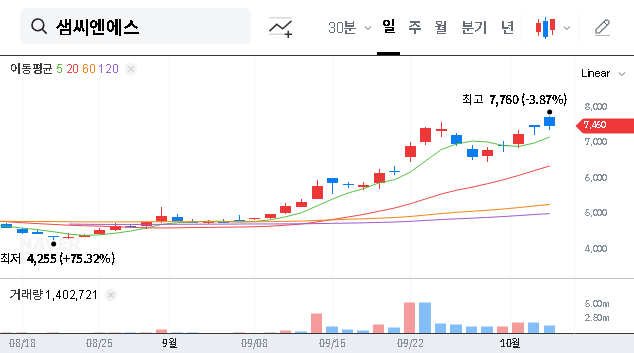

The latest T. K. CORPORATION earnings report for Q3 2025 has sent ripples through the market, revealing an astonishing performance that far outpaced analyst predictions. The company, also known as 태광, delivered what can only be described as a significant ‘earnings surprise’, headlined by a jaw-dropping 307.5% surge in net profit. This explosive growth raises critical questions for investors: What are the fundamental drivers behind this success, and is it a sustainable trend or a one-time event? This comprehensive analysis will break down the T. K. CORPORATION stock outlook, exploring the core financials, the impact of its secondary battery materials division, and the macroeconomic landscape to provide a clear investment thesis.

We will delve into the official numbers, compare them against market consensus, and assess the long-term viability of T. K. CORPORATION’s growth trajectory, offering actionable insights for your investment strategy.

Q3 2025 Earnings Analysis: Crushing Expectations

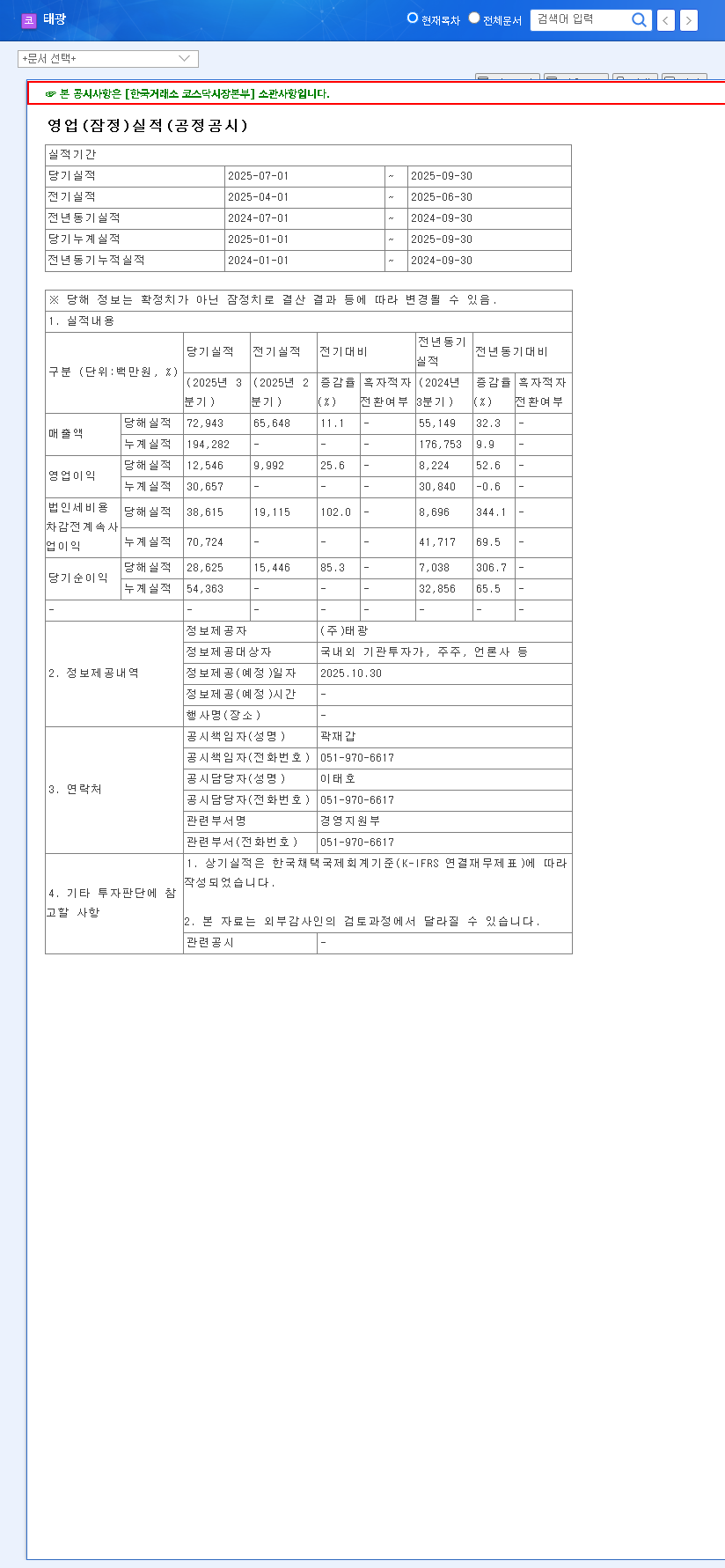

On October 30, 2025, T. K. CORPORATION released its preliminary Q3 operating results, which significantly exceeded market consensus as reported by major financial news outlets. The performance was strong across the board, but the net profit figure was the undeniable highlight. The data comes directly from the company’s Official Disclosure filed with DART.

