The upcoming Q3 2025 Investor Relations (IR) conference for SAMSUNG SDI CO.,LTD (006400) on October 28, 2025, is poised to be a pivotal moment for investors. After a challenging first half marked by operating losses and underutilization in key segments, the market is eagerly awaiting a clear roadmap for recovery and future growth. This comprehensive Samsung SDI stock analysis will dissect the company’s current standing, evaluate the macroeconomic landscape, and outline the critical factors that will shape its trajectory, helping you make a more informed investment decision.

From its strategic investments in next-generation battery technology to the restructuring of its Electronic Materials division, Samsung SDI is making bold moves. But will these be enough to overcome the headwinds of a slowing EV market and intense competition? This IR is the company’s chance to restore confidence and prove its long-term value proposition.

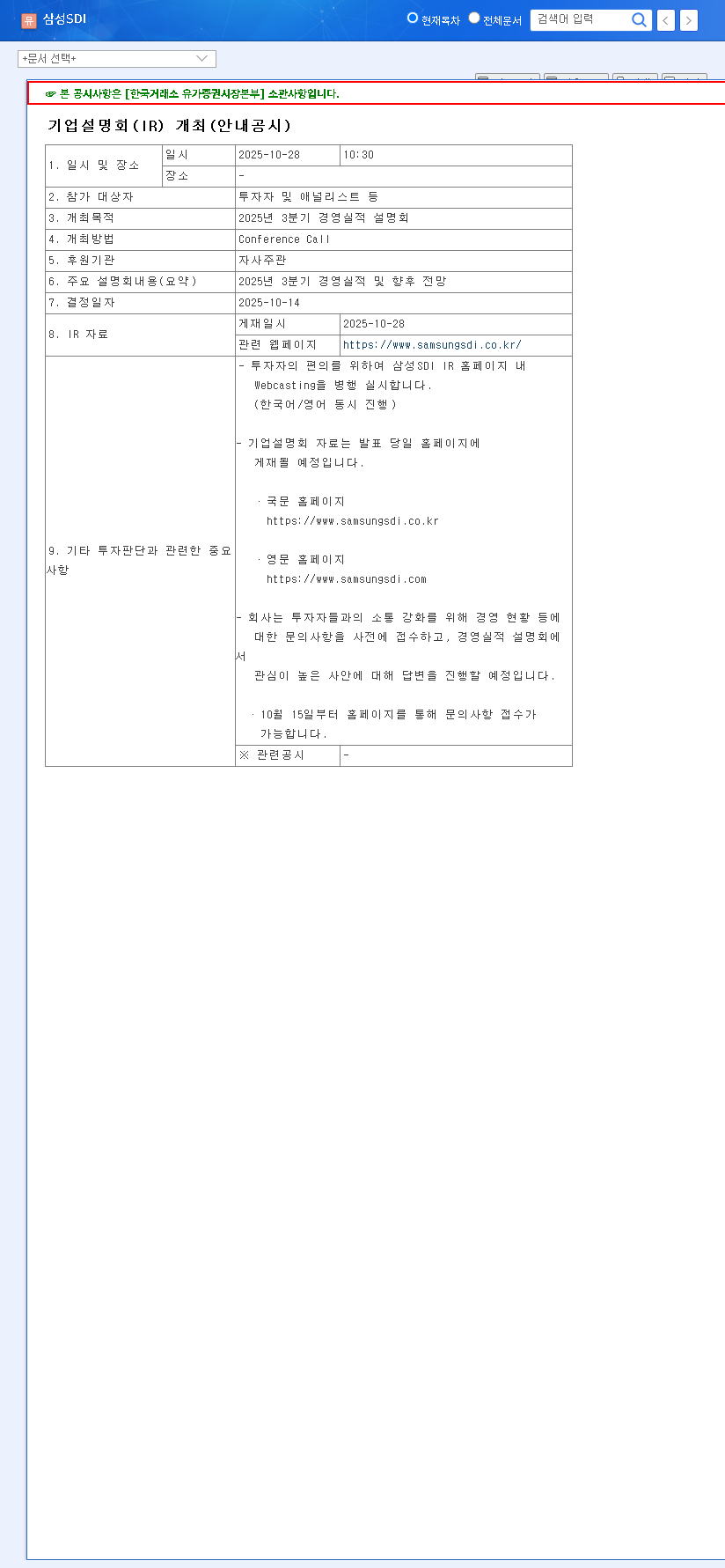

Q3 2025 Investor Relations Event Details

Samsung SDI will present its quarterly performance and provide crucial updates on its strategic direction. This event is a key opportunity for management to address investor concerns directly.

