The semiconductor industry is buzzing as QUALITAS SEMICONDUCTOR CO., LTD., a leader in cutting-edge semiconductor Intellectual Property (IP), announces a monumental ₩1 billion IP license contract, marking its strategic entry into the European market. This deal is far more than a revenue boost; it serves as a powerful validation of the company’s advanced technology and lays a critical foundation for future global growth. But what does this mean for investors and the company’s long-term valuation?

This comprehensive analysis will dissect the contract’s details, explore the strategic implications for the Qualitas Semiconductor stock, and weigh the promising outlook against the company’s current financial challenges to provide a balanced perspective for informed investment decisions.

The European Breakthrough: Deconstructing the ₩1 Billion Deal

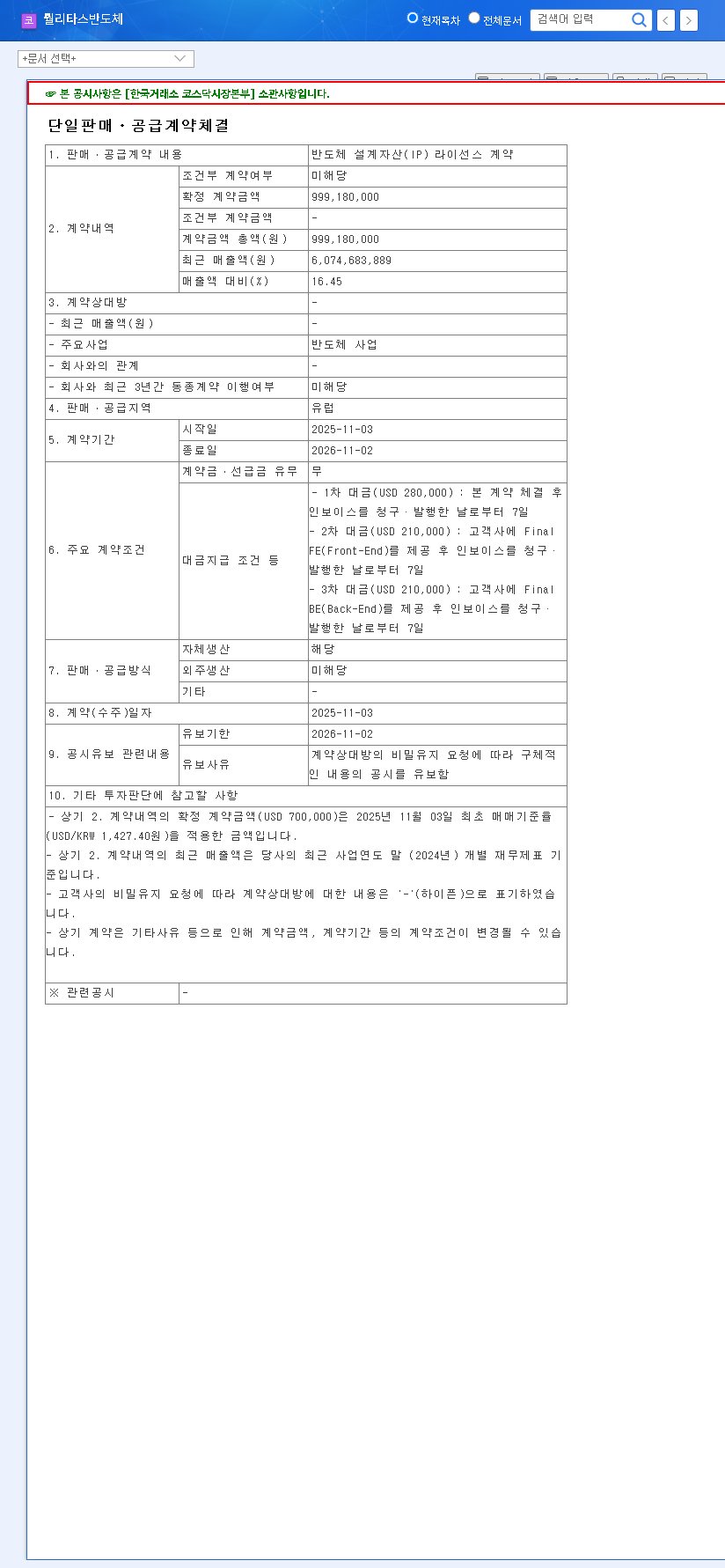

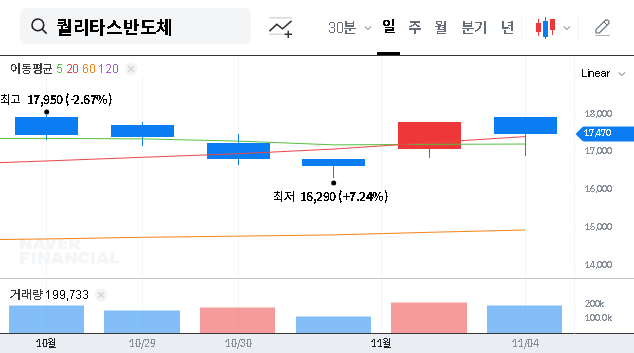

On November 4, 2025, QUALITAS SEMICONDUCTOR formally announced a significant semiconductor IP license contract valued at ₩1 billion (approximately $750,000 USD) with an as-yet-undisclosed company in Europe. According to the Official Disclosure, the agreement is valid for one year, from November 3, 2025, to November 2, 2026. The magnitude of this single contract cannot be overstated, representing approximately 35.8% of the company’s entire revenue from the first half of 2025.

Key Contract Details:

- •Contract Type: Single Sale/Supply Contract (Semiconductor IP License)

- •Contract Value: ₩1,000,000,000 KRW

- •Supply Region: Europe

- •Contract Period: Nov 3, 2025 – Nov 2, 2026

Core Technology & Strategic Impact

This deal is a victory for QUALITAS SEMICONDUCTOR’s technological prowess. The company specializes in high-speed interconnect IP licensing, which is the critical technology that allows different components within a chip or system to communicate at lightning-fast speeds. This is the digital backbone for high-growth industries like Artificial Intelligence (AI), High-Performance Computing (HPC), and data centers. Their portfolio, featuring standards like MIPI, PCIe, and the emerging Universal Chiplet Interconnect Express (UCIe), positions them at the forefront of innovation.

Securing a major IP license agreement in the competitive European market is a clear validation of a company’s technology. It signals to investors that the R&D investment is translating into commercially viable and globally recognized products.

Why the European Market Matters