The core of this earnings surprise was the net profit of 28.6 billion KRW, which demolished the market expectation of 9.3 billion KRW. This represents a 307.5% achievement rate, a staggering 207.5 percentage points above consensus.

Key Financial Metrics vs. Market Consensus:

- •Revenue: 72.9 billion KRW (Achieved 102.8% of the 70.9 billion KRW expectation).

- •Operating Profit: 12.5 billion KRW (Achieved 109.6% of the 11.4 billion KRW expectation).

- •Net Profit: 28.6 billion KRW (Achieved an incredible 307.5% of the 9.3 billion KRW expectation).

What’s Fueling the Growth Engine?

This exceptional performance isn’t accidental. It’s a combination of solid fundamentals in core businesses and potentially significant one-off financial events that boosted the bottom line.

The Power of Secondary Battery Materials

T. K. CORPORATION operates in two primary segments: plant equipment and secondary battery materials. While plant equipment provides a stable foundation, the secondary battery division is the company’s star growth engine. Amid the global transition to electric vehicles (EVs), demand for high-quality battery components has skyrocketed. T. K. CORPORATION’s strategic position within this supply chain is a critical pillar supporting its revenue growth and a key factor for anyone evaluating T. K. CORPORATION stock for the long term. This segment is a key part of the broader, rapidly expanding renewable energy technology sector.

The Mystery of the Net Profit Surge

The fact that net profit was more than double the operating profit strongly suggests the influence of non-operating income. The most likely culprits are one-off gains, such as the sale of an asset, or significant foreign exchange (FX) gains from a weakening Korean Won. While this is fantastic for the Q3 report, investors must determine if this is repeatable before projecting similar results into the future.

Navigating the Macroeconomic Tides

No company operates in a vacuum. The current global economic environment presents both tailwinds and headwinds for T. K. CORPORATION.

- •Favorable Factors: The downward trend in key commodity prices (crude oil, industrial metals) and logistics costs (Baltic and China Container Freight Indexes) is a major positive. This directly reduces T. K. CORPORATION’s cost of goods sold and shipping expenses, thereby boosting profit margins.

- •Unfavorable Factors: Rising interest rates, particularly in the U.S., increase the cost of capital and can raise the financial burden from corporate debt. Furthermore, while a weak KRW can lead to FX gains on foreign-denominated assets, sustained volatility creates uncertainty for financial planning.

Investment Outlook: Risks vs. Opportunities

The blockbuster T. K. CORPORATION earnings for Q3 will likely provide a strong short-term catalyst for the stock. However, a prudent investor must weigh the long-term prospects.

Short-Term Opportunities & Risks

Opportunity: The powerful earnings surprise is expected to attract positive investor sentiment and could drive short-term momentum in the stock price as the market digests the news.

Risk: The primary risk is that the market overreacts to a one-off gain. If the net profit surge is not from sustainable operational improvements, future earnings reports may seem disappointing in comparison, potentially leading to a correction.

Long-Term Growth & Headwinds

Growth Driver: The long-term investment appeal is anchored in the immense growth potential of the secondary battery materials business. As the world electrifies, T. K. CORPORATION is well-positioned to capitalize on this multi-decade trend.

Headwind: Persistent macroeconomic uncertainty (interest rates, FX volatility) and intensifying competition in the battery market are notable risks. The company’s ability to innovate and maintain its competitive edge will be crucial for sustained growth.

Actionable Investor Checklist

For those considering an investment in T. K. CORPORATION, a disciplined approach is essential. Here are three key steps:

- •Verify the Source of Profit: Scrutinize subsequent company announcements and conference calls to identify the exact cause of the net profit surge. Differentiating between operational excellence and one-off gains is paramount.

- •Monitor Macro Trends: Keep a close watch on exchange rates, interest rates, and commodity prices. Understand how T. K. CORPORATION is using strategies like hedging to mitigate these external risks.

- •Evaluate Competitive Positioning: Analyze the company’s R&D pipeline, market share, and strategic partnerships within the secondary battery sector. Long-term success depends on staying ahead of the technological curve.

In conclusion, while the Q3 T. K. CORPORATION earnings report is overwhelmingly positive, its long-term value hinges on the sustainability of its core business growth, particularly in the dynamic secondary battery market.