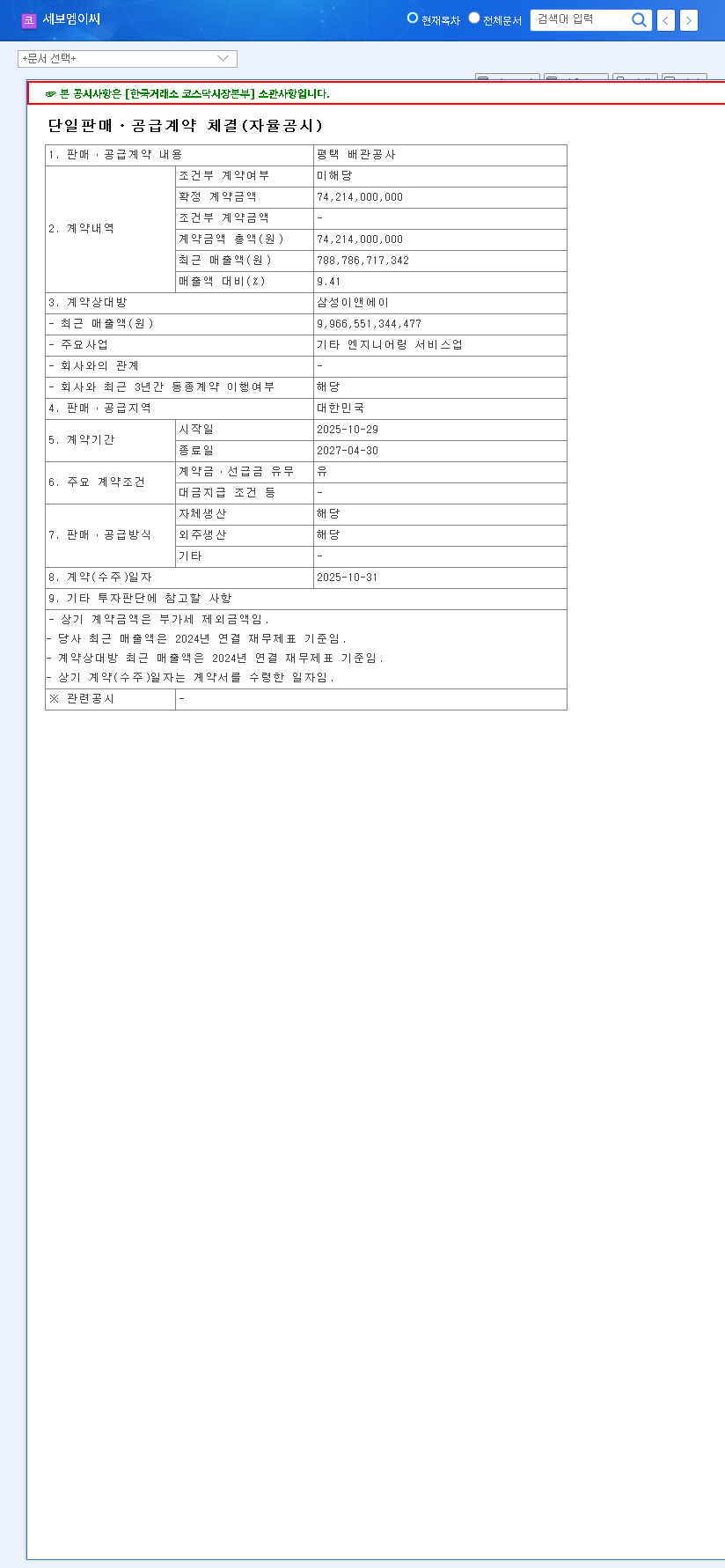

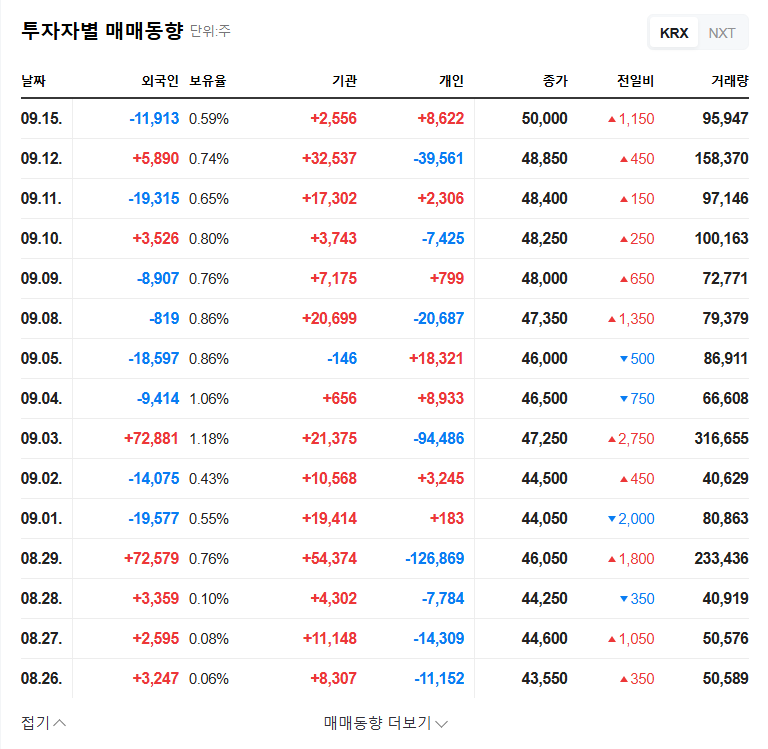

In a significant development for the industrial construction sector, SEBO MANUFACTURING ENGINEERING CORPORATION (SEBO MEC) has officially secured a major deal with Samsung E&A. This newly announced SEBO MEC contract, valued at an impressive ₩74.2 billion, provides a much-needed boost and a clear strategic direction amidst a challenging domestic construction market. The project focuses on critical piping construction and represents a substantial portion of SEBO MEC’s annual revenue, signaling both a vote of confidence from an industry leader and a potential catalyst for future growth.

This analysis will delve into the specifics of the SEBO MEC contract, examine the company’s underlying financial health, and weigh the opportunities against the persistent macroeconomic headwinds. For investors and industry observers, understanding the nuances of this agreement is key to evaluating SEBO MEC’s trajectory over the next few years.

Breaking Down the Landmark Samsung E&A Contract

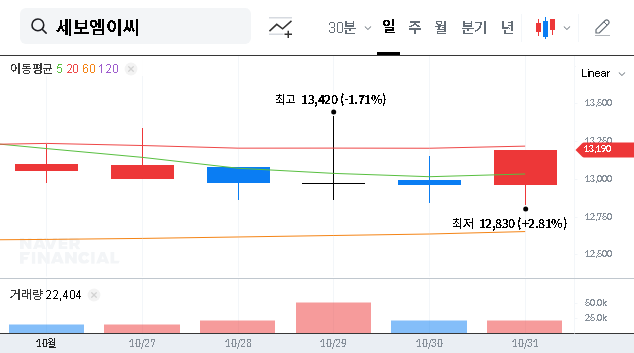

The core of this announcement is a single sales and supply agreement for Pyeongtaek piping construction with Samsung E&A. Valued at approximately ₩74.2 billion (around $54 million USD), this deal constitutes a remarkable 9.41% of SEBO MEC’s recent total revenue. The contract’s timeline is set from October 29, 2025, to April 30, 2027, ensuring a stable revenue stream for the company for an 18-month period. The full details of this significant agreement have been made public. (Source: Official DART Disclosure). This partnership not only strengthens SEBO MEC’s core business but also enhances its market position as a trusted contractor for large-scale industrial projects.

SEBO MEC’s Financial Health: A Foundation of Stability

Despite a year-over-year revenue decrease in the first half of 2025 due to the broader market slowdown, SEBO MANUFACTURING ENGINEERING CORPORATION has maintained solid fundamentals. The company’s core facility business continues to be a reliable pillar, accounting for over 92% of total revenue. While profitability saw a slight dip, proactive cost-efficiency measures have helped mitigate the impact.

Key Financial Strengths

- •Improved Financial Soundness: The company’s debt-to-equity ratio improved to a healthy 55%, indicating low leverage and a reduced financial risk profile.

- •Strategic Diversification: SEBO MEC is not standing still. By acquiring an environmental specialty construction license, it is actively diversifying its operations to tap into new growth markets.

