The NAVER Corporation Q3 2025 earnings report has sent a significant positive signal to the market, reaffirming the tech giant’s robust growth trajectory. Investors and analysts were taken by surprise as the company announced a staggering 46% beat on net profit estimates, a figure that speaks volumes about its operational efficiency and strategic initiatives. This comprehensive analysis will dissect the official NAVER earnings report, explore the performance of its diverse business segments, evaluate its financial health amidst a challenging macroeconomic landscape, and provide critical insights for anyone following NAVER stock.

From its AI-powered search platform to its expanding global content empire, NAVER’s performance this quarter offers a compelling glimpse into its future. Let’s explore the key drivers behind these exceptional results.

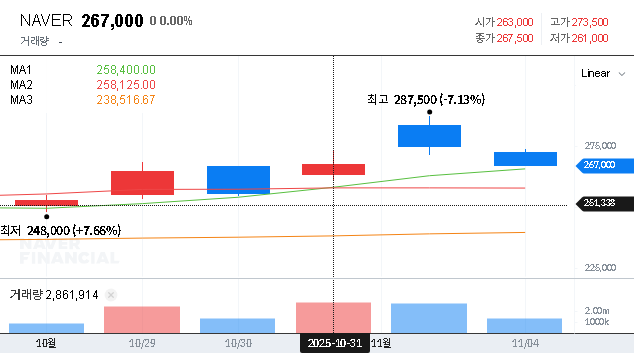

📈 The Stunning Q3 2025 Financials: A Deeper Look

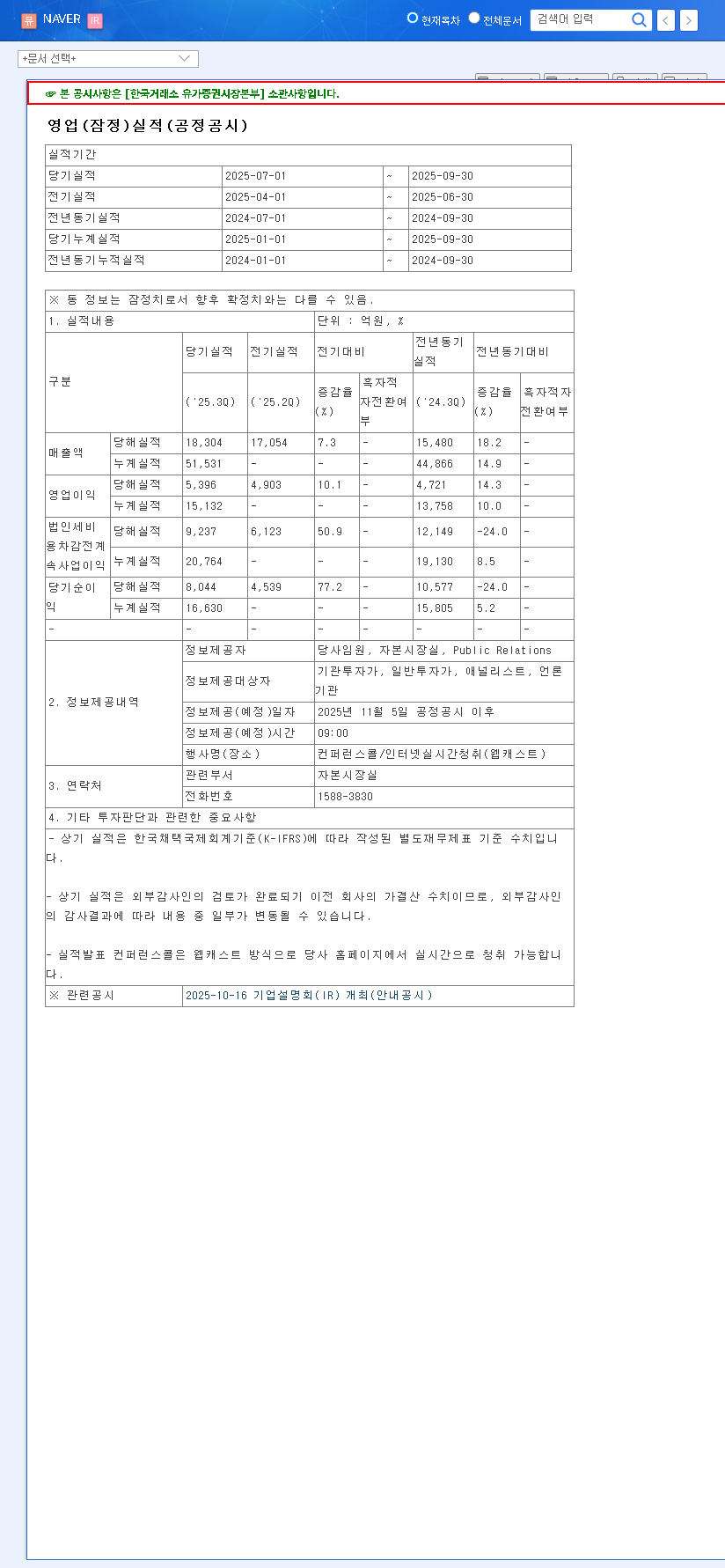

On November 5, 2025, NAVER unveiled its preliminary consolidated results, decisively outperforming market consensus in key areas. The highlight was not just meeting but soundly beating profit expectations. The full details can be reviewed in the company’s Official Disclosure filed with DART.

- •Revenue: KRW 3,138.1 billion, a solid 3% above the market estimate of KRW 3,048.6 billion.

- •Operating Income: KRW 570.6 billion, perfectly aligned with the market estimate of KRW 568.7 billion.

- •Net Profit: KRW 726.4 billion, an incredible 46% above the market estimate of KRW 496.5 billion.

Such a significant net profit surprise indicates powerful underlying factors at play, such as highly effective cost optimization, unexpected non-operating revenue streams, or the early fruition of strategic investments. This result is a key factor in the current positive sentiment surrounding NAVER’s stock analysis.

Core Business Segments: The Engine of Growth

NAVER’s strength lies in the balanced and synergistic growth across its primary business divisions. Each segment contributed to the impressive Q3 2025 results.

Search & AI Platform

The foundational search platform remains a pillar of stability. Growth is consistently driven by the integration of advanced AI, enhancing advertising efficiency and user search experience. While concerns about a general slowdown in the online ad market persist, NAVER’s technological edge continues to provide a defensive moat.

Commerce

In a fiercely competitive e-commerce landscape, especially with the rise of Chinese platforms, NAVER has fortified its position. By enhancing its membership benefits and leveraging specialized platforms like the C2C marketplace Poshmark and sneaker reseller KREAM, it has cultivated a loyal user base. This focus on user experience and niche markets is key to its resilience.

