The situation for investors in HYUNDAI FEED Inc. (016790) has escalated from concerning to critical. Already navigating treacherous waters with ongoing delisting procedures, the company has been hit by another severe blow: a provisional seizure of its major shareholder’s stock. This development compounds existing uncertainties and raises fundamental questions about the company’s viability. This in-depth analysis will dissect these crises, evaluate the company’s fragile fundamentals, and provide a clear-eyed view for investors caught in the storm.

A Company in Crisis: The Provisional Stock Seizure Explained

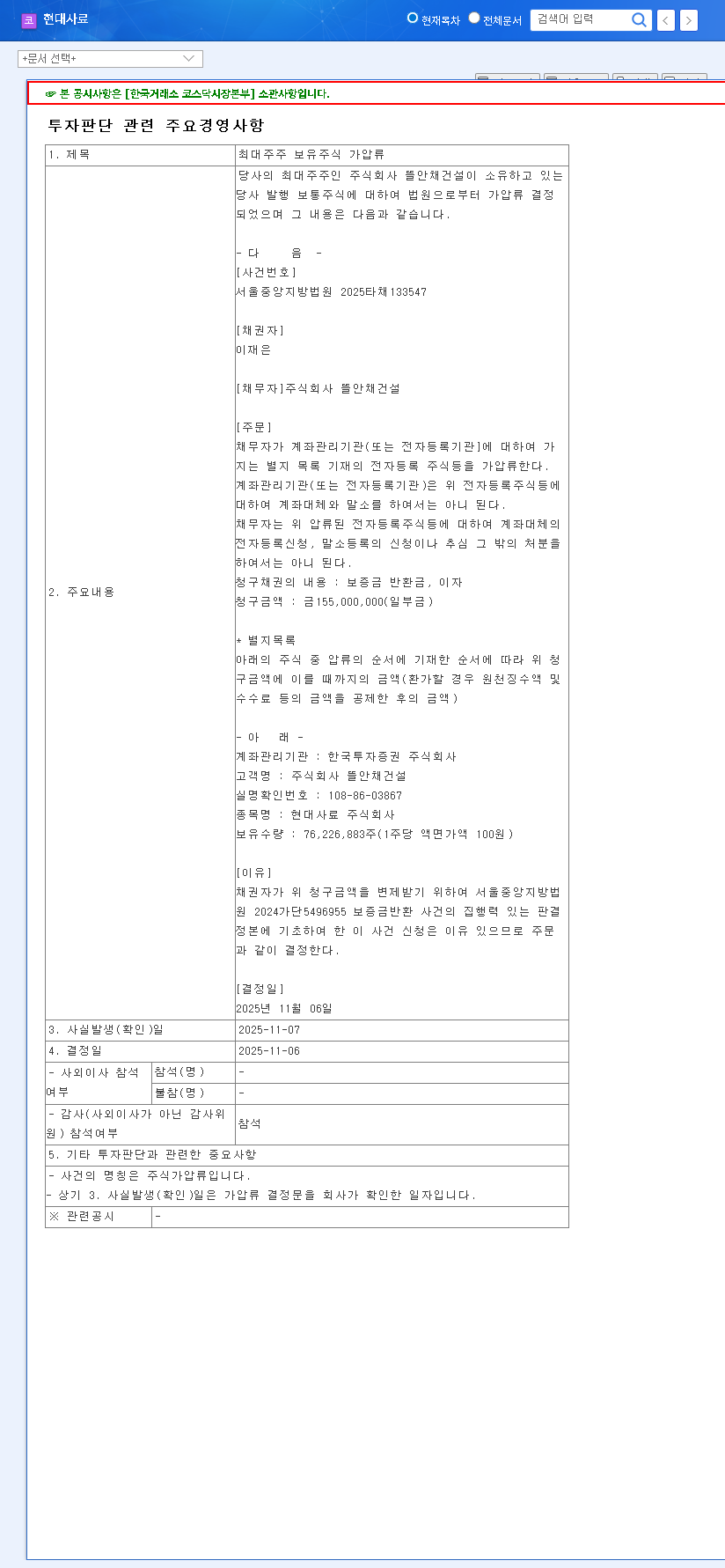

On November 7, 2025, HYUNDAI FEED Inc. made a critical disclosure that sent shockwaves through its investor base. The Seoul Central District Court enacted a provisional seizure on a substantial portion of shares held by its primary shareholder, Tteulanchae Construction Co., Ltd. This legal action effectively freezes these assets, preventing their sale or transfer pending the resolution of a financial dispute. You can view the Official Disclosure on DART for complete details.

