The latest DK-Lok Corporation Q3 2025 earnings report, released on November 11, 2025, sent a significant ripple through the market. After a challenging second quarter, the company posted a remarkable turnaround with impressive revenue and profit figures. But does this signal a sustainable recovery and a new growth phase, or is it merely a temporary reprieve from underlying issues? This comprehensive DK-Lok financial analysis will dissect the quarterly results, explore the positive catalysts and persistent risks, and provide a clear investment outlook for the future.

Breaking Down the DK-Lok Corporation Q3 2025 Earnings Report

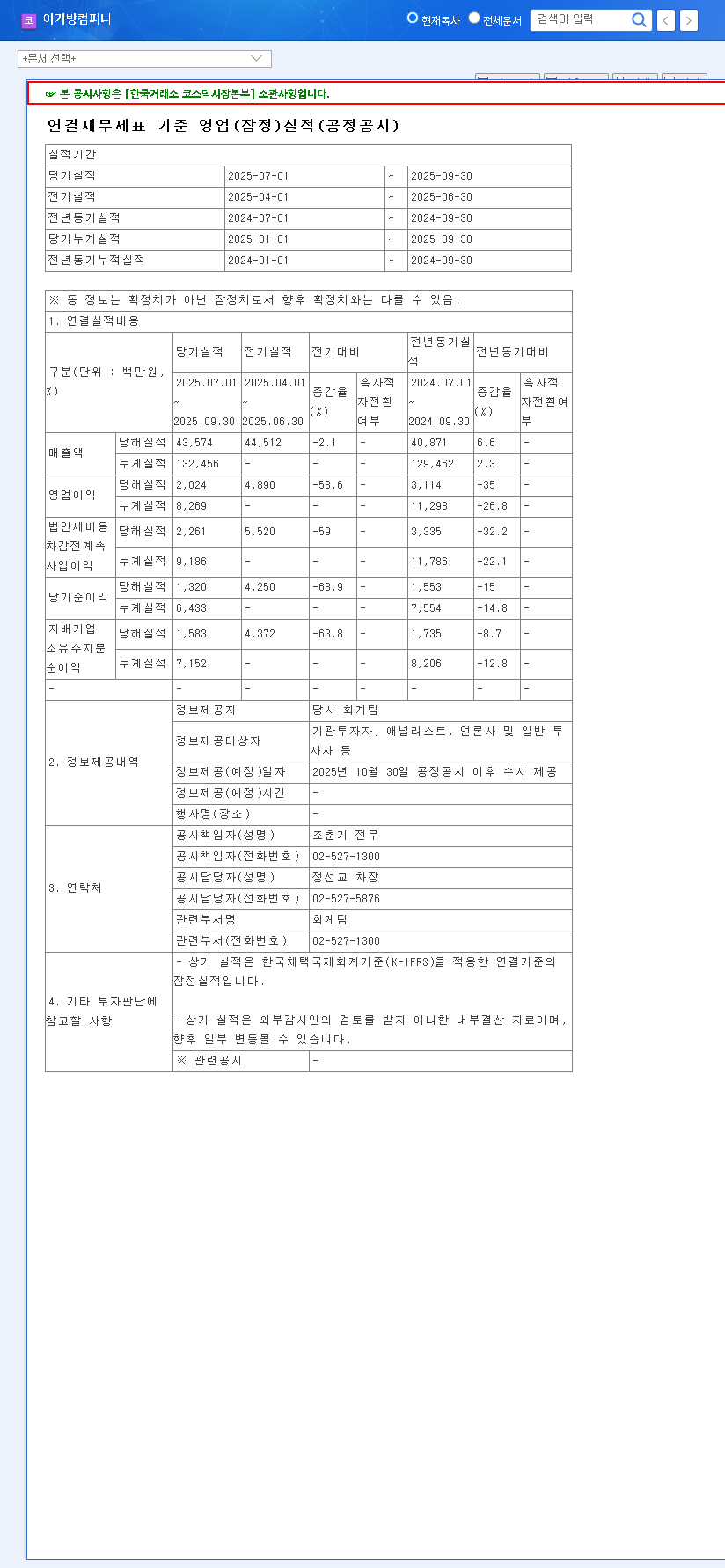

DK-Lok Corporation announced a significant performance rebound in its preliminary third-quarter results, a stark contrast to the sluggish performance seen in Q2 2025. The numbers paint a picture of a company returning to strong profitability. The official data can be reviewed in the company’s disclosure. (Source: Official Disclosure).