FinTech

Naver Pay continues to expand its footprint, moving beyond simple online payments to a comprehensive suite of financial services. This expansion provides a powerful growth engine, though it requires proactive navigation of an evolving regulatory environment in South Korea.

Content & Webtoons

The global webtoon business is a standout performer. By strengthening its intellectual property (IP) value chain—turning popular webtoons into dramas, films, and merchandise—NAVER is creating diverse and high-margin revenue streams. This global content strategy is a critical component of its long-term growth narrative.

NAVER’s strategy of aggressive yet calculated investment is paying dividends. The Q3 2025 earnings show a company that is not just expanding but is doing so efficiently, converting top-line growth into impressive bottom-line results.

Navigating Macroeconomic Realities

As a global player, NAVER’s performance is intrinsically linked to the wider economic environment. High exchange rates can be a double-edged sword, potentially boosting the value of overseas earnings when converted to KRW but also increasing the cost of foreign investments. Similarly, elevated interest rates, as noted by sources like Reuters, increase borrowing costs. However, NAVER’s robust financial structure and strong cash generation from operations provide a substantial buffer against these pressures, allowing it to continue its strategic investments.

Investor Outlook: Bullish Signals & Risks

The NAVER Corporation Q3 2025 earnings paint a bright picture, but a balanced view is essential for investors.

Positive Factors to Watch

- •AI Integration: Continued monetization of AI across its business portfolio.

- •Global Content Growth: The Webtoon IP value chain continues to show immense potential.

- •Earnings Surprise: The 46% net profit beat provides strong momentum and boosts investor confidence.

Risk Factors to Monitor

- •Competition: Intense pressure in e-commerce and search from both domestic and international rivals.

- •Economic Volatility: Global economic slowdowns and exchange rate fluctuations remain a threat.

- •Investment ROI: Ensuring that large-scale investments in AI and new ventures deliver tangible financial results.

In conclusion, NAVER’s Q3 performance demonstrates a company firing on all cylinders. Its ability to innovate, manage costs, and execute its global strategy confirms its position as a formidable player in the tech industry. Investors should continue to monitor these key factors, as NAVER builds on its diverse and powerful growth story.