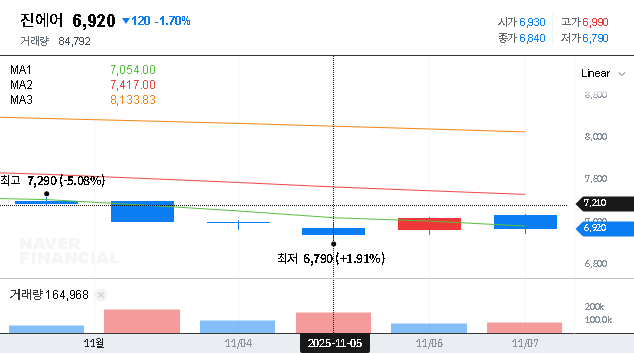

As JIN AIR CO., LTD. (272450) prepares for its crucial Q3 2025 earnings call on November 13, 2025, the aviation industry and investors are watching closely. The upcoming JIN AIR investor relations event is more than just a presentation of numbers; it’s a critical moment for the company to outline its strategy for navigating a challenging economic landscape marked by slowing profitability. After a difficult first half of 2025, this session will reveal JIN AIR’s plans to regain momentum, manage costs, and drive future growth.

This article provides a comprehensive JIN AIR financial analysis, breaking down the macroeconomic pressures, the company’s recent performance, and the key strategic questions that need answers. We will explore what investors should monitor during the IR call and outline a potential action plan for the 272450 stock analysis.