Key Financial Highlights (Consolidated)

- •Revenue: 37.6 billion KRW (up from 30.6 billion in Q2)

- •Operating Profit: 6.7 billion KRW (a significant swing from 0.3 billion in Q2)

- •Net Profit: 7.8 billion KRW (a dramatic recovery from a -4.3 billion loss in Q2)

The most striking figure is the operating profit margin, which soared to approximately 17.8%, a massive leap from the razor-thin 0.98% margin in the previous quarter. This suggests a powerful combination of increased sales volume, better cost controls, or a more favorable product mix.

The Bull Case: Catalysts for Sustained Growth

Solid Domestic Demand & Global Competitiveness

Even before this quarter, DK-Lok showed strength in its home market, with domestic sales growing 15.11% in the first half of 2025. This provides a stable foundation. Crucially, the company is not just a domestic player. With an export ratio of approximately 74%, DK-Lok has proven its ability to compete and win on the global stage against industry giants, demonstrating the quality and cost-effectiveness of its precision fittings and valves.

Future-Proofing through High-Growth Industries

DK-Lok is actively positioning itself at the forefront of technological innovation. The company’s focus on new product development for high-growth sectors is a key pillar of its long-term strategy. This includes:

- •Hydrogen: Developing specialized valves and fittings capable of handling the high pressures and unique properties of hydrogen gas for fueling stations and transport.

- •Electric Vehicles (EVs): Supplying components for battery cooling systems and other fluid management applications within EV manufacturing.

- •Semiconductors: Providing ultra-high-purity (UHP) fittings and valves essential for the manufacturing of next-generation microchips.

While the Q3 turnaround is impressive, the core question for investors is whether the fundamental issues, particularly with the overseas subsidiary, have been resolved or simply masked by a strong quarter.

The Bear Case: Persistent Risks and Headwinds

The Drag from Overseas: VALVOMETAL ITALY

The primary cause of the consolidated net loss in the first half of 2025 was the significant underperformance of its Italian subsidiary, VALVOMETAL ITALY. The Q3 report does not specify if this subsidiary’s profitability has fundamentally improved. Without a structural fix, this remains a major source of potential volatility that could erase gains in future quarters. Investors should seek clarity on the turnaround plan for this specific unit.

Financial and Macroeconomic Pressures

Several financial metrics warrant caution. Inventory levels rose significantly to 59.38 billion KRW, which could signal sales forecasting issues or tie up valuable cash. Additionally, increased borrowing for factory expansion, while necessary for growth, adds to financial risk, especially in a rising interest rate environment. The company is also highly sensitive to foreign exchange volatility; a 5% swing in exchange rates could impact pre-tax profit by over 2.1 billion KRW. For more on this, investors can read about managing currency risk in international stocks.

Investment Outlook and Final Verdict

The strong DK-Lok Corporation Q3 2025 earnings create a positive short-term narrative. However, a prudent DK-Lok investment strategy requires a long-term view. The positive momentum from new growth sectors is promising, but it’s weighed down by the unresolved issues at its Italian subsidiary and various financial pressures. As reported by leading financial news outlets like Bloomberg, market sentiment often depends on the sustainability of such turnarounds.

Therefore, our DK-Lok stock outlook remains “Neutral.” An upgrade to a more bullish stance would be contingent on clear evidence of:

- •A sustainable turnaround in the profitability of VALVOMETAL ITALY.

- •Effective management and reduction of elevated inventory levels.

- •Tangible revenue contributions from the hydrogen, EV, and semiconductor initiatives.

Frequently Asked Questions (FAQ)

Q1: How did DK-Lok Corporation perform in Q3 2025?

A1: DK-Lok Corporation showed a significant rebound in Q3 2025, reporting revenue of 37.6 billion KRW, operating profit of 6.7 billion KRW, and net profit of 7.8 billion KRW. This marked a successful return to profitability after a difficult second quarter.

Q2: What are the key risks for a DK-Lok investment?

A2: The primary risks include continued losses from its overseas subsidiary (VALVOMETAL ITALY), the impact of high currency exchange rate volatility, the financial burden from high inventory levels, and increased borrowing for expansion.

Q3: What are DK-Lok Corporation’s long-term growth drivers?

A3: Long-term growth is expected to come from its strong global export market and strategic product development in high-growth industries, including hydrogen, electric vehicles, and semiconductors, which require specialized, high-quality fittings and valves.