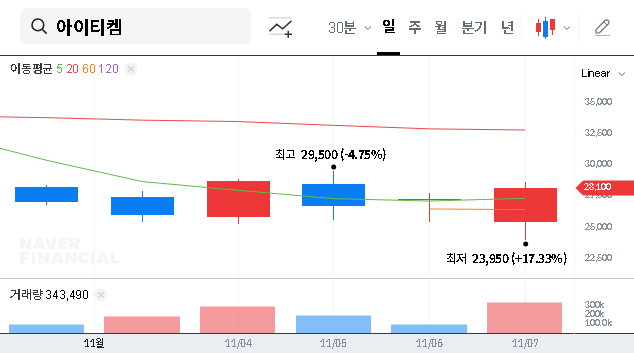

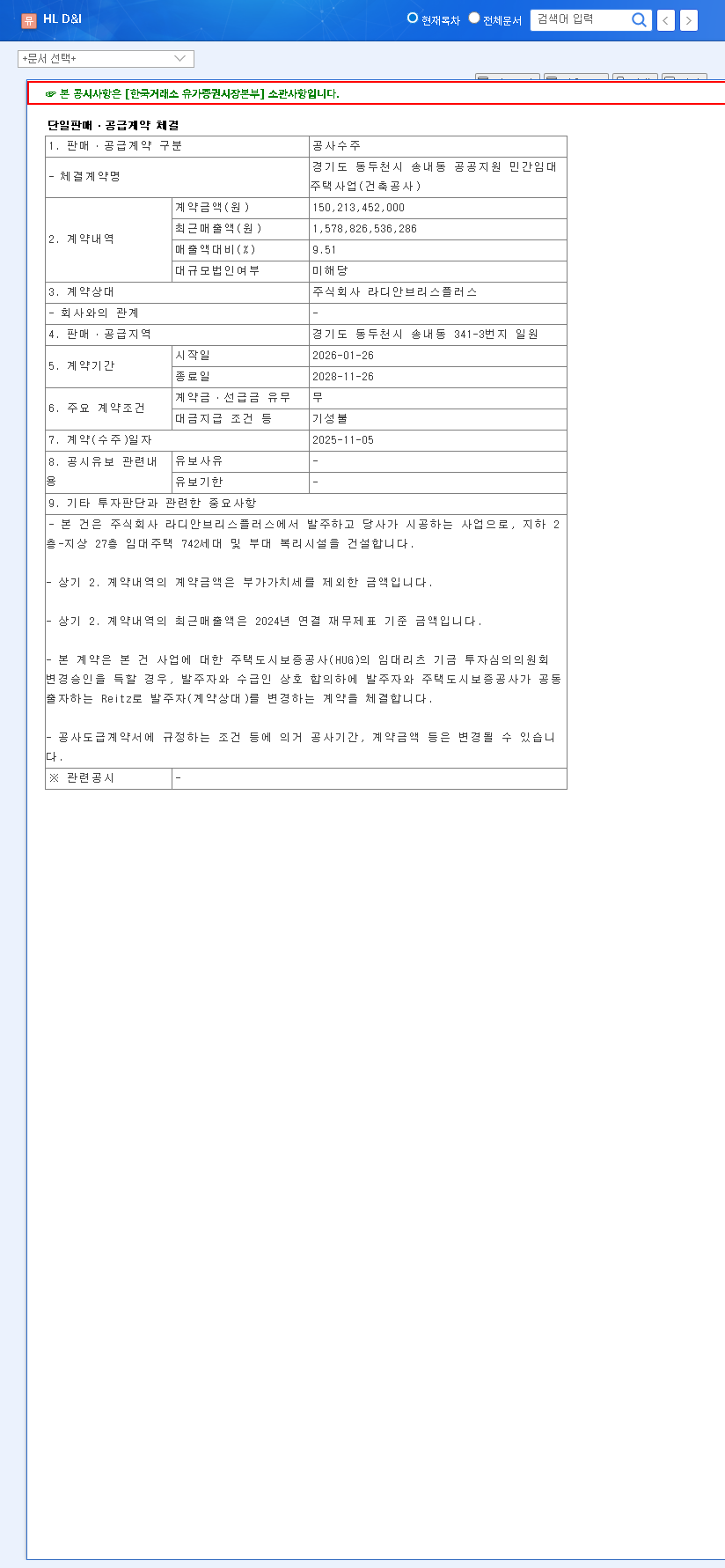

A recent major development has put HL D&I HALLA CORPORATION (014790) back in the spotlight for investors. The company has successfully secured a massive ₩90 billion public contract, a move that could significantly impact its trajectory. While this news injects a dose of optimism, a thorough HL D&I investment analysis reveals a complex picture fraught with both opportunity and considerable risk. This article will dissect the contract’s implications, examine the company’s underlying financial health, and provide a clear-eyed guide for potential investors evaluating the HL D&I stock.

Unpacking the ₩90 Billion Public Contract

On November 13, 2025, HL D&I HALLA CORPORATION formally announced the ₩90 billion deal with the Armed Forces Financial Management Corps. The project, officially titled the ’24-N-00 Base Mooring Facility Expansion’, is a significant civil engineering endeavor. According to the Official Disclosure, this contract value represents about 5.70% of the company’s revenue from the first half of 2025. Spanning a three-year period until November 2028, this project promises a steady, long-term revenue stream. Mooring facilities are critical infrastructure for naval bases, and this expansion likely involves significant construction and engineering expertise, validating the company’s capabilities in the public sector.

Public sector contracts offer more than just revenue; they provide a bedrock of stability in the often-turbulent construction industry, shielding companies from the volatility of the private real estate market.

The Bull Case: Why This Contract Fuels Optimism

Revenue Injection and Growth Momentum

In an economic climate where the private construction segment faces headwinds from rising interest rates and slowing demand, this HL D&I public contract is a timely boost. It provides a predictable revenue pipeline for the next three years, offering a counter-balance to potential softness in other areas and establishing a new engine for growth.

Portfolio Diversification and Stability

Over-reliance on the private housing market is a significant risk for any construction firm. By winning a substantial government contract, HL D&I HALLA CORPORATION strategically diversifies its portfolio. Public infrastructure projects are generally less susceptible to economic cycles, thereby enhancing the company’s overall business stability and resilience.

Enhanced Corporate Credibility

Securing a large-scale project from a government entity like the Armed Forces Financial Management Corps is a powerful endorsement of a company’s technical capabilities and reliability. This enhances corporate image and can be a significant advantage in bidding for future projects, both public and private.