Entering the European semiconductor market is a strategic masterstroke. Beyond simple revenue diversification, it opens doors to the region’s massive automotive, industrial, and telecommunications sectors, all of which are undergoing rapid digital transformation. This foothold serves as a launchpad for future IP sales and design service opportunities, reducing the company’s reliance on a concentrated client base.

The Investor’s Dilemma: Growth vs. Profitability

Despite the celebratory news, a prudent investor must examine the full financial picture. As of H1 2025, QUALITAS SEMICONDUCTOR reported revenue of ₩2.795 billion but posted an operating loss of ₩11.415 billion. This persistent deficit is largely driven by an aggressive R&D expenditure, which sits at a staggering 421.40% of revenue. While this heavy investment is crucial for maintaining a technological edge in the fast-evolving semiconductor space, it creates a significant drag on short-term profitability.

A single ₩1 billion contract, while significant, is not a silver bullet for these accumulated losses. The path to profitability will require a series of such wins. Investors should also be mindful of macroeconomic headwinds, such as the global semiconductor market’s recovery pace and currency fluctuations, which are explored in reports from authorities like the Semiconductor Industry Association (SIA).

Frequently Asked Questions (FAQ)

What does QUALITAS SEMICONDUCTOR specialize in?

QUALITAS SEMICONDUCTOR is a specialized semiconductor Intellectual Property (IP) company. They design and license high-speed interconnect technology (e.g., MIPI, PCIe, UCIe) that enables rapid data transfer in advanced electronics for AI, HPC, and automotive applications.

How significant is this new European contract?

The ₩1 billion IP license contract is highly significant. It represents about 35.8% of the company’s revenue from the first half of 2025, provides a crucial entry into the strategic European market, and validates the commercial appeal of its technology on a global stage.

What are the main risks for Qualitas Semiconductor stock investors?

The primary risk is the company’s current lack of profitability due to high R&D spending. While this new contract is a positive step, sustained revenue growth from multiple new contracts is needed to overcome the operating losses. Investors should monitor the company’s ability to convert its technological lead into consistent financial performance.

What should investors watch for next?

Key monitoring points include:

- •Disclosure of the European partner’s identity and potential for follow-on deals.

- •The pace of securing additional contracts in Europe and other new markets.

- •Quarterly financial reports showing a clear trend towards profitability.

- •Progress on turning its R&D investment into tangible, profitable revenue streams.