Analyzing the Landmark ₩53.1 Billion HD-Hyundai Marine Engine Contract

In a significant development for the global shipbuilding industry, HD-Hyundai Marine Engine Co., Ltd. has secured a major shipbuilding engine supply contract valued at ₩53.1 billion. This pivotal agreement not only provides a substantial revenue injection but also solidifies the company’s position as a key player in the transition towards eco-friendly marine technology. This in-depth analysis will dissect the specifics of the HD-Hyundai Marine Engine contract, evaluate its impact on the company’s robust fundamentals, and explore the broader implications for the shipbuilding engine market and potential investors.

For anyone considering an HD-Hyundai Marine Engine investment, understanding the nuances of this deal is critical. It serves as a powerful indicator of the company’s growth trajectory, its alignment with stringent environmental regulations, and its synergistic strength within the wider HD-Hyundai Group.

Contract Breakdown: The Core Details

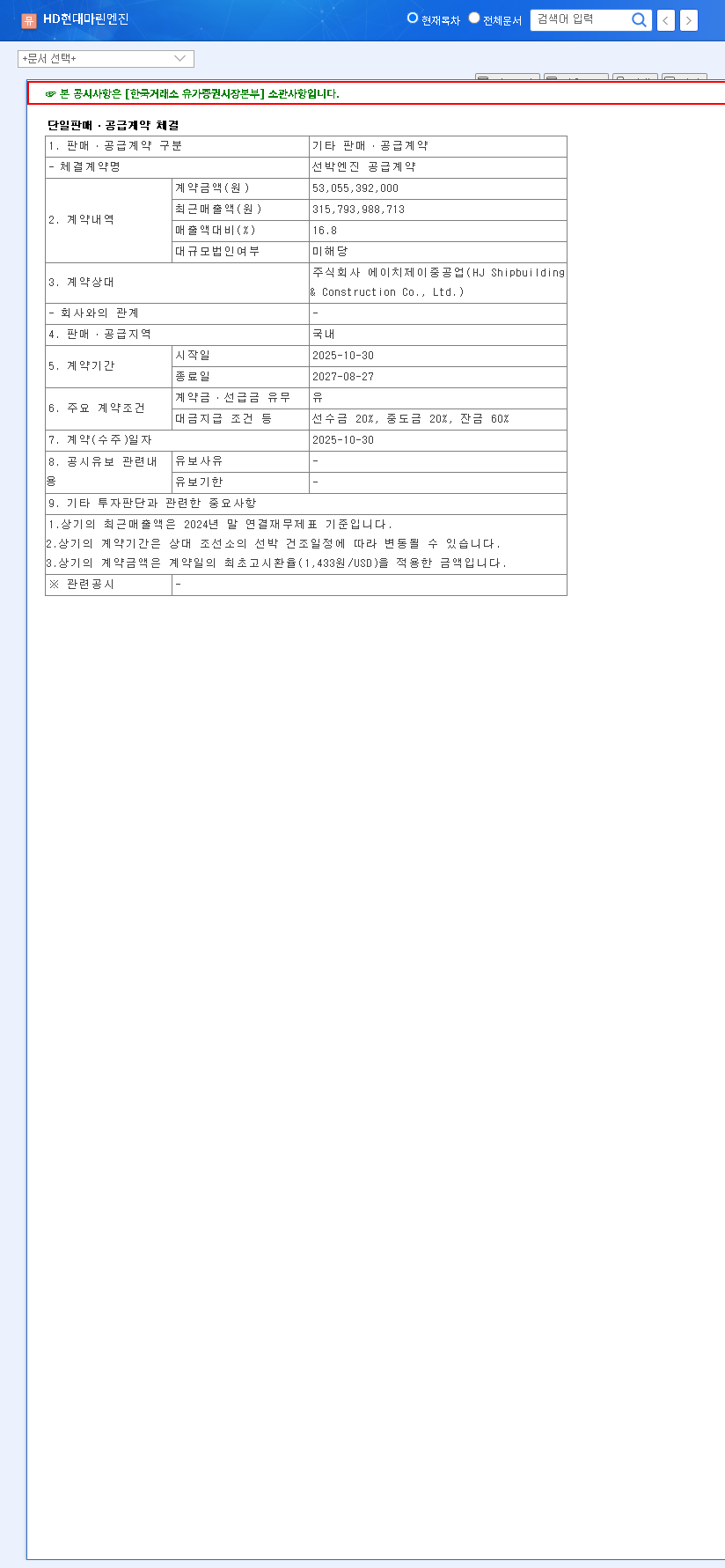

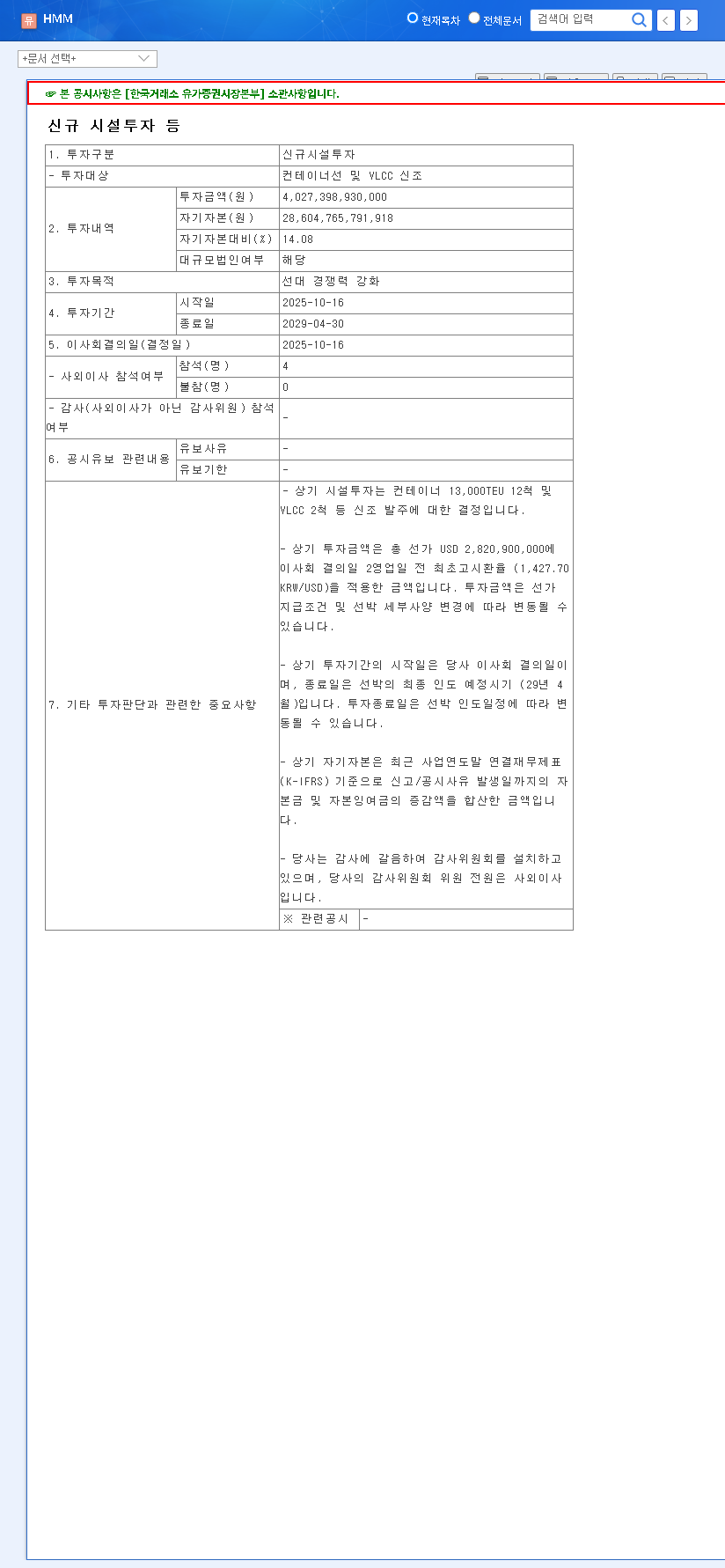

On October 31, 2025, HD-Hyundai Marine Engine Co., Ltd. officially signed the ₩53.1 billion engine supply contract with HJ Shipbuilding & Construction Co., Ltd. The agreement’s details, confirmed in an official disclosure (Source: DART), highlight its strategic importance. The contract value represents a significant 16.8% of the company’s revenue from the first half of 2025. Spanning a period of nearly two years, from October 30, 2025, to August 27, 2027, this deal ensures a stable and predictable revenue stream, bolstering the company’s financial foundation.

This long-term contract is more than just a number; it’s a testament to market confidence in HD-Hyundai’s technology and a crucial pillar for its mid-term financial stability and growth projections.