The Context: JIN AIR’s Q3 2025 Investor Briefing

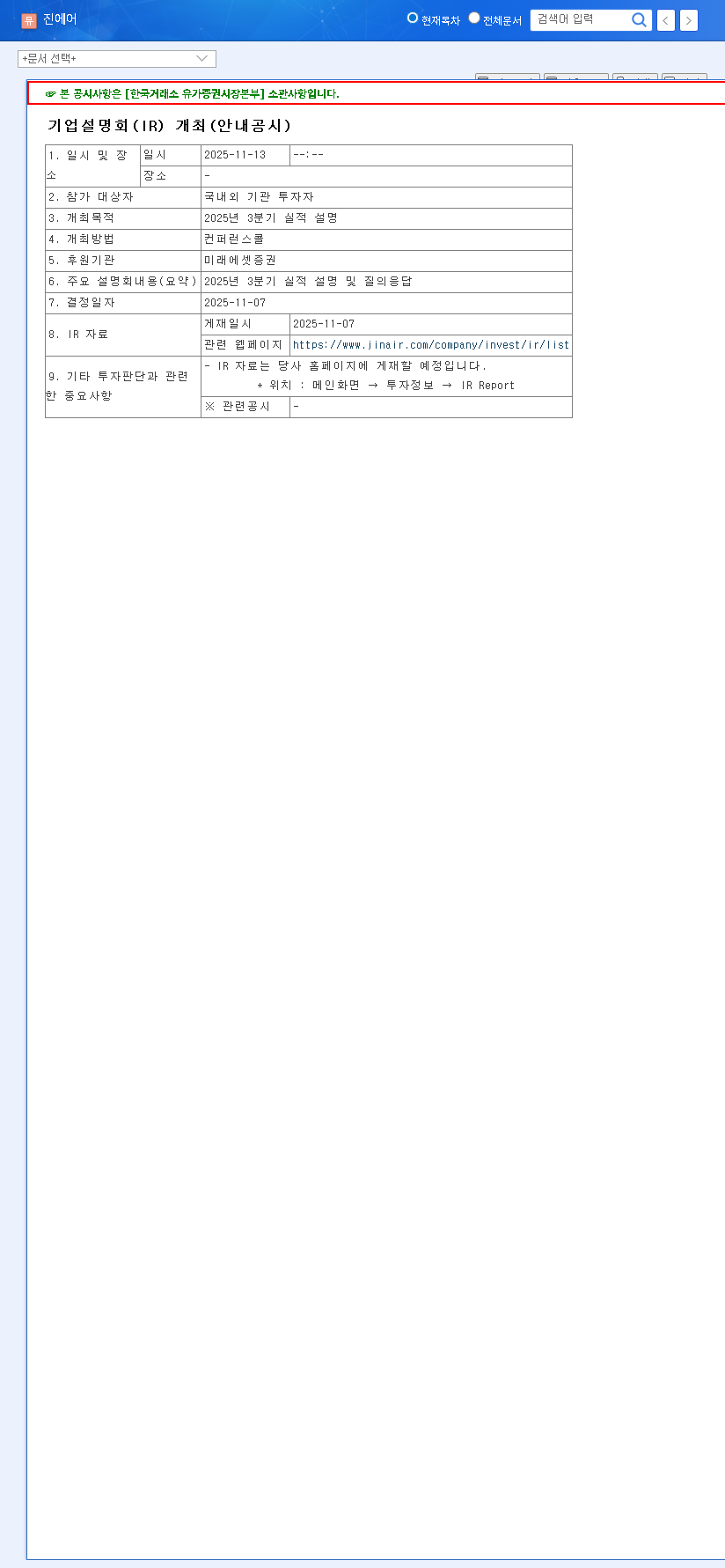

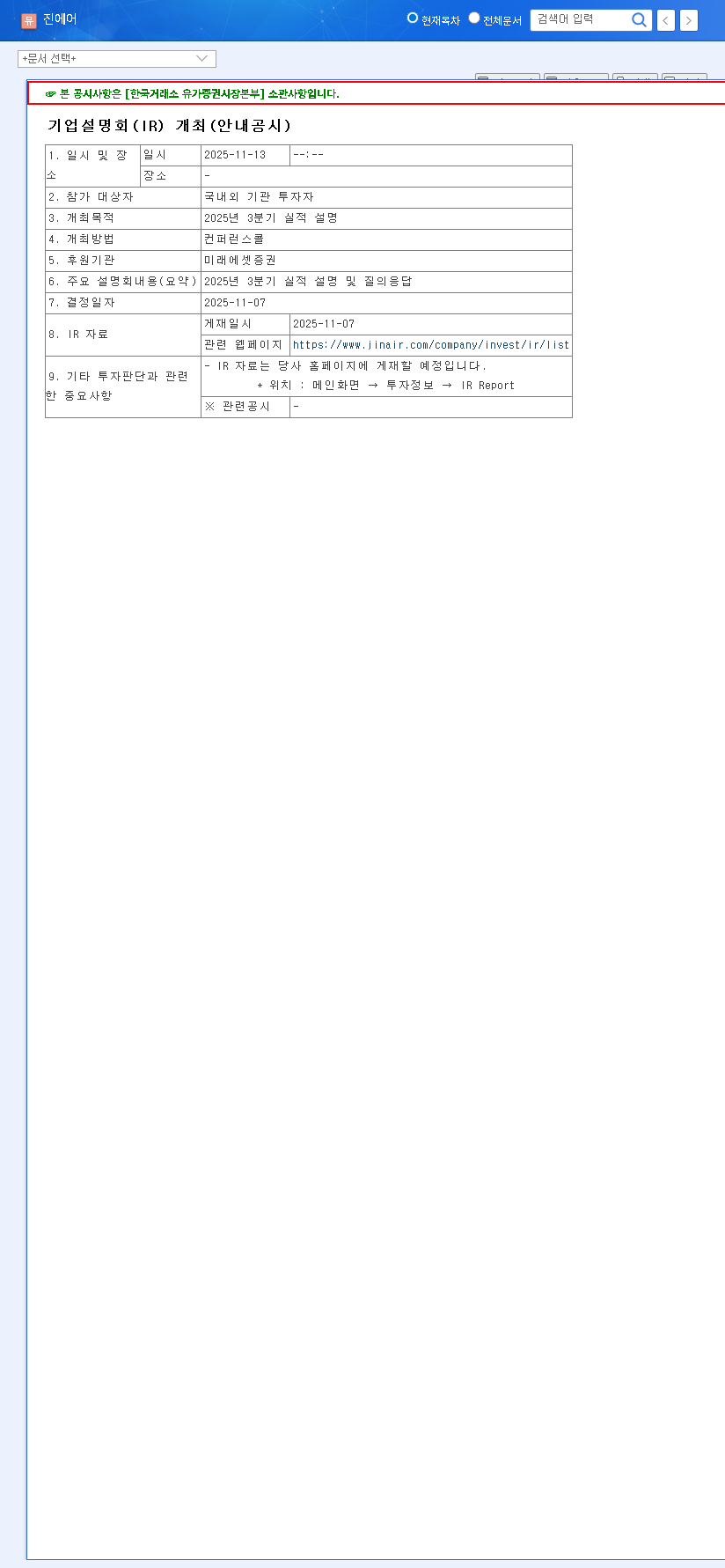

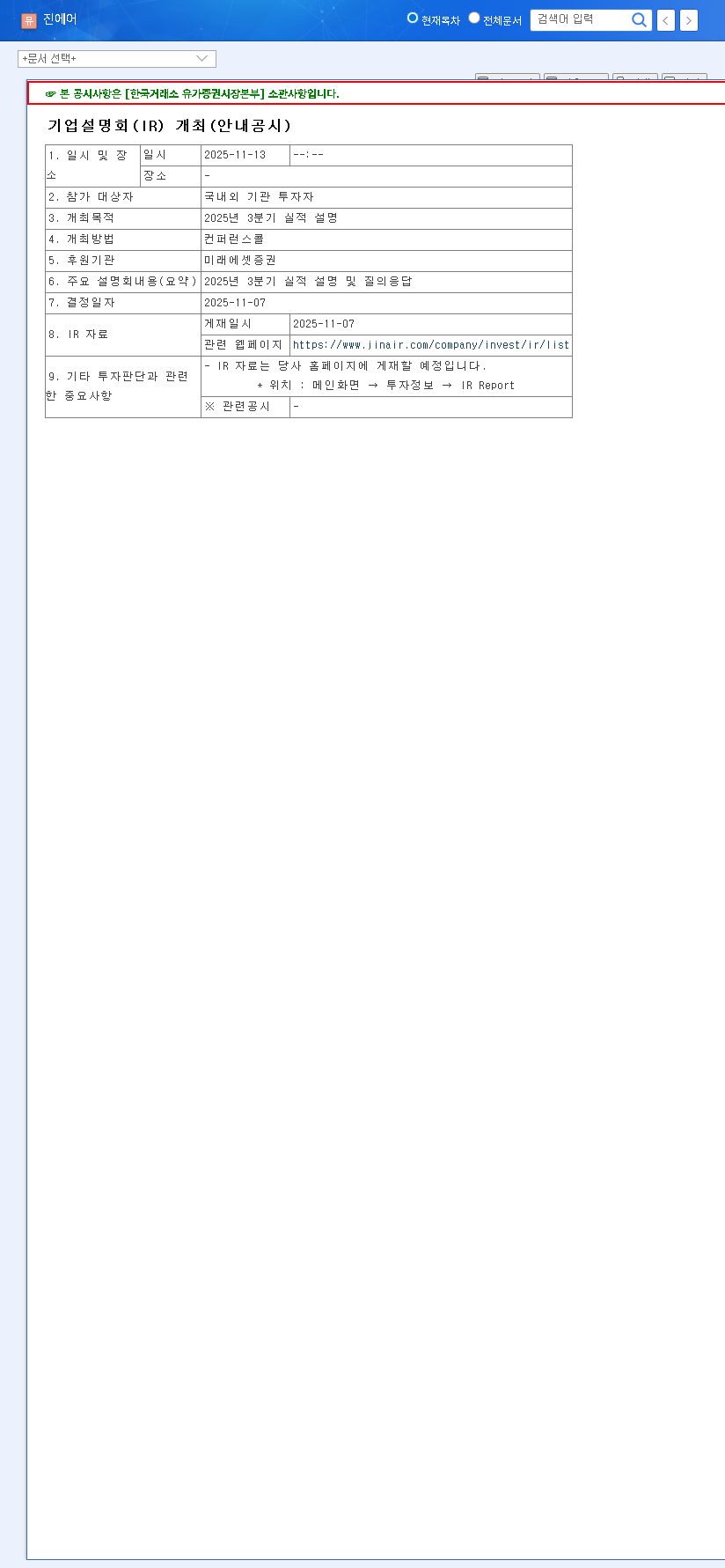

JIN AIR CO., LTD. has formally scheduled its Investor Relations (IR) briefing to announce and discuss its Q3 2025 financial results. The primary objective is to offer transparent, detailed performance data to shareholders and the broader market. More importantly, this event will serve as a platform for management to communicate its strategic direction and future outlook, aiming to rebuild market confidence. For official details regarding the announcement, stakeholders can refer to the company’s filing. (Official Disclosure)

