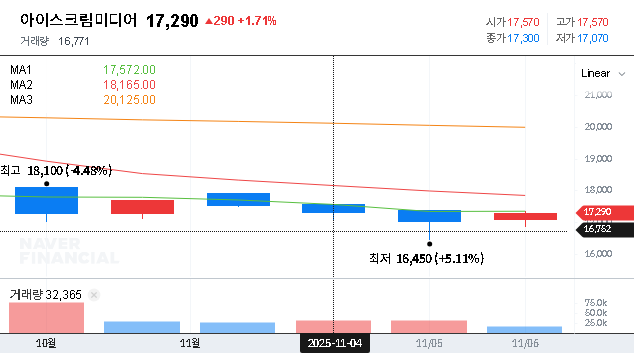

A recent move by i-Scream Media CO., LTD. has sent ripples through the investment community, prompting a critical question: is the company’s latest financial maneuver a red flag or a green light for growth? The announcement of a significant i-Scream Media self-stock disposal worth 12 billion KRW has created short-term uncertainty. However, a deeper analysis reveals this could be a strategic play to fuel its long-term ambitions in the competitive EdTech landscape.

This comprehensive i-Scream Media analysis unpacks the details of this decision, evaluates the company’s robust underlying fundamentals, and provides a clear roadmap for investors navigating the potential volatility to identify long-term opportunity.

The Core Event: Understanding the Self-Stock Disposal

On November 6, 2025, i-Scream Media disclosed its plan to dispose of 598,969 of its own shares, valued at approximately 12 billion KRW. This isn’t a simple stock sale. The company is using these treasury shares as the underlying asset to issue private placement Exchangeable Bonds (EB). In essence, they are raising capital by offering bonds that can be exchanged for company stock at a later date. To learn more about the mechanics of these financial instruments, you can refer to authoritative sources like Investopedia’s guide on Exchangeable Bonds. This strategic fundraising is poised to heavily influence the company’s investment capacity and future operational direction.

While the market often reacts nervously to potential share dilution, the true test is how the raised capital is deployed. For a financially sound, debt-free company like i-Scream Media, this is likely a calculated move to accelerate growth, not a measure of desperation.

Beyond the Headlines: A Look at i-Scream Media’s Rock-Solid Fundamentals

Despite the market’s short-term focus on the stock disposal, the company’s core business remains exceptionally strong. An analysis of its operations reveals a multi-faceted leader in the booming EdTech investment space.

Market Dominance Across Key Sectors

- •Education Publishing: With the 2022 revised curriculum driving textbook sales, the highly popular ‘i-Scream S’ platform ensures a high adoption rate among teachers, creating a cycle of stable, long-term revenue.

- •Commerce (i-Scream Mall): Holding a staggering 90% market share, the focus is now on improving profitability by expanding its private label products and enhancing its B2G services for educators.

- •Teacher Training: As the undisputed leader with a 36.5% market share, this segment provides stable income and is set to benefit from government policies expanding early childhood education.

Investing in Future Growth Engines

i-Scream Media is not resting on its laurels. The company is actively investing in next-generation technology to cement its leadership. This includes a major push into the AI Digital Textbook market, leveraging AI for personalized learning experiences. Furthermore, continuous R&D into LLMs, generative AI, and multimodal technologies—supported by collaborations with top universities like KAIST—ensures a strong competitive edge in the future of EdTech.

An Impeccable Financial Structure

Perhaps the most compelling fundamental is the company’s financial health. With current assets of 113.6 billion KRW and zero total borrowings, i-Scream Media boasts an incredibly low debt ratio and excellent soundness. This strong financial position means the 12 billion KRW fundraising isn’t a necessity for survival but rather an offensive move to capture more market share and innovate faster.

Investor Playbook: Navigating the i-Scream Media Stock

The i-Scream Media self-stock disposal introduces clear short-term risks, primarily the downward price pressure from an increased supply of shares and the potential for future share dilution when the bonds are exchanged. However, for the discerning investor, this volatility could present a buying opportunity.

Actionable Recommendations for Investors

- •Do Your Due Diligence: The first step is to review the primary source. The company’s filing provides critical details. You can view the Official Disclosure (DART report) here.

- •Focus on Fund Utilization: The key question is how the 12 billion KRW will be used. Watch for announcements regarding investments in AI development, new business acquisitions, or platform enhancements. Effective use of capital will be a powerful long-term catalyst.

- •Adopt a Long-Term Perspective: While short-term traders may react to price fluctuations, long-term investors should focus on the fundamentals. The company’s market leadership and debt-free status provide a significant margin of safety.

- •Monitor Market Consensus: Keep an eye on reports from securities firms and financial analysts. As more information about the fund’s deployment becomes available, the market sentiment may shift.

In conclusion, while the self-stock disposal creates near-term headwinds for the i-Scream Media stock price, it should be viewed through the lens of strategic investment. For a company with such a powerful market position and pristine balance sheet, this move is far more likely to be a stepping stone to its next phase of growth than a sign of trouble. Cautious, informed investors may find the current climate to be an attractive entry point.