- •Shareholder Value: Consistent share buyback programs signal management’s confidence in the company’s long-term value and commitment to shareholder returns.

“Securing a high-value contract with a blue-chip partner like Samsung E&A in this climate is a testament to SEBO MEC’s technical expertise and market reputation. It provides a critical buffer against industry-wide volatility.”

Navigating the Headwinds: Market Risks and Challenges

While the SEBO MEC contract is a major victory, the company still operates in a challenging environment. The South Korean construction market is projected to see a further decline in investment through 2026, which could suppress new order opportunities. Furthermore, global economic uncertainties, as highlighted in forecasts from institutions like the International Monetary Fund (IMF), add another layer of risk. Potential trade conflicts, resurgent inflation, and interest rate volatility can negatively impact corporate investment sentiment and project financing.

Profitability could also face pressure from fluctuating prices of key raw materials like steel coils. Although prices have recently trended downwards, their inherent volatility requires careful and strategic management throughout the duration of the Pyeongtaek piping construction project.

Investor Outlook and Strategic Path Forward

For investors, the key takeaway is one of cautious optimism. This contract significantly de-risks SEBO MEC’s short-to-medium-term revenue outlook and solidifies its core business. The immediate positive impact on investor sentiment could provide momentum for its stock price. However, long-term success will hinge on the company’s ability to execute this project flawlessly while navigating the broader economic landscape.

Recommendations for Sustained Growth:

- •Flawless Execution: Delivering the Samsung E&A project on time and on budget is paramount to building a foundation for future collaborations and securing a reputation for excellence.

- •Aggressive Diversification: Continue to pursue new clients and translate new ventures, like environmental construction, into tangible revenue streams to offset cyclical downturns in the industrial construction sector.

- •Proactive Financial Management: Enhance financial stability by hedging against currency and interest rate volatility. Investors can learn more by reading our complete guide to industrial sector investing.

In conclusion, the ₩74.2 billion SEBO MEC contract is a powerful strategic win. It provides a stable anchor in a turbulent market, but the company’s long-term prosperity will depend on its agility and continued strategic discipline.