Key Details of the Provisional Seizure:

Seized Assets: 76,226,883 common shares of HYUNDAI FEED Inc.

Debtor: Tteulanchae Construction Co., Ltd. (Major Shareholder)

Creditor: Lee Jae-eun

Claim Amount: 155,000,000 KRW (related to a deposit refund)

Legal Effect: Prohibits the disposal or transfer of the seized shares.

While the monetary claim is relatively small, the implications are vast. This event, layered on top of the existing HYUNDAI FEED Inc. delisting review, signals deep-seated instability within the company’s controlling structure and further erodes any remaining investor confidence.

Deconstructing the Cracks: HYUNDAI FEED Inc.’s Shaky Fundamentals

To understand why this provisional seizure is so damaging, we must examine the company’s underlying health. The foundation was already showing significant stress long before this latest development.

Core Business Model Under Pressure

HYUNDAI FEED Inc. has a long history in the compound feed industry, a sector that typically benefits from steady demand. However, the company faces a perfect storm of operational risks:

- •Existential Delisting Threat: The primary risk stems from a disclaimer of audit opinion in 2023, which triggered a delisting review. Trading has been suspended since February 2024, leaving shareholders in limbo.

- •Market Volatility: The business is highly sensitive to international grain prices and currency exchange rates (KRW/USD, KRW/EUR), which can severely impact profit margins.

- •Fierce Competition: The feed market is increasingly competitive, with a trend towards large-scale farms that demand lower prices and better terms, squeezing smaller players.

Financial Health Check (As of H1 2025)

Financially, the picture is mixed but ultimately precarious. While HYUNDAI FEED Inc. managed to pull itself out of full capital impairment, its recovery is fragile. Revenue has declined significantly after the divestment of its bio business. Although operating profit has shown some recovery, the recent decrease in total capital during the first half of the year is a major red flag, suggesting that the positive turn may not be sustainable.

The Ripple Effect: How the Seizure Amplifies Delisting Risks

The provisional seizure is not an isolated event; it’s a catalyst that worsens an already dire situation. Its impact will be felt across several critical areas:

- •Maximized Uncertainty: It casts severe doubt on management’s stability and control. A major shareholder entangled in personal financial disputes undermines the entire corporate governance structure.

- •Compromised Delisting Appeal: The company’s appeal against delisting relies on demonstrating stability and a clear path forward. This event directly contradicts that narrative, potentially giving regulators more reason to uphold the delisting decision.

- •Barriers to Fundraising: Any hope of raising capital to shore up finances is now virtually non-existent. No credible lender or investor would engage with a company facing this level of management and legal risk.

An Investor’s Guide: What to Do About HYUNDAI FEED Inc. Stock

Given the confluence of extreme negative factors, investors must act with the utmost caution. The outlook for HYUNDAI FEED Inc. is overwhelmingly negative, and the risk of total capital loss is severe.

Immediate Recommendations:

- •Avoid New Investment: Initiating any new position in this stock would be pure speculation, not investment. The risks far outweigh any potential, improbable rebound.

- •Monitor Official News: For existing shareholders, the only course of action is to closely monitor the final verdict on the delisting appeal and any updates regarding the provisional seizure lawsuit.

- •Prepare for the Worst-Case Scenario: The most probable outcome is the confirmation of delisting. Investors should understand what this means for their holdings and consult with a financial advisor. You can learn more by reading our guide on How to Handle Delisted Stocks in Your Portfolio.

- •Understand the Legal Terms: For a broader understanding of the legal mechanism at play, authoritative sources like Investopedia offer detailed explanations of asset seizures.

This analysis is based on publicly available information. Investment decisions carry inherent risks and should be made based on your own judgment and consultation with professional advisors.