The recent news surrounding DMS Co.,Ltd. (DMS) presents a classic case of conflicting signals for investors. While a newly announced supply contract with industry giant LG Display seems positive on the surface, a much more sinister issue lurks within its financial reporting: a critical auditor’s disclaimer of opinion. This analysis unpacks the details of the contract, the severe implications of the audit issue, and DMS’s deteriorating financial health to provide a clear perspective on the inherent investment risks.

This comprehensive breakdown is essential for any investor looking to understand whether the recent contract is a sign of recovery or merely a distraction from fundamental, potentially catastrophic, problems at DMS Co.,Ltd.

The LG Display Contract: A Glimmer of Hope?

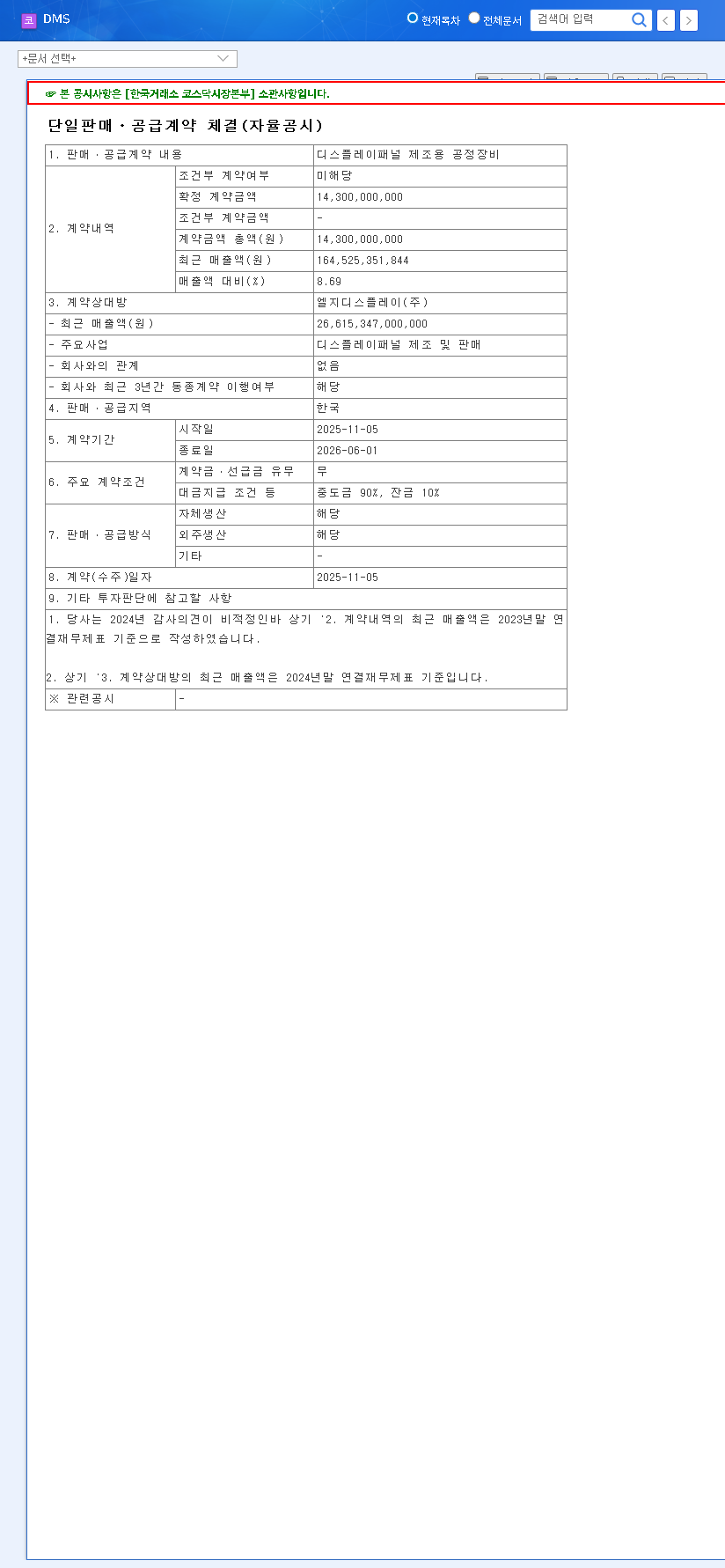

On November 6, 2025, DMS Co.,Ltd. disclosed a significant supply agreement for display panel manufacturing equipment with LG Display Co., Ltd. This deal, valued at 14.3 billion KRW, represents approximately 8.69% of the company’s projected annual revenue. The contract period extends from November 5, 2025, to June 1, 2026. You can view the Official Disclosure on DART for more details.