- •Company: SAMSUNG SDI CO.,LTD (006400)

- •Event: Q3 2025 Investor Relations (IR) Conference

- •Date & Time: October 28, 2025, 10:30 AM (KST)

- •Purpose: Announce Q3 2025 financial results and discuss the future business outlook.

- •Official Source: Investors can review the Official Disclosure on DART for formal documentation.

Deep Dive: SAMSUNG SDI CO.,LTD’s Core Business Segments

The company’s performance is driven by two distinct divisions, each facing its own set of opportunities and challenges. A thorough Samsung SDI stock analysis requires understanding the dynamics of both.

1. Energy Solution Division (93% of Sales)

This division, the company’s primary revenue engine, encompasses batteries for electric vehicles (EVs), energy storage systems (ESS), and small-sized applications. The first half of 2025 was tough, with sales down 28.6% and a significant operating loss. The low utilization rate for small-sized batteries (44%) has been a major drag on profitability.

Despite near-term headwinds in the EV market, the long-term electrification trend remains intact. The key question for Samsung SDI is how it will navigate the current slowdown and capture growth in burgeoning areas like grid-scale ESS.

Key factors to watch include progress on its all-solid-state battery technology, securing new long-term orders from major automakers, and strategies to improve capacity utilization. The global EV market is becoming increasingly competitive, with rivals like LG Energy Solution and CATL expanding aggressively. For more context, you can read about the global trends in the EV battery industry.

2. Electronic Materials Division (7% of Sales)

While smaller, this division is a high-margin business focused on semiconductor and display materials. The decision to divest its polarizing film business signals a strategic shift to concentrate on higher-growth areas. The explosive demand for AI is a significant tailwind, driving growth in materials used for advanced semiconductors and HBM (High-Bandwidth Memory).

Investors will look for commentary on how Samsung SDI plans to capitalize on the AI boom and what new material innovations are in the pipeline. This division’s consistent profitability provides a crucial buffer against the volatility in the Energy Solution segment. For more on this sector, see our guide on investing in the semiconductor supply chain.

Financial Health and Strategic Outlook

In May 2025, SAMSUNG SDI CO.,LTD successfully raised KRW 1.65 trillion through a rights offering. These funds are being deployed into aggressive facility investments, primarily to expand battery production capacity. While this dilutes existing shareholders in the short term, it’s a necessary step to secure long-term growth.

The Samsung SDI future outlook will be heavily influenced by how efficiently this new capital is used to generate returns. The IR presentation must provide clear metrics and timelines for these investments to reassure the market.

Key Questions for the IR Conference

- •What is the concrete plan to improve the utilization rate of the small-sized battery lines?

- •Can you provide an updated timeline for the mass production of all-solid-state batteries?

- •How is the new order pipeline for EV batteries shaping up for 2026 and beyond?

- •What are the expected synergies and profitability improvements from the Electronic Materials business restructuring?

Investment Thesis and Recommendation

Currently, a ‘Hold’ recommendation seems prudent for 006400. The company possesses undeniable long-term growth potential, underpinned by its technological prowess and strategic investments. However, significant short-term uncertainties and profitability challenges cloud the immediate outlook.

The upcoming Q3 2025 IR is the critical catalyst. A convincing presentation that addresses the key questions above and provides a clear, credible path to improved profitability could shift this rating to a ‘Buy’. Conversely, a lack of clarity or further negative guidance could increase downside risk.

Disclaimer: This analysis is for informational purposes only and is not investment advice. All investment decisions should be made based on your own research and risk tolerance.