ST PHARM Co., Ltd. (KRX: 237690) has captured the market’s attention with its preliminary Q3 2025 earnings, revealing a performance that didn’t just meet expectations—it shattered them. This remarkable achievement signals a pivotal moment for the company, showcasing robust growth in its core businesses and a strengthening financial foundation. For investors, this raises a critical question: Is this the start of a sustained growth trajectory for ST PHARM? This comprehensive analysis will dissect the Q3 results, explore the key drivers behind this success, and evaluate the long-term ST PHARM investment thesis.

Decoding ST PHARM’s Blockbuster Q3 2025 Earnings

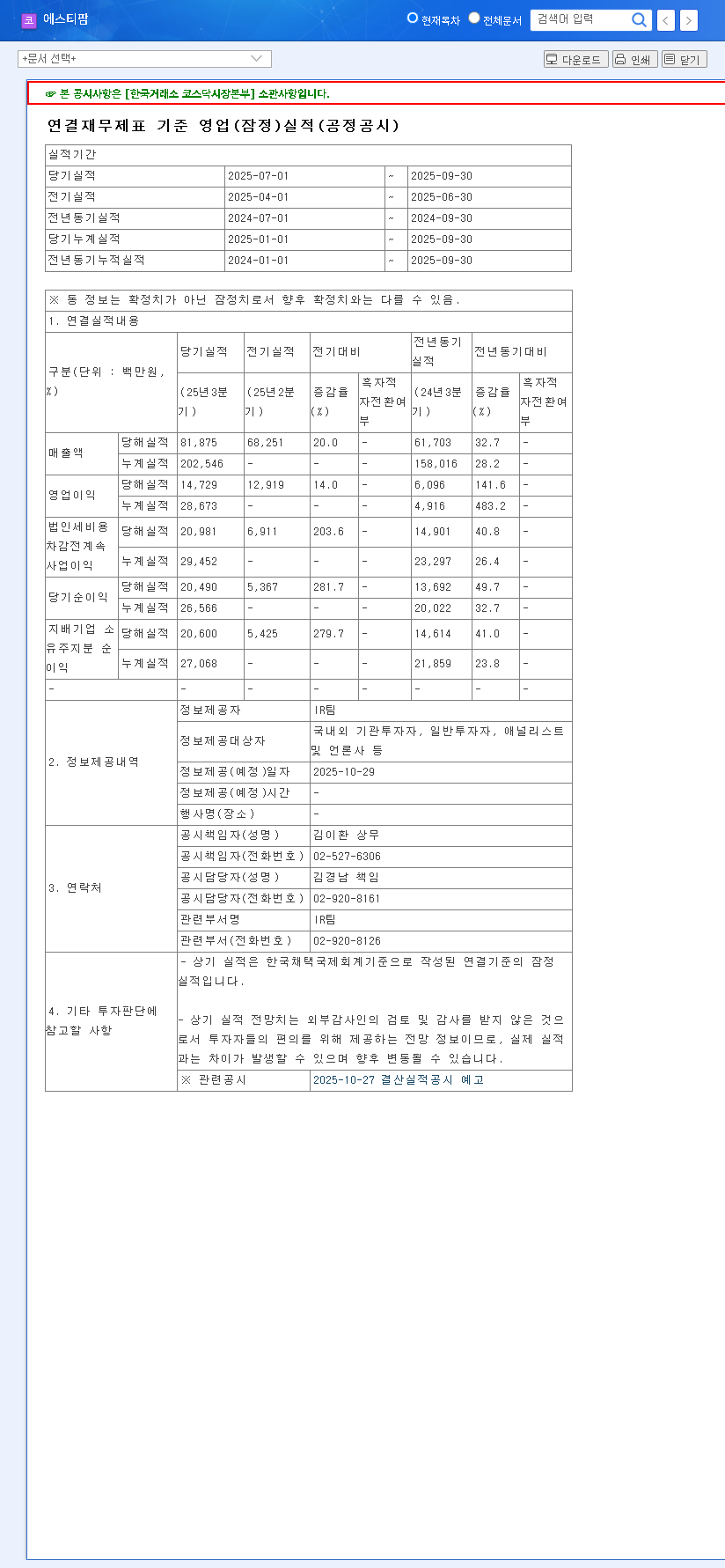

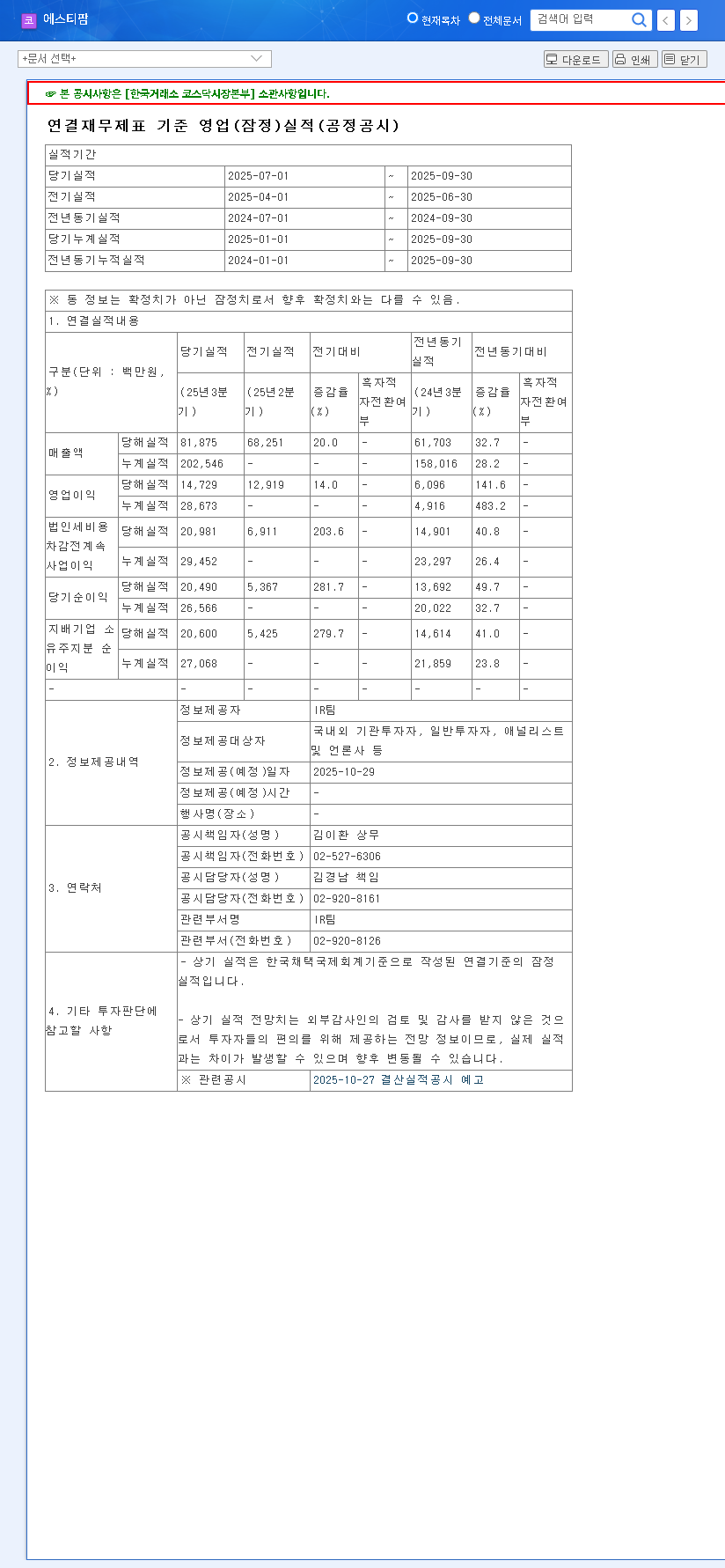

The preliminary consolidated financial results, announced on October 29, 2025, delivered an exceptionally positive surprise. The numbers speak for themselves, painting a picture of a company firing on all cylinders. According to the Official Disclosure (Source), ST PHARM’s performance far outpaced market consensus:

- •Revenue: KRW 81.9 billion, a remarkable 23% above the projected KRW 66.4 billion.