Why This Deal Matters: Fundamentals and Future Outlook

The timing of this contract aligns perfectly with HD-Hyundai Marine Engine’s strong performance and favorable market trends. The company’s fundamentals paint a picture of a healthy, growing enterprise poised to capitalize on industry shifts.

Robust Financial Health

The company’s financial performance in H1 2025 was exceptional, providing a strong base for this new contract. Key indicators include:

- •Impressive Growth: Revenue surged to ₩182.252 billion, a 24% year-on-year increase, driven by high demand for marine engines and crankshafts, especially in the Asian market.

- •Solid Profitability: A healthy Return on Equity (ROE) of approximately 8.5% and a manageable debt-to-equity ratio around 60% demonstrate financial stability.

- •Strong Cash Flow: Operating cash flow improved dramatically to ₩71.141 billion, a vital sign of operational efficiency in a capital-intensive industry.

Capitalizing on the Green Shipping Revolution

A primary driver of the positive outlook for the shipbuilding engine market is the global push for decarbonization. The International Maritime Organization (IMO) has set ambitious goals for reducing greenhouse gas emissions. These tightening regulations are forcing a fleet-wide transition to cleaner technologies, creating immense demand for eco-friendly marine engines. HD-Hyundai Marine Engine is perfectly positioned as a beneficiary of this trend, producing the advanced, dual-fuel engines that the market requires. You can learn more about these regulations directly from the official IMO website.

Market Impact and Strategic Investment Outlook

The ₩53.1 billion contract sends a clear, positive signal to the market and investors. It reinforces the company’s order-winning capabilities and strengthens its momentum. The partnership with HJ Shipbuilding & Construction also underscores the powerful synergy within the broader HD-Hyundai Group, a competitive advantage that can lead to more stable and integrated projects.

