The latest CJ ENM earnings announcement for Q3 2025 presented a complex picture for investors. On one hand, a dazzling net profit figure far surpassed expectations, creating a wave of initial optimism. However, lurking beneath this headline number was a concerning miss in operating profit, raising critical questions about the health of the company’s core businesses. This deep-dive analysis unpacks the preliminary 035760 earnings report, dissecting the conflicting signals to provide a clear outlook on what’s next for the South Korean entertainment giant.

We will explore the fundamental drivers behind these results, from segment-specific performance to macroeconomic headwinds, to provide a comprehensive CJ ENM stock analysis. Let’s uncover the true narrative behind the numbers and what it means for your investment strategy.

CJ ENM Q3 2025 Earnings: The Headline Figures

