The latest SEOUL VIOSYS 2025 Q4 Outlook has sent ripples through the investment community, painting a challenging picture for the opto-semiconductor specialist (KRX: 092190). With a projected revenue of just KRW 185 billion, investors are left questioning the company’s trajectory. Is this a temporary downturn for a tech leader poised for a rebound, or a sign of deeper structural issues? This comprehensive analysis will break down the official disclosure, evaluate the company’s fundamentals, and provide a clear investment strategy for navigating the uncertainty surrounding SEOUL VIOSYS stock.

The core issue is whether Seoul Viosys’s long-term investments in next-generation technologies like Micro LED can offset the severe short-term revenue decline and restore investor confidence.

A Deep Dive into the SEOUL VIOSYS 2025 Q4 Outlook

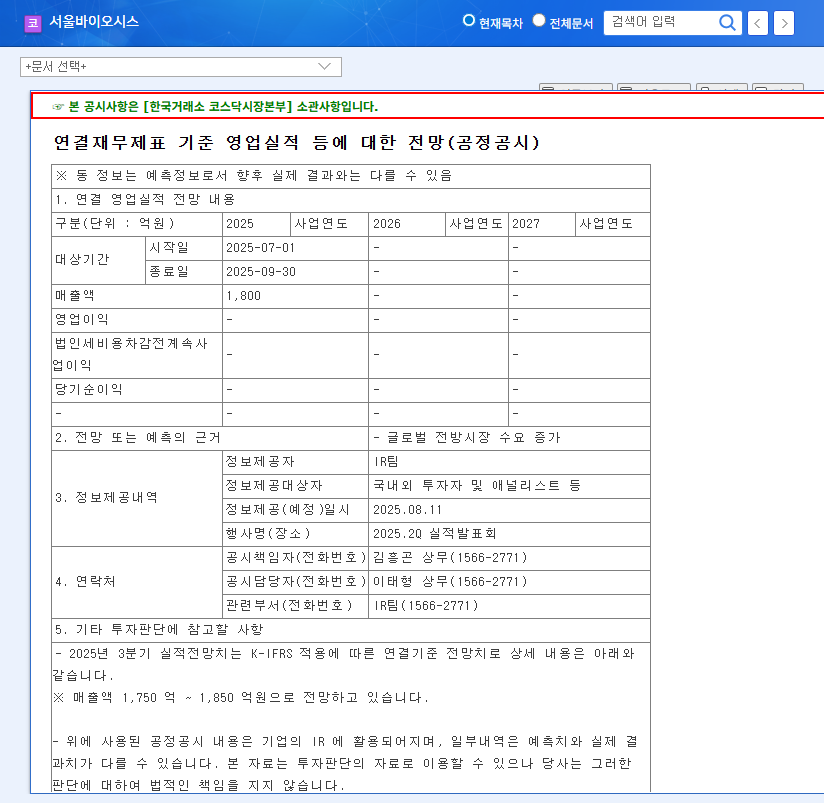

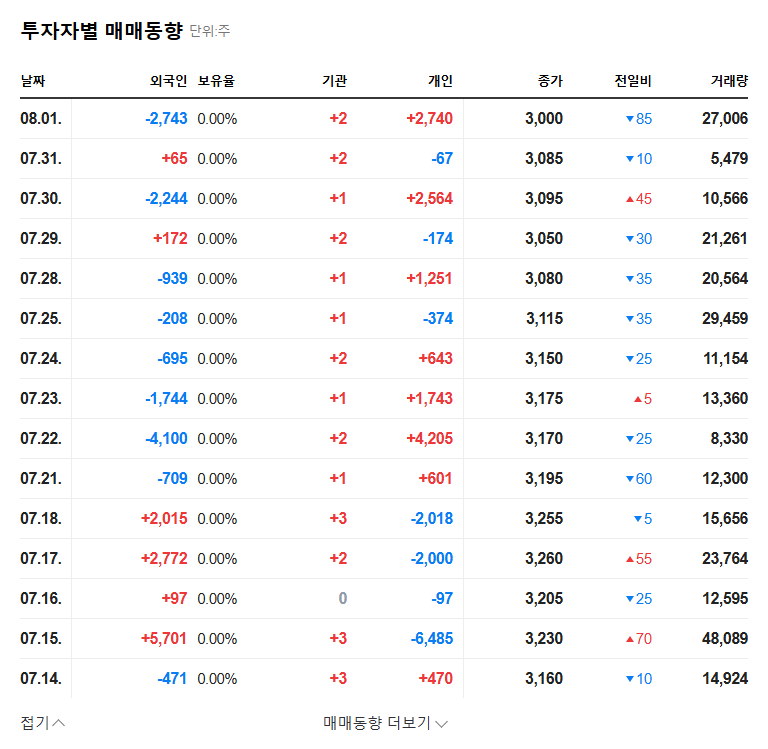

On November 14, 2025, SEOUL VIOSYS released its consolidated financial performance forecast for the fourth quarter. The headline figure—a revenue of KRW 185 billion—is starkly lower than previous periods. This projection, detailed in the company’s Official Disclosure (DART Report), serves as the primary benchmark for the market in the absence of broad analyst consensus. This figure represents a significant contraction not only year-over-year but also sequentially, amplifying concerns about a deepening business slump and casting doubt on the company’s ability to achieve profitability in the near term.

Fundamental Weaknesses: Analyzing the Performance Slump

Persistent Revenue Decline and Profitability Woes

The Q4 forecast is not an isolated event. It is the culmination of a worrying trend. The company’s cumulative revenue for the third quarter of 2025 had already fallen by 22.3% year-on-year, accompanied by a substantial operating loss of KRW 14.844 billion. While SEOUL VIOSYS holds a commanding market share in niche segments like UV LED, it has not been enough to insulate it from a broader downturn in the global LED manufacturing industry. The projected Q4 revenue pales in comparison to historical figures, suggesting that the probability of continued operating losses is extremely high and that a turnaround is not imminent.

Concerning Financial Health Indicators

A closer look at the balance sheet reveals further reasons for caution. While the debt-to-equity ratio has improved, other key metrics signal instability. The company’s financial health can be summarized by these key points:

- •Low Liquidity: A current ratio of just 49.35% indicates potential challenges in meeting short-term obligations, a significant red flag for investors.