The core challenge highlighted by H1 2025 results is a significant drop in operating profit, signaling that cost pressures and market competition are currently outpacing revenue generation. This makes the upcoming strategy reveal a pivotal moment for the company’s valuation.

Deep Dive: A Comprehensive JIN AIR Financial Analysis

The profitability slowdown observed in the first half of 2025 was not an isolated event but a result of intersecting macroeconomic headwinds and internal performance metrics. Understanding these factors is key to evaluating the JIN AIR Q3 2025 outlook.

Macroeconomic Environment (H1 2025)

- •Persistent High Oil Prices: Aviation fuel is a primary cost driver. Sustained high international oil prices directly squeezed profit margins, a trend that likely continued into Q3.

- •Exchange Rate Volatility: A strong US dollar against the Korean won increases the cost of fuel and aircraft leases, which are often priced in USD. This currency pressure is a significant variable in JIN AIR’s cost structure. For more context on global economic trends impacting airlines, you can consult authoritative sources like Reuters Market Data.

- •Intense Market Competition: The low-cost carrier (LCC) market is fiercely competitive, leading to pressure on ticket prices even as operational costs rise.

H1 2025 Performance Summary

- •Revenue vs. Profit: Revenue saw only a slight decrease to KRW 723.9 billion. However, operating profit plummeted to KRW 15.9 billion from KRW 99.3 billion year-over-year, showcasing the severe impact of rising costs on JIN AIR profitability.

- •Improving Financial Health: On a positive note, the debt-to-equity ratio improved to 3.65x, and the company returned to a retained earnings surplus, indicating better balance sheet management.

- •Strategic Bright Spots: The company is actively expanding its network with new routes (e.g., Ishigakijima, Qingdao) and leveraging data for cost optimization. Potential synergies with Korean Air remain a significant long-term positive factor.

Investor Action Plan: What to Watch in the JIN AIR Investor Relations Call

Given the mixed signals, our investment opinion remains ‘Neutral‘. The IR session is the key event that could shift this outlook. Investors should focus on the substance behind the numbers. This strategic direction is crucial, as it affects the entire LCC airline industry landscape.

Key Monitoring Points for Q3 and Beyond

- •Q3 Profit Margin Recovery: Will the announced Q3 results show an improvement in operating profit margin? This is the single most important metric to watch.

- •New Route Performance: Management should provide data on the passenger load factor (PLF) and profitability of recently launched routes.

- •Tangible Cost-Saving Measures: Look for specific details on fuel efficiency gains, operational streamlining, and the financial impact of these efforts.

- •Forward-Looking Guidance: What is the company’s outlook for Q4 2025 and early 2026? Any guidance on demand trends and cost expectations will heavily influence stock performance.

- •Korean Air Synergy Update: Investors will want concrete examples of how the collaboration with Korean Air is yielding cost savings or revenue opportunities.

Frequently Asked Questions (FAQ)

When is JIN AIR’s Q3 2025 investor relations call?

JIN AIR CO., LTD. is scheduled to host its IR session for the Q3 2025 earnings announcement on November 13, 2025.

What caused JIN AIR’s drop in profitability in H1 2025?

The primary causes were increased operational costs from high international oil prices and unfavorable exchange rates, combined with intense price competition in the LCC market which limited the ability to pass costs to consumers.

What are the main positive factors for JIN AIR’s stock?

Positive drivers include aggressive network expansion into new markets, ongoing efforts to optimize costs through data analytics, potential synergies with parent company Korean Air, and an improving balance sheet.

What is the current investment outlook for JIN AIR (272450)?

The current investment opinion is ‘Neutral’. While the company has positive long-term drivers, the short-term profitability challenges are significant. The upcoming Q3 2025 IR call is critical for assessing if a change in outlook is warranted.