The latest KEPCO earnings report for the first half of 2025 has captured the market’s full attention, revealing a significant turnaround for the utility giant. KOREA ELECTRIC POWER CORPORATION (KEPCO) announced impressive results that not only surpassed expectations but also suggest a potential shift in its long-term trajectory. For investors evaluating KEPCO stock (015760), this moment is critical. But beyond the headline numbers, what are the fundamental drivers behind this resurgence, and what risks remain on the horizon? This comprehensive analysis will break down the H1 2025 performance, explore KEPCO’s strategic initiatives, and provide a clear outlook for potential investors.

H1 2025 KEPCO Earnings: The Numbers at a Glance

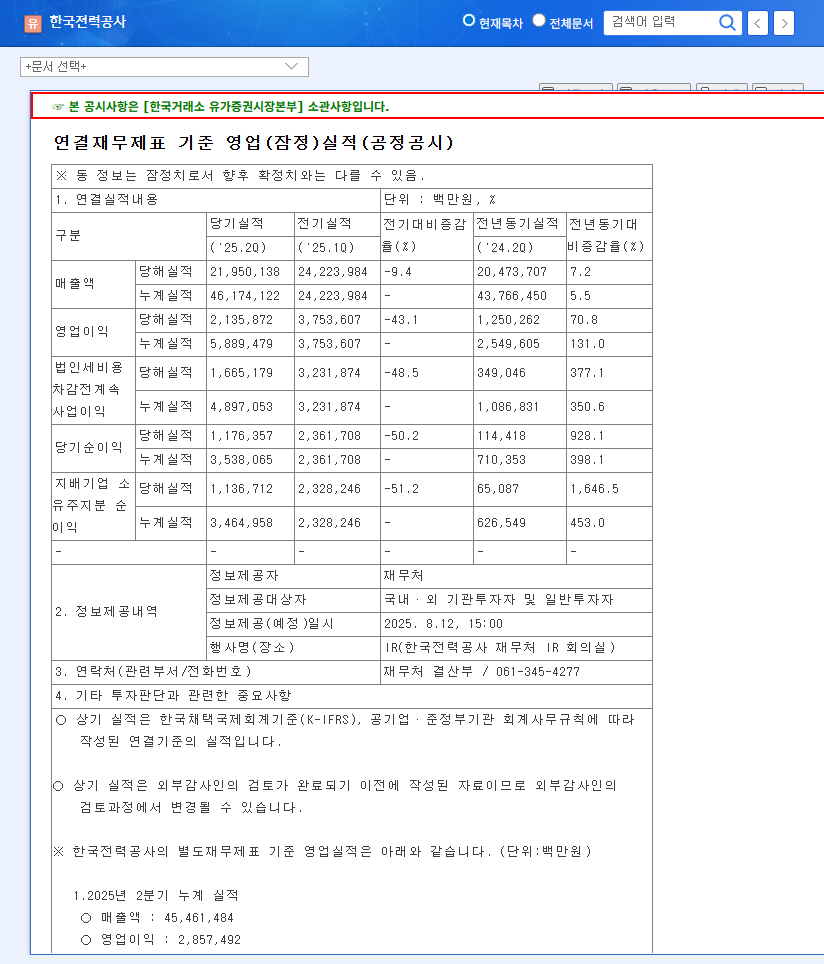

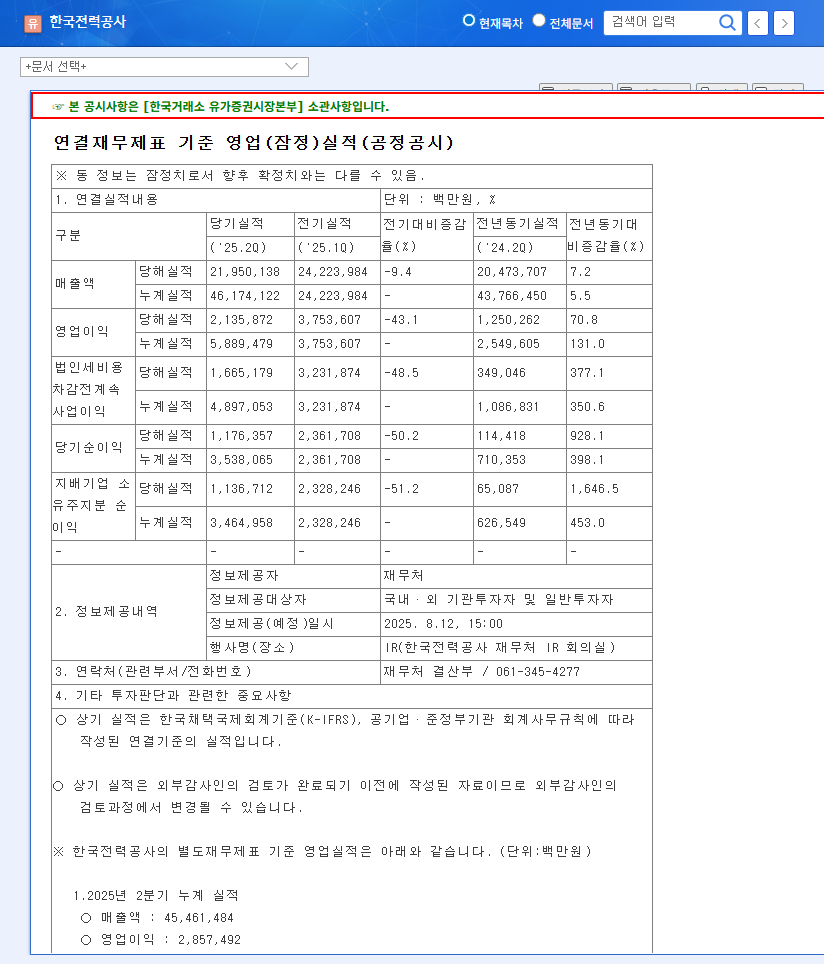

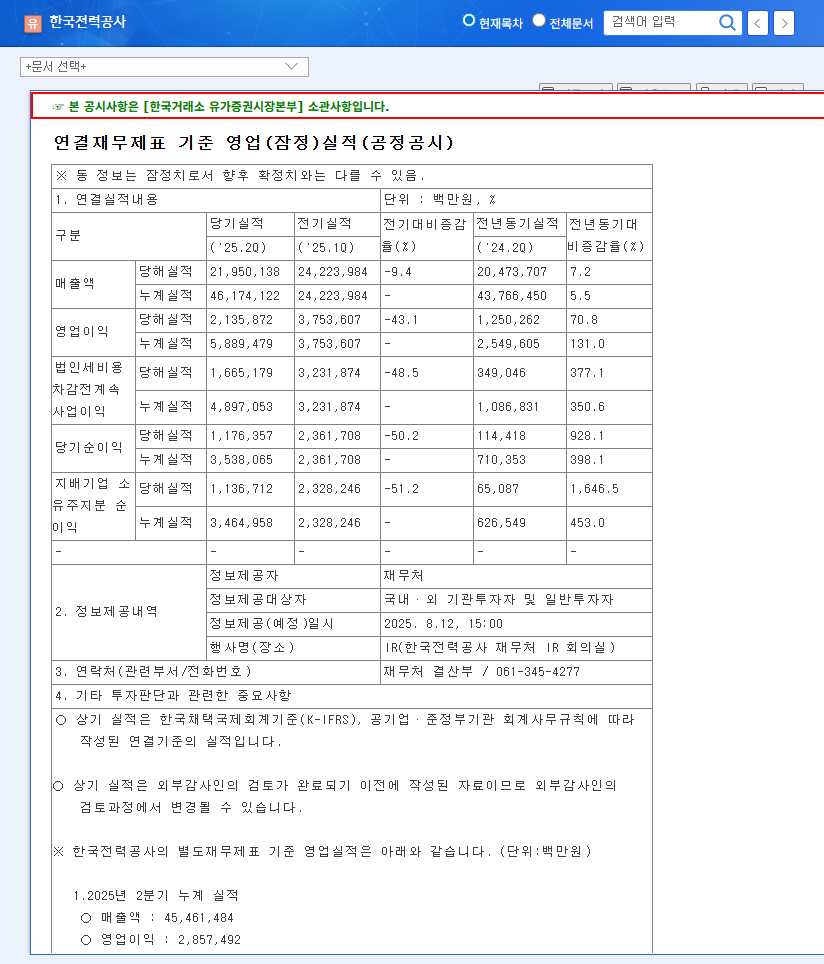

In a powerful demonstration of recovery, KOREA ELECTRIC POWER CORPORATION reported a consolidated revenue of 46.1741 trillion KRW, a year-on-year increase of 5.5%. Even more impressively, operating profit surged by 23.2% to reach 5.8895 trillion KRW. This robust performance led to a net income surplus of 3.5381 trillion KRW, a figure that decisively beat market consensus. These figures, confirmed in their official disclosure (Source: DART), signal that KEPCO’s operational and strategic adjustments are beginning to yield substantial financial fruit.

Key Drivers Fueling KEPCO’s Remarkable Growth

1. The Resurgence of Nuclear Power & Operational Excellence

A cornerstone of the improved KEPCO earnings was the exceptional performance of its nuclear power division. Achieving a high utilization rate of 92.1%, the nuclear fleet provided a stable and cost-effective source of electricity, which is crucial for profitability. This operational excellence is being exported globally, with KEPCO expanding its overseas nuclear projects in the Czech Republic and the UAE. This not only diversifies revenue but also showcases the company’s world-class technological capabilities on an international stage.

2. Strategic Tariff Adjustments and Digital Transformation

On the revenue side, an increase in electricity sales tariffs for industrial use played a significant role. This adjustment reflects both the recovery of domestic economic activity and a more favorable regulatory environment. Concurrently, KEPCO has enhanced operational efficiency and customer satisfaction through digital initiatives like the ‘KEPCO ON’ platform. This focus on technology-driven service improvement helps in retaining a loyal customer base for the long term.

