The precarious situation for GW Vitek CO.,LTD., a company already navigating treacherous corporate rehabilitation proceedings, has intensified significantly. A newly emerged appeal for a KRW 3.841 billion goods payment lawsuit casts a dark, ominous shadow over its prospects for recovery. This development introduces a critical layer of uncertainty that investors and stakeholders cannot afford to ignore. This comprehensive analysis will dissect the lawsuit’s implications for GW Vitek, its fragile financial state, and the viability of its entire rehabilitation process.

The New Legal Hurdle: A KRW 3.8 Billion Lawsuit

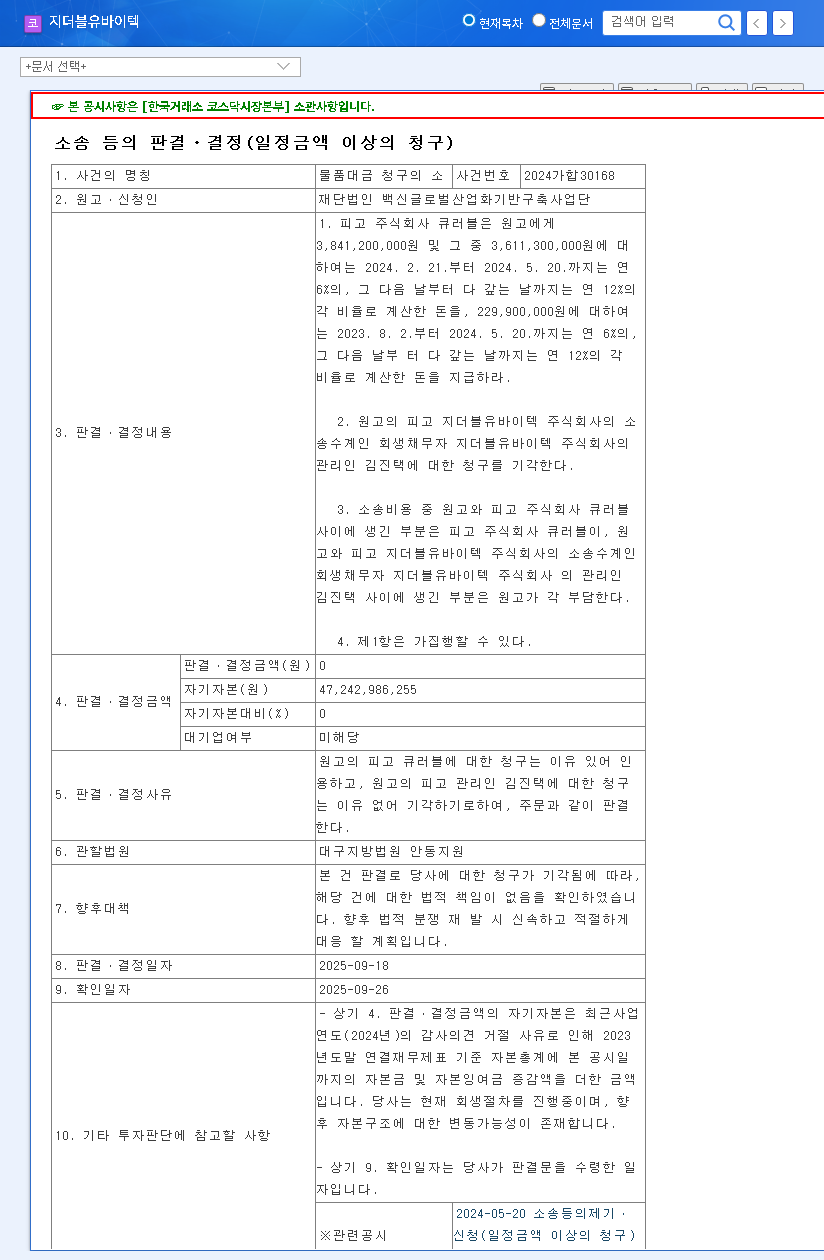

Already burdened by severe management challenges and suspended stock trading, GW Vitek now confronts another significant legal battle. The Vaccine Global Industrialization Foundation has filed an appeal for a ‘claim for goods payment’ lawsuit valued at KRW 3.841 billion. This amount represents a substantial 7.62% of the company’s total assets, making it a material event with potentially devastating consequences.

