a global slowdown in new orders, the company’s strategic initiatives paint a more optimistic future. A deeper look into its core segments reveals a multi-faceted approach to growth.

Shipbuilding: The Green Revolution

The shipbuilding industry is at a crossroads, driven by the dual pressures of aging fleets and stringent environmental regulations. Mandates from the International Maritime Organization (IMO) and the EU are accelerating the transition to eco-friendly vessels. HD Hyundai Heavy Industries is capitalizing on this trend by focusing on high-value, technologically advanced ships powered by LNG, ammonia, and methanol. This strategic pivot is essential for maintaining market leadership and securing premium contracts.

Offshore Plant & Renewable Energy

Stabilizing oil prices provide a floor for the traditional offshore plant segment. However, the real long-term growth story is in renewable energy. The company is actively expanding its portfolio to include offshore wind power installations and other green energy infrastructure projects. While this segment faces challenges from raw material price volatility, its strategic importance for diversification cannot be overstated. For more information, you can read our deep-dive on the global shipbuilding industry.

Engine & Machinery: Powering the Future

This segment remains a cornerstone of profitability. The push for decarbonization is fueling massive demand for eco-friendly dual-fuel engines. HD Hyundai Heavy Industries is at the forefront of developing next-generation power systems, including promising ammonia-fueled engines, which strengthens its competitive moat and ensures its technology remains critical to the future of shipping.

Financial Health and Investment Thesis

From a financial standpoint, the company shows signs of robust health. As of June 2025, the debt-to-equity ratio improved to 219.3%, and cash flow from operations surged by an impressive 61.6%. Most importantly, the order backlog stands at a massive KRW 46.34 trillion. This enormous backlog provides exceptional revenue visibility and a stable foundation for profitability over the next several years.

While the short-term impact of this KRW 256.2 billion contract is modest, its long-term implication is significant. It reinforces positive market sentiment, demonstrates continued ordering momentum, and expands the company’s global footprint. This leads to our current investment rating of ‘Neutral,’ with a positive long-term outlook contingent on continued execution.

Actionable Investment Strategy

- •For Short-Term Investors: A cautious approach is warranted. Key metrics to monitor include new order flow, steel and other raw material price trends, and currency exchange rate fluctuations. The performance of the eco-friendly vessel market is a primary catalyst.

- •For Mid-to-Long-Term Investors: Focus on the bigger picture. Analyze the company’s progress in new business segments like offshore wind, its ESG initiatives, and its R&D pipeline for future-fuel technologies. A long-term perspective aligned with the recovery cycle of the global shipbuilding market is recommended.

Frequently Asked Questions

What is the latest major order for HD Hyundai Heavy Industries?

The company recently secured a KRW 256.2 billion contract for two 157,000 DWT crude oil tankers from an Oceania-based shipping company.

How does this contract affect the company’s revenue?

The contract value is 1.77% of the first-half 2025 revenue. While the immediate financial impact is limited, it strengthens the substantial order backlog and supports long-term revenue and profit stability.

What is the current financial health of HD Hyundai Heavy Industries?

As of mid-2025, the company’s financial health is considered sound, marked by an improved debt-to-equity ratio, a significant increase in operating cash flow, and a robust order backlog of over KRW 46 trillion.

Disclaimer: This content is for informational purposes only and is based on publicly available information and general market analysis. It should not be construed as investment advice or a recommendation to buy or sell any security. Investors should conduct their own research and make decisions based on their own judgment and risk tolerance.