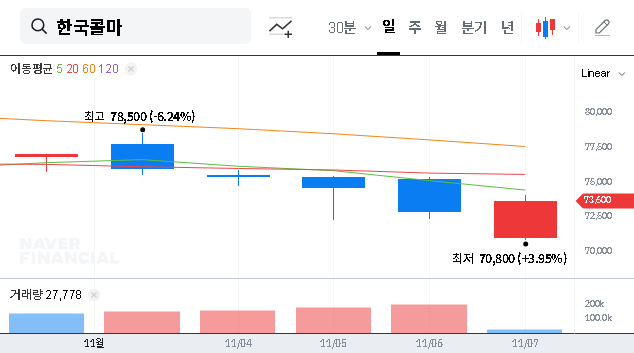

The recent KOLMAR KOREA earnings shock for Q3 2025 has sent ripples through the investment community. On November 7, 2025, the cosmetics ODM and pharmaceutical giant released preliminary figures that starkly missed market expectations, triggering immediate concern over the company’s trajectory and the stability of KOLMAR KOREA stock. With revenue plummeting to less than half of forecasts and profits taking a significant hit, investors are left asking critical questions. What’s behind this sudden downturn, and what does it mean for the company’s future? This analysis provides a comprehensive breakdown of the situation and offers a clear, strategic path forward for investors.

Deconstructing the Q3 2025 Earnings Shock

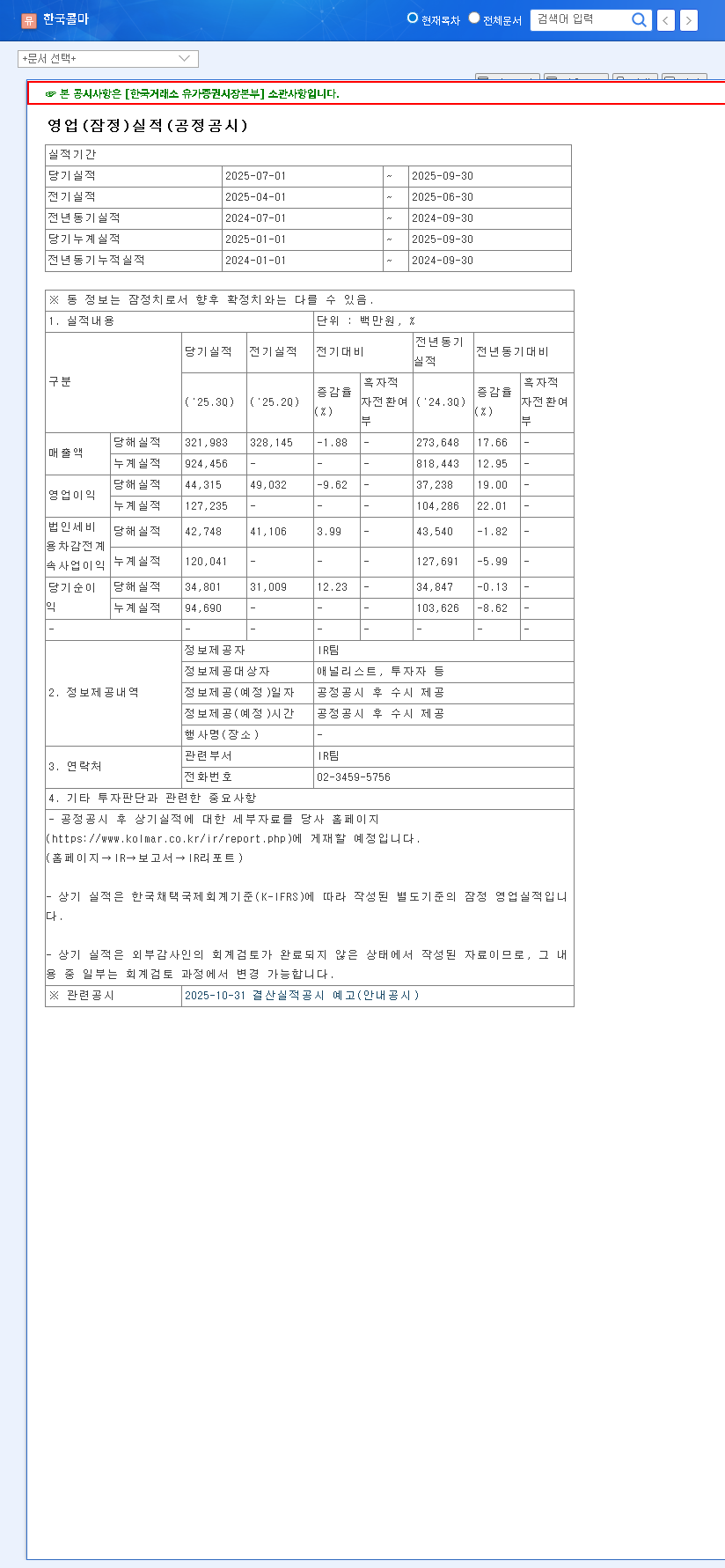

An ‘earnings shock’ occurs when a company’s reported earnings are dramatically different from what analysts and the market predicted. In KOLMAR KOREA’s case, the deviation was substantial, painting a concerning picture for the third quarter. Let’s examine the numbers in detail:

- •Revenue: Reported KRW 322 billion, a staggering 54% below the forecasted KRW 695.2 billion.

- •Operating Profit: Came in at KRW 44.3 billion, which is 34% lower than the expected KRW 67.5 billion.

- •Net Profit: Registered KRW 34.8 billion, falling 11% short of the KRW 39.3 billion consensus.

These figures not only represent a significant miss against forecasts but also a sharp decline from the previous quarter’s solid performance (Q2 2025 revenue was KRW 730.8 billion). This sudden reversal calls for a deep re-evaluation of the company’s operational health and market position.

Analyzing the Root Causes of the Slump

To formulate a sound investment strategy, we must first understand the potential drivers behind this poor performance. The issues likely stem from a combination of internal challenges and external pressures.

Challenges in Core Business Divisions

KOLMAR KOREA’s strength lies in its diverse portfolio, with cosmetics ODM (Original Design Manufacturing) and pharmaceuticals as its primary pillars. Such a drastic revenue drop suggests a severe issue in one or both of these key areas. Potential problems could include the loss of a major client, significant production delays, unexpected weakness in demand from key markets, or intensifying competition from other ODM players. A detailed breakdown in the final report is needed to pinpoint the exact source of the weakness.

Macroeconomic and Industry Headwinds

While favorable exchange rates (rising EUR/KRW and USD/KRW) should theoretically benefit an exporter like KOLMAR KOREA, they were clearly not enough to offset the negative factors. The performance is particularly puzzling given the continued global popularity of K-beauty and the steady growth in the pharmaceutical sector. This suggests that company-specific issues may outweigh broader industry trends. Furthermore, rising raw material costs, global supply chain disruptions, and increased logistics expenses could have squeezed profit margins more than anticipated.

The magnitude of this earnings miss suggests that the challenges are likely more structural than temporary. Investors should be prepared for a period of heightened volatility and downward revisions from market analysts.

Stock Impact and Future Outlook

The immediate impact of the KOLMAR KOREA earnings shock will almost certainly be negative pressure on its stock price. Investor confidence is fragile, and such a significant deviation from expectations can trigger a wave of selling. The market will be looking for clear, decisive action from management to address the underlying problems. The company’s recovery potential is high, given its R&D capabilities and global footprint, but it is contingent on a transparent explanation and a credible turnaround plan. For precise figures and official statements, investors should refer to the company’s Official Disclosure on DART.

A Smart Investment Strategy for KOLMAR KOREA Stock

In light of these events, a reactive approach is risky. A disciplined, informed strategy is essential. Here are key steps for investors to consider:

- •Practice Patience and Observation: Avoid the temptation to ‘buy the dip’ prematurely. It’s crucial to wait for the dust to settle. Monitor the company’s official full earnings release, conference call, and subsequent management communications for clarity.

- •Dive Deep into the ‘Why’: Focus on understanding the precise reasons for the slump. Was it a one-off event like a delayed shipment, or a more profound issue like the loss of a key client? The answer will heavily influence the long-term outlook for the KOLMAR KOREA stock.

- •Benchmark Against Competitors: Analyze the performance of other players in the cosmetics ODM space. Are they facing similar headwinds, or is this a KOLMAR-specific problem? This context is critical for assessing its competitive standing. For more information, you can check reports from leading financial news outlets.

- •Review Financial Health: Scrutinize the company’s balance sheet. Pay close attention to debt levels, cash flow, and liquidity ratios to ensure the company can weather this storm without significant financial distress. Our guide on how to perform fundamental analysis can help.

- •Adopt a Long-Term View: Base your final investment decision on the company’s fundamental long-term value, including its R&D pipeline and global expansion plans, rather than short-term price movements caused by the recent earnings shock.

In conclusion, the Q3 2025 KOLMAR KOREA earnings shock presents a significant short-term risk. A conservative and analytical approach is the most prudent course of action until management provides a clear explanation and a viable strategy for returning to a path of sustainable growth.