The appeal, which will be heard at the Andong Branch of the Daegu District Court, seeks to overturn a first-instance ruling where the plaintiff was unsuccessful. If the appeal succeeds, this KRW 3.841 billion will be confirmed as a rehabilitation claim, adding a massive financial weight to a company already on the brink. The specifics of this legal challenge were disclosed in an official regulatory filing. You can view the Official Disclosure (Source) for detailed information.

Understanding the Gravity: GW Vitek’s Deep-Rooted Crisis

To fully appreciate the impact of this lawsuit, it’s essential to understand the dire state of GW Vitek’s fundamentals. The company is operating under extreme ‘going concern uncertainty,’ a term auditors use when a business is at high risk of failure. This isn’t a new development but a culmination of persistent financial decay.

With liabilities soaring and equity diminishing, the addition of a multi-billion KRW claim from this GW Vitek lawsuit could be the final straw that breaks the company’s chances of a successful turnaround.

Catastrophic Financial Performance

The company’s financial reports paint a grim picture. In Q3 2025, accumulated sales plummeted to KRW 3.25 billion, an 85% decrease year-over-year, while the operating loss ballooned to KRW 3.27 billion. More alarmingly, total liabilities stand at a staggering KRW 136.4 billion against a dwindling total equity of just KRW 15.048 billion, signaling severe capital impairment and a desperate need for restructuring. These are not just numbers; they represent a fundamental collapse of the business’s operational viability.

Compounding Internal and External Pressures

The problems extend beyond poor sales. GW Vitek is also dealing with the fallout from alleged embezzlement and breach of trust, resulting in outstanding illegal activity receivables of KRW 18.33 billion. This, combined with numerous other ongoing lawsuits and the loss of control over subsidiaries, has created a perfect storm. The auditor’s ‘disclaimer of opinion’ underscores the chaos, making it nearly impossible for investors to trust the financial statements. Furthermore, the harsh macroeconomic climate of high interest rates and inflation makes sourcing capital or finding operational efficiencies incredibly challenging. For more information on navigating such situations, investors can review resources on analyzing distressed companies.

How the Lawsuit Derails the Rehabilitation Process

The success of corporate rehabilitation proceedings hinges on creating a clear and viable path forward. This new lawsuit threatens to shatter that clarity in several ways:

- •Exacerbated Financial Burden: If the court rules against GW Vitek, its already overwhelming debt load will increase, making financial restructuring nearly impossible and potentially triggering liquidation.

- •Deterrent to M&A and Investment: Potential buyers or investors seek stability. A large, unresolved legal claim is a major red flag, significantly reducing the chances of a successful M&A deal that could save the company.

- •Damaged Corporate Trust: Continuous legal disputes destroy a company’s reputation. Even if GW Vitek somehow survives, rebuilding trust with customers, suppliers, and the market will be a monumental task.

- •Complicated Rehabilitation Plan: The entire rehabilitation plan submitted to the court is now thrown into question. Creditors will be less likely to approve a plan when a massive, uncertain liability is looming.

Conclusion: An Extremely High-Risk Scenario for Investors

The emergence of this KRW 3.841 billion ‘claim for goods payment’ lawsuit is a profoundly negative event for GW Vitek. It compounds an existing crisis defined by rehabilitation proceedings, suspended trading, embezzlement-related debts, and a damning auditor’s report. The path to normalization now appears more obscured than ever.

Therefore, any investment consideration in GW Vitek at this juncture carries an exceptionally high level of risk. Investors must exercise extreme caution and diligently monitor all developments. A prudent approach is not just recommended; it is essential for capital preservation. Focus on the outcome of this lawsuit and the progress of the rehabilitation plan, as these will be the ultimate determinants of the company’s fate.