Ordinarily, securing a contract with a key client like LG Display would be a bullish signal, suggesting continued operational relevance and potential for short-term revenue stability. However, this positive news is overwhelmingly overshadowed by a profound issue that strikes at the very heart of the company’s credibility.

The Critical Red Flag: DMS’s Auditor’s Disclaimer of Opinion

The most significant factor in any DMS financial analysis is the ‘auditor’s disclaimer of opinion’ issued for its financial statements as of December 31, 2024. This is not a minor concern; it is one of the most severe findings an auditor can issue and serves as a major warning to the market.

What Does a ‘Disclaimer of Opinion’ Actually Mean?

In simple terms, a disclaimer of opinion means the independent auditor was unable to gather sufficient evidence to form an opinion on the accuracy and fairness of the company’s financial statements. It’s like a doctor telling you they couldn’t complete an examination because the patient wouldn’t cooperate or the equipment was broken—you simply cannot trust any conclusions about their health. For a publicly-traded company, this is a catastrophic failure in transparency and governance.

An auditor’s disclaimer of opinion fundamentally undermines investor confidence, as it renders the company’s reported financial position and performance unreliable. This can be a direct precursor to a stock being delisted from an exchange.

In the case of DMS Co.,Ltd., the disclaimer was reportedly due to limitations regarding related-party transactions and other major audit procedures. This raises serious questions about internal controls and potential conflicts of interest. For a detailed explanation of this audit finding, you can reference this external resource on understanding audit reports from Investopedia.

Financial Health Under the Microscope

Even without the disclaimer, the financial trajectory for DMS Co.,Ltd. is alarming. The 14.3 billion KRW contract is simply not enough to reverse the significant and persistent negative trends.

- •Plummeting Revenue: Projections show a steep and continuous decline in revenue, falling from KRW 1,147.7 billion in 2022 to a forecast of just KRW 469.4 billion in 2025.

- •Profitability Collapse: The company is on track to swing from an operating profit of KRW 175.8 billion in 2022 to a projected operating loss of KRW -30.8 billion in 2025.

- •Worsening Debt Load: The debt-to-equity ratio has climbed from 92.27% to 114.65% in two years, signaling increased financial leverage and risk.

- •Negative Margins: Key metrics like net profit margin and Return on Equity (ROE) show consistently negative trends, indicating an inability to generate value for shareholders.

These metrics paint a picture of a company in severe distress, a situation that the auditor’s disclaimer of opinion only exacerbates.

Investment Recommendation: Extreme Caution Required

Considering the evidence, the DMS investment risk is exceptionally high. The positive sentiment from the LG Display contract is completely negated by the fundamental lack of financial transparency and the company’s rapid financial decline.

Key Actions for Investors:

- •Await Audit Resolution: No investment should be considered until DMS Co.,Ltd. fully resolves the issues that led to the disclaimer and receives a clean audit opinion. The company must demonstrate a commitment to transparent financial reporting.

- •Monitor Financial Turnaround: Look for multiple consecutive quarters of revenue stabilization, a return to profitability, and an improving balance sheet before re-evaluating.

- •Consider Reducing Exposure: For current investors, the risk of delisting or further value erosion is substantial. It is prudent to consider reducing or eliminating positions until there is concrete proof of a fundamental resolution. For more information, read our guide on how to analyze high-risk stocks.

In conclusion, the ‘disclaimer of opinion’ is the only story that matters for DMS Co.,Ltd. right now. Until this foundational issue of trust and transparency is rectified, any positive operational news should be viewed with extreme skepticism. A highly cautious, watch-and-wait approach is the only logical strategy.