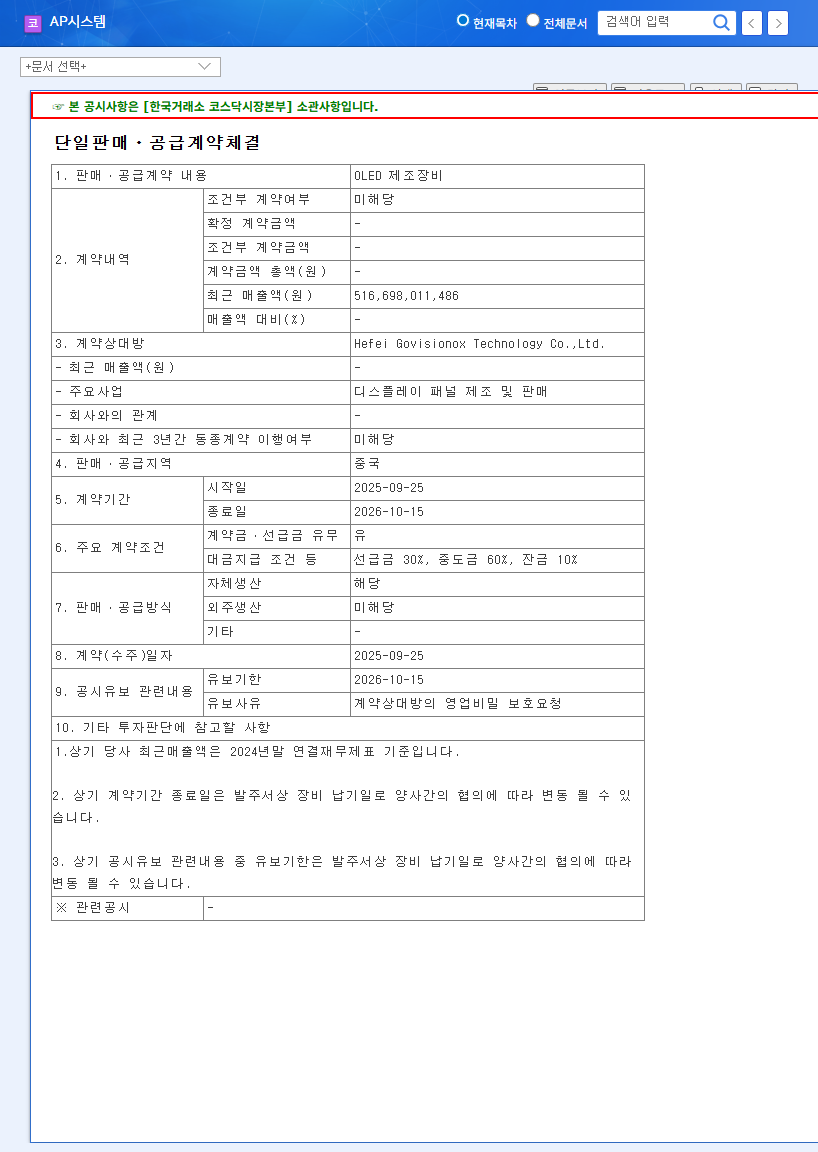

1. What Happened? AP Systems Signs OLED Equipment Supply Contract with Govisionox

AP Systems signed an OLED manufacturing equipment supply contract with China’s Hefei Govisionox Technology on September 25, 2025. The contract period is one year, from September 25, 2025, to October 15, 2026. This contract is part of AP Systems’ strategy to expand into the Chinese market and is expected to contribute to future sales growth.

2. Why Is It Important? Expansion into Chinese Market and Growth Momentum for OLED Business

This contract is expected to have several positive impacts on AP Systems. First, it secures a new customer in the Chinese market, expanding the company’s business scope and securing future growth drivers. Second, the consistent signing of contracts in the existing core business of OLED equipment demonstrates the company’s technological prowess and market competitiveness. Third, these positive factors are likely to be well-received by investors, potentially providing upward momentum for the stock price. In particular, as AP Systems focuses on securing future growth engines such as the development of HBM-related laser equipment, this contract can further accelerate its growth.

3. So What? Coexistence of Positive Impacts and Potential Risk Factors

However, there are also some uncertainties. The undisclosed contract amount makes it difficult to accurately predict the impact of this contract on AP Systems’ performance. Also, the impact of external factors such as geopolitical risks and US-China trade conflicts stemming from increased dependence on the Chinese market needs to be considered.

4. What Should Investors Do? Short-term/Mid-to-long-term Investment Strategies

In the short term, investors can expect upward momentum in the stock price due to the signing of the contract. However, it is important to make investment decisions after assessing the actual financial impact once the contract amount is disclosed.

In the mid-to-long term, it is necessary to comprehensively consider AP Systems’ potential growth in HBM-related new businesses, the growth trend of the OLED market, and efforts to diversify order sources. Attention should also be paid to changes in the external environment, such as global macroeconomic variables and exchange rate volatility.

What are AP Systems’ main businesses?

AP Systems operates OLED, semiconductor, and secondary battery equipment businesses. It maintains stable sales, especially in the OLED equipment sector, and is also focusing investment in HBM-related semiconductor equipment and secondary battery equipment businesses.

What kind of company is Hefei Govisionox Technology, the counterparty to this contract?

Hefei Govisionox Technology is a display manufacturer in China.

What is the impact of this contract on AP Systems’ stock price?

While it may provide upward momentum for the stock price in the short term, there are also uncertainties such as the undisclosed contract amount. The mid-to-long-term impact needs to be considered comprehensively, taking into account AP Systems’ fundamentals, market conditions, and external factors.