While macroeconomic factors like exchange rate volatility and fluctuating raw material prices remain potential risks, the company’s current trajectory is decidedly positive. A stronger US Dollar, for instance, has been shown to positively impact profit margins on its export-heavy business model. For investors looking for a deeper dive, consider reviewing our complete guide to investing in the shipbuilding industry.

Investor Action Plan & Key Takeaways

The HD-Hyundai Marine Engine contract is a fundamentally positive event that reinforces the company’s growth narrative. Investors should:

- •Recognize the direct contribution to revenue growth and long-term stability.

- •Appreciate the strengthened order momentum and enhanced market sentiment.

- •Monitor macroeconomic factors, particularly exchange rates and commodity prices.

- •Watch for future financial announcements and news of additional orders.

Frequently Asked Questions (FAQ)

Q1: What are the key details of the contract?

A1: HD-Hyundai Marine Engine signed a ₩53.1 billion engine supply contract with HJ Shipbuilding & Construction. This represents 16.8% of H1 2025 revenue and runs for approximately 1 year and 10 months, until August 2027.

Q2: How does this contract impact the company financially?

A2: It provides a direct boost to revenue and establishes a stable income base for nearly two years, enhancing financial predictability and supporting the company’s impressive growth trend.

Q3: What is the business outlook for HD-Hyundai Marine Engine?

A3: The outlook is highly positive. The increasing demand for eco-friendly marine engines, driven by IMO regulations, creates a favorable market. Synergy within the HD-Hyundai Group further strengthens its competitive position.