- •Operating Profit: KRW 14.7 billion, an explosive 130% surge compared to the expected KRW 6.4 billion.

- •Net Profit: KRW 20.6 billion, a staggering 390% above the forecast of KRW 4.2 billion.

This explosive growth, particularly in operating and net profit, underscores a significant improvement in profitability and highly efficient cost management. The cumulative performance for the first three quarters of 2025 further solidifies this trend, setting a strong precedent for the year-end results.

The Dual Engines Driving ST PHARM’s Growth

This outperformance isn’t accidental. It’s the direct result of strategic focus and excellence in high-growth sectors. Two areas, in particular, are responsible for propelling ST PHARM’s financial success.

Mastery in Oligonucleotide & mRNA CDMO

The core of ST PHARM’s success lies in its Contract Development and Manufacturing Organization (CDMO) services, specifically for oligonucleotides and mRNA. Oligonucleotides are short DNA or RNA molecules used in precision therapies, while mRNA technology, famously used in COVID-19 vaccines, holds immense promise for treating a wide range of diseases. As the global demand for these advanced therapeutics grows, specialized manufacturing partners like ST PHARM become indispensable. The company has expertly capitalized on this trend, leveraging its advanced technology and production capabilities. To learn more about this revolutionary field, you can explore resources from authoritative bodies like the National Institutes of Health. For a closer look at market dynamics, you can read our guide on navigating the global CDMO market.