- •Negative Cash Flow: The company is experiencing cash outflows from operating activities due to persistent losses. This strains its ability to fund operations and investments without relying on external financing.

- •Declining Projections: Key indicators such as net profit and Return on Equity (ROE) are all projected to decline, offering little solace for those looking for positive signals.

Stock Impact and Future Growth Potential

Short-Term Pain for SEOUL VIOSYS Stock

The disappointing SEOUL VIOSYS 2025 Q4 Outlook is almost certain to trigger a negative reaction in the market. This forecast is likely to fuel bearish sentiment, leading to significant short-term downward pressure on the stock price. The vast gap between this projection and previous performance metrics will likely cause a re-evaluation of the company’s worth by analysts and institutional investors, potentially leading to sell-offs.

Can Future Tech Investments Save the Day?

The bull case for SEOUL VIOSYS rests on its investment in high-growth future technologies. The company is a key player in developing Micro LEDs (the next-generation display technology), UV LEDs (for sterilization and industrial curing), and VCSELs (used in 3D sensing and LiDAR). For more information on this market, you can review our comprehensive analysis of the Micro LED market. However, the pressing question is whether these long-term bets can generate revenue quickly enough to offset the current decline. If the performance slump continues, the company’s ability to fund this crucial R&D will be questioned, eroding confidence in its long-term growth story. For a broader understanding of semiconductor trends, resources like Semiconductor Industry Association (SIA) provide valuable data.

Investment Thesis & Recommendations

Given the deeply concerning revenue forecast and underlying financial weaknesses, a highly cautious approach is warranted. The current outlook suggests that the company’s challenges are significant and not easily resolved.

Investment Opinion: Sell / Cautious Hold

The rationale is clear: the sharp decline in projected revenue points to a severe weakening of business competitiveness and a deteriorating market environment. Confidence that future technology investments can bridge the gap in the short-to-medium term is low. Investors should be aware of the following key risks:

- •Potential for further downward revisions to earnings forecasts.

- •Intensifying competition in the LED and semiconductor space.

- •Delays in the commercialization and profitability of new technologies.

- •Broader macroeconomic headwinds impacting global demand.

Investors considering a position in SEOUL VIOSYS must exercise extreme caution. It is critical to await the final Q4 earnings announcement and scrutinize management’s strategic plans for a tangible performance recovery before making any investment decisions.