The K-beauty industry is buzzing with a significant development: the potential ABLE C&C A’pieu sale. News that the parent company is considering the divestment of its popular, youth-focused brand ‘A’pieu’ signals a critical strategic shift. This decision could profoundly reshape ABLE C&C’s future, impacting its financial stability, market focus, and ultimately, its value to investors. This analysis explores the driving forces behind this move, its potential consequences, and what stakeholders should watch for next.

On July 18, 2025, ABLE C&C confirmed it was exploring strategic options for the A’pieu brand, appointing Samjong KPMG as an advisor. According to the Official Disclosure filed, no final decisions have been made, with a follow-up announcement expected within six months. This move has understandably captured the market’s attention, given A’pieu’s role as a past growth engine for the company.

Why Consider the A’pieu Brand Sale Now?

The rationale behind the potential A’pieu brand sale is a complex mix of internal financial pressures and external market dynamics. ABLE C&C is navigating a challenging landscape that demands decisive action to ensure long-term sustainability and growth.

Internal Financial Realities

While the company has shown positive signs, such as revenue recovery driven by a high export ratio (44.71% in Q3 2025) and an improved capital structure, underlying issues persist. Key challenges include:

- •Declining Profitability: A consistent decrease in consolidated operating profit and margins is a major concern, suggesting that top-line growth isn’t translating to bottom-line health.

- •Asset Management Inefficiency: Challenges in managing accounts receivable and high inventory levels can tie up valuable capital and indicate potential issues with sales velocity or demand forecasting.

- •Currency Exposure: Heavy reliance on exports makes the company vulnerable to performance risks from exchange rate volatility, particularly with the KRW against the EUR and USD.

Evolving and Competitive Market Trends

The global cosmetics market is fiercely competitive and evolving at a rapid pace. According to market analysis from sources like Forbes, trends are shifting quickly. Key factors influencing the ABLE C&C investment strategy include:

- •The Rise of Gen Z: Younger consumers (MZ/Z generations) demand authenticity, sustainability (clean beauty), and a strong digital presence. Brands must constantly innovate to remain relevant, which requires significant investment.

- •Channel Shift: The dominance of online and direct-to-consumer channels necessitates a different marketing and distribution playbook compared to traditional retail.

- •Macroeconomic Headwinds: High interest rates increase the cost of capital, while global economic uncertainty can dampen consumer spending on non-essential goods.

Potential Impacts of the ABLE C&C A’pieu Sale

Selling A’pieu is a double-edged sword, presenting both significant opportunities and risks that could redefine ABLE C&C’s trajectory.

The proposed sale represents a strategic choice: streamline operations and focus on core strengths, or risk diluting resources across a portfolio that may not be fully optimized for future market conditions.

The Upside: A Leaner, Stronger ABLE C&C

- •Enhanced Financial Health: A successful sale would inject significant capital, allowing the company to pay down debt, strengthen its balance sheet, and fund new growth initiatives.

- •Sharpened Business Focus: Divesting A’pieu would allow management to concentrate resources—financial and human—on its flagship brand, MISSHA, potentially accelerating its growth. Learn more about their existing plans in our article on MISSHA’s Global Strategy.

- •Positive Market Perception: A well-executed sale could be viewed by the market as a decisive and smart strategic move, potentially boosting investor confidence and the stock price.

The Downside: Potential Pitfalls

- •Revenue Contraction: An immediate drop in total revenue is unavoidable. If A’pieu represents a substantial portion of sales, it could weaken the company’s overall market presence.

- •Erosion of Brand Portfolio: The sale could damage corporate image and create a perception of a shrinking empire, potentially affecting the value and appeal of the remaining brands.

- •Execution Risk: The sale process itself carries risks, including restructuring costs, uncertainty about the final price and buyer, and potential for a prolonged period of instability.

Investor Action Plan: A Time for Cautious Observation

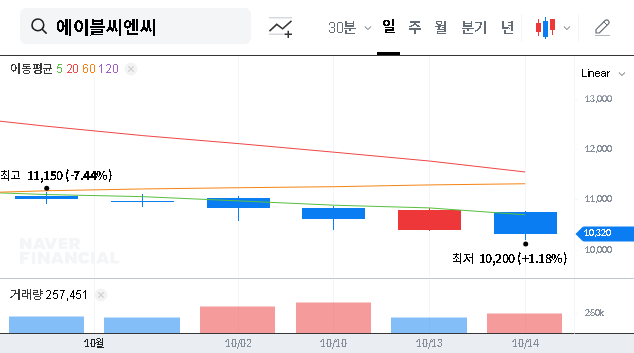

Given the mix of potential outcomes from the ABLE C&C A’pieu sale, a ‘Neutral’ and watchful stance is advisable. In the short term, investors should anticipate stock price volatility as news develops. The key will be the specifics of the deal, which are expected within six months.

For a long-term perspective, the focus must be on ABLE C&C’s post-sale strategy. How will the capital be deployed? Will it be used to innovate within MISSHA, acquire a new high-growth brand, or simply pay down debt? The company’s ability to address its fundamental challenges—profitability, asset management, and global market positioning—will ultimately determine whether this strategic pivot is a success. Careful monitoring of future disclosures is essential for making an informed investment decision.