3. A Decisive Pivot to Future Energy Solutions

KEPCO is proactively future-proofing its portfolio. The completion of major projects like the Jeju Hanlim Offshore Wind Power Complex and strategic acquisitions in Saudi Arabia and the U.S. highlight a serious commitment to renewable energy. This aligns with global ESG trends and diversifies the energy mix. Furthermore, investments in replacing aging coal plants with efficient LNG facilities and developing hydrogen co-firing technology show that KEPCO is adapting to tightening environmental regulations and a changing energy landscape.

KEPCO’s H1 2025 performance is more than a financial rebound; it’s a strategic pivot, balancing the stability of nuclear power with aggressive expansion into renewable and future-proof energy technologies.

Financial Health & External Risks: A Balanced View

The Lingering Challenge of Debt

Despite the positive earnings, a key concern for any KEPCO investment thesis is its financial structure. The consolidated debt ratio, while slightly improved, stood at a high 110% at the end of H1. This level of leverage poses a risk, particularly in a rising interest rate environment, as it could significantly increase interest payment burdens and pressure financial soundness. Close monitoring of KEPCO’s deleveraging efforts is essential for investors.

External Headwinds to Monitor

Several external variables could impact the KEPCO stock price and future earnings:

- •Government Policy: As a state-owned utility, KEPCO’s profitability is heavily influenced by government decisions on electricity tariffs and renewable energy mandates (RPS).

- •Macroeconomic Factors: Fluctuations in the Korean Won’s exchange rate can affect the cost of servicing foreign currency debt, while rising interest rates increase borrowing costs.

- •Global Energy Prices: The price of international commodities like oil and natural gas directly impacts fuel costs for thermal power generation, creating potential volatility in profit margins.

Action Plan for KEPCO Investors

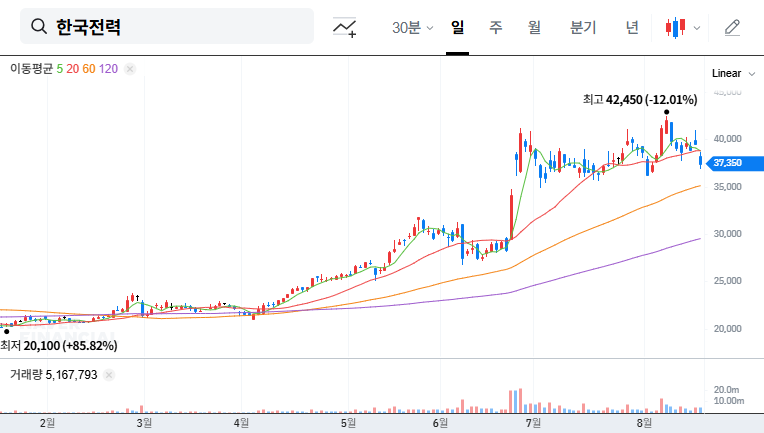

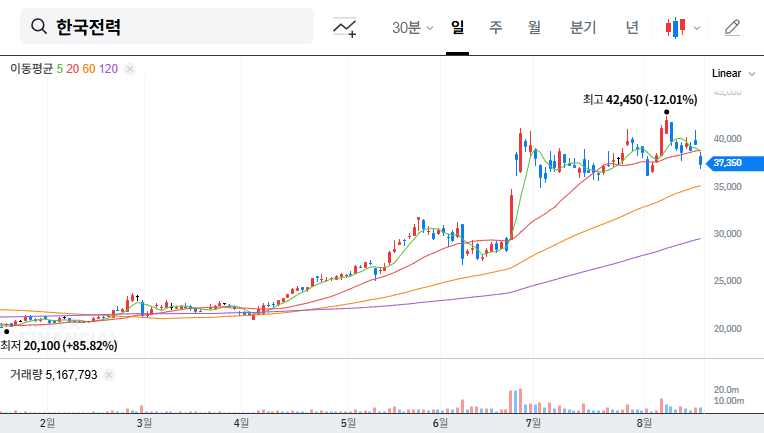

The strong KEPCO earnings and forward-looking strategy present a compelling case, but investors must weigh this against the financial and external risks. From a long-term perspective, KEPCO’s strategic positioning within the global energy transition is a significant advantage. The company’s deep expertise in nuclear power and its growing footprint in renewables could drive substantial corporate value over the next decade. The global shift towards sustainable energy is a powerful tailwind, a trend frequently highlighted by sources like the International Energy Agency.

In conclusion, KOREA ELECTRIC POWER CORPORATION is at an exciting inflection point. While the high debt ratio requires cautious monitoring, the company’s ability to generate strong profits, innovate in future technologies, and expand globally suggests a positive outlook. Investors should adopt a long-term perspective, carefully tracking KEPCO’s progress in improving its financial structure while capitalizing on its growth engines. For more analysis on this sector, you can explore our complete guide to investing in Asian utility stocks.