The Bear Case: Analyzing the Underlying Risks

The Burden of a High Debt-to-Equity Ratio

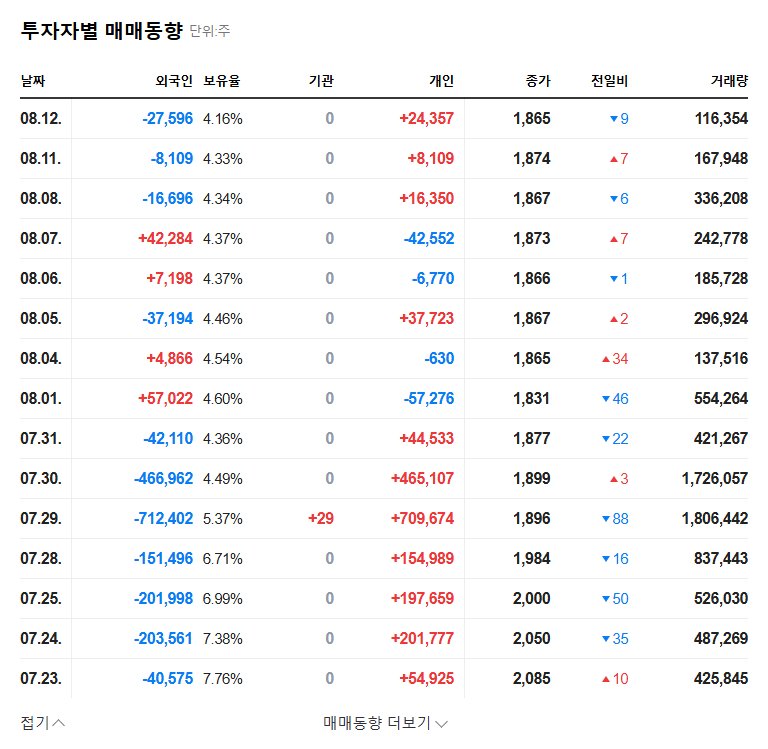

Despite the positive news, investors cannot ignore the company’s precarious financial position. As of H1 2025, HL D&I reported a debt-to-equity ratio of 305%. This figure, explained in detail on sites like Investopedia, indicates that the company is heavily leveraged, relying far more on debt than equity to finance its assets. Such high leverage increases financial risk, making the company vulnerable to interest rate hikes and economic downturns.

Surging Inventory and Profitability Pressures

Another red flag is the 239% surge in inventory. This could signal unsold properties or an accumulation of raw materials, tying up capital and potentially leading to write-downs. Furthermore, the construction industry is battling soaring costs for materials and labor. Without meticulous cost management, the profitability of this new ₩90 billion contract could be severely eroded, a key concern in any HL D&I investment analysis.

An Investor’s Guide to HL D&I (014790)

Given this complex backdrop, a cautious and informed approach is essential. Investors should actively monitor the following areas:

- •Financial Deleveraging Efforts: Watch for any strategic plans or actions aimed at reducing the high debt-to-equity ratio. This is the most critical factor for long-term stability.

- •Operating Cash Flow: Scrutinize quarterly reports to see if the company is generating positive cash flow from its operations, which is crucial for servicing debt and funding growth.

- •Profit Margins on New Projects: Pay close attention to the profitability of the civil engineering segment to see if the company is effectively managing rising construction costs.

- •Growth in Non-Construction Segments: Stable performance in its logistics, port, and environmental businesses can provide a buffer. To learn more, read our guide on how to analyze a diversified industrial company.

Conclusion: A Cautiously Optimistic Outlook

In conclusion, the ₩90 billion contract is undeniably a positive catalyst for HL D&I HALLA CORPORATION. However, it is not a silver bullet. The deep-seated financial risks, particularly the high debt load, remain a significant concern that could overshadow the benefits. For investors, the path forward requires diligent monitoring of the company’s efforts to improve its financial health while executing successfully on this new opportunity.

Frequently Asked Questions (FAQ)

What is the ₩90 billion contract secured by HL D&I HALLA CORPORATION?

It is a public civil engineering contract with the Armed Forces Financial Management Corps for the ’24-N-00 Base Mooring Facility Expansion’ project. The contract is valued at ₩90 billion and will be executed over a three-year period.

What are the potential benefits of this contract for HL D&I?

The primary benefits include securing a stable revenue stream, diversifying the business away from the volatile private market, boosting growth momentum, and enhancing the company’s corporate image and credibility for future projects.

What are the main risks associated with investing in HL D&I stock?

The most significant risks are structural and financial. These include a very high debt-to-equity ratio (305%), a recent and dramatic surge in inventory levels, ongoing profitability challenges due to rising construction costs, and several outstanding lawsuits.

What should investors monitor regarding HL D&I HALLA CORPORATION?

Investors should closely track key financial health indicators, such as changes in the debt ratio, inventory levels, and operating cash flow. It’s also vital to assess the company’s ability to manage costs, the profitability of new contracts, and the performance of its non-construction business segments.

![(000370) Hanwha General Insurance: K-ICS Stability Analysis & Carrot Subsidiary Risk [2025 Investor Deep Dive]](https://note12345-images.s3.ap-southeast-2.amazonaws.com/wp-content/uploads/2025/11/12202007/000370.png)

![(000370) Hanwha General Insurance: K-ICS Stability Analysis & Carrot Subsidiary Risk [2025 Investor Deep Dive] 관련 이미지](http://note12345-images.s3.ap-southeast-2.amazonaws.com/wp-content/uploads/2025/11/12202010/000370_%EA%B3%B5%EC%8B%9C.png)