Strategic Expansion: 2nd Oligo Facility & sgRNA Ventures

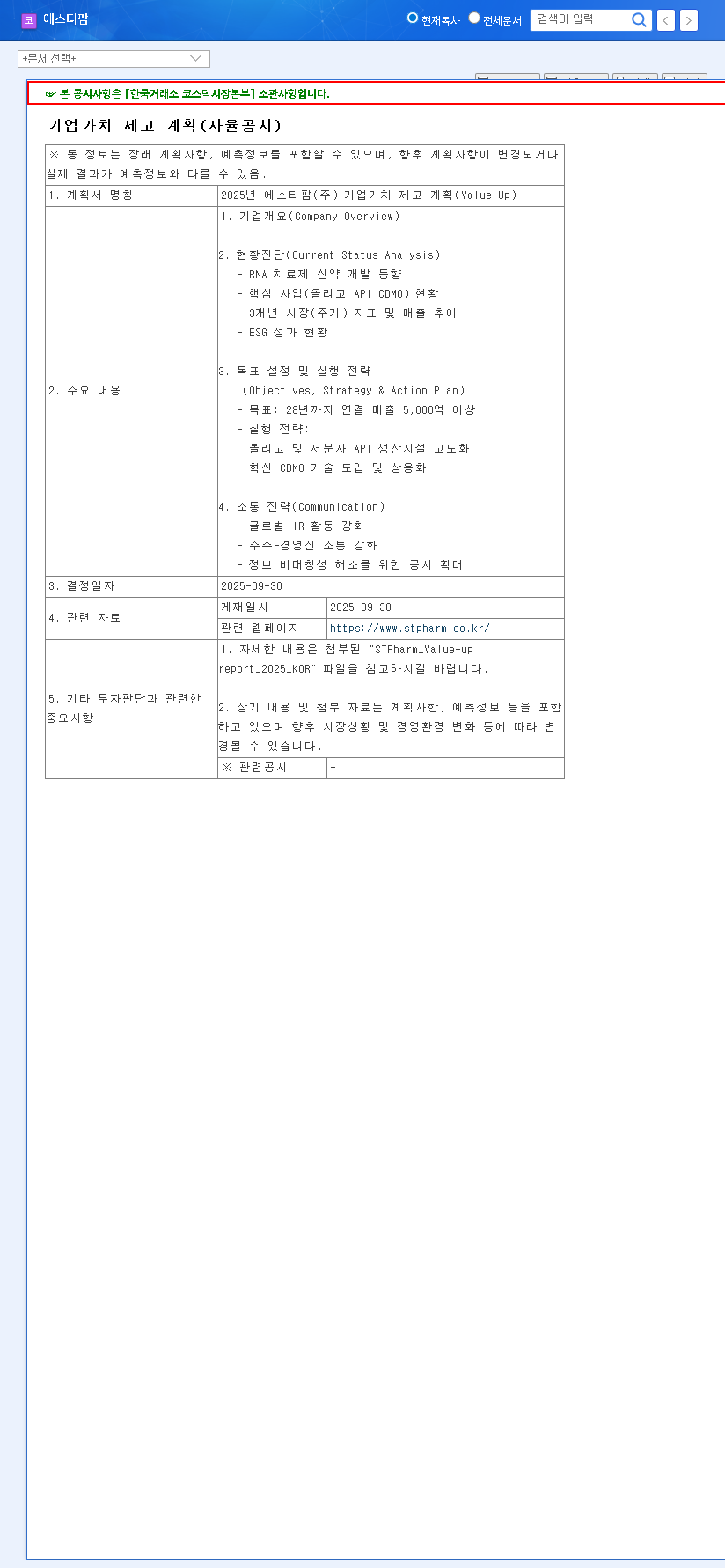

ST PHARM is not resting on its laurels. The company is actively investing in future growth. The impending operation of its second oligonucleotide facility is set to significantly boost production capacity, allowing it to take on more and larger contracts. Furthermore, its strategic entry into the sgRNA (small guide RNA) business is a forward-thinking move. sgRNA is a critical component of CRISPR gene-editing technology, positioning ST PHARM at the forefront of the next wave of genetic medicine innovation.

ST PHARM’s strategy is clear: dominate the current oligonucleotide and mRNA CDMO market while simultaneously building the infrastructure to lead the next generation of gene-editing therapeutics.

A Comprehensive ST PHARM Investment Analysis

Strengthening Financials and Profitability

Beyond the headline numbers, ST PHARM’s financial health is showing marked improvement. The company is transitioning from a period of investment and losses into a phase of sustainable profitability. The impressive operating profit margin of nearly 18% and net profit margin of over 25% in Q3 are not just one-offs but indicators of a structurally sound business model. A steadily decreasing debt-to-equity ratio and rising current ratio also point to excellent liquidity and a stable foundation for future investments.

Risks and Considerations for Investors

No investment is without risk. For ST PHARM, a key factor to monitor is exchange rate volatility. With a significant portion of its business conducted in foreign currencies, fluctuations in the KRW/USD and KRW/EUR rates can impact reported profits. Additionally, the CDMO space is becoming increasingly competitive, and investors should watch for how ST PHARM maintains its technological edge and market share against global rivals. It’s also worth noting that past restatement disclosures were procedural corrections and did not affect the company’s intrinsic value, but rather enhanced its transparency.

Final Verdict: Is ST PHARM a Strong Investment Opportunity?

The ST PHARM Q3 2025 earnings report is a powerful testament to the company’s robust fundamentals and rapid growth in the high-demand oligonucleotide CDMO and mRNA sectors. With clear growth drivers, expanding capacity, and a strengthening financial position, ST PHARM presents a compelling case as an attractive investment target with significant, sustained growth potential.

Disclaimer: This analysis is based on publicly available information and is for informational purposes only. It does not constitute financial advice or an investment recommendation. All investment decisions should be made based on your own research and consultation with a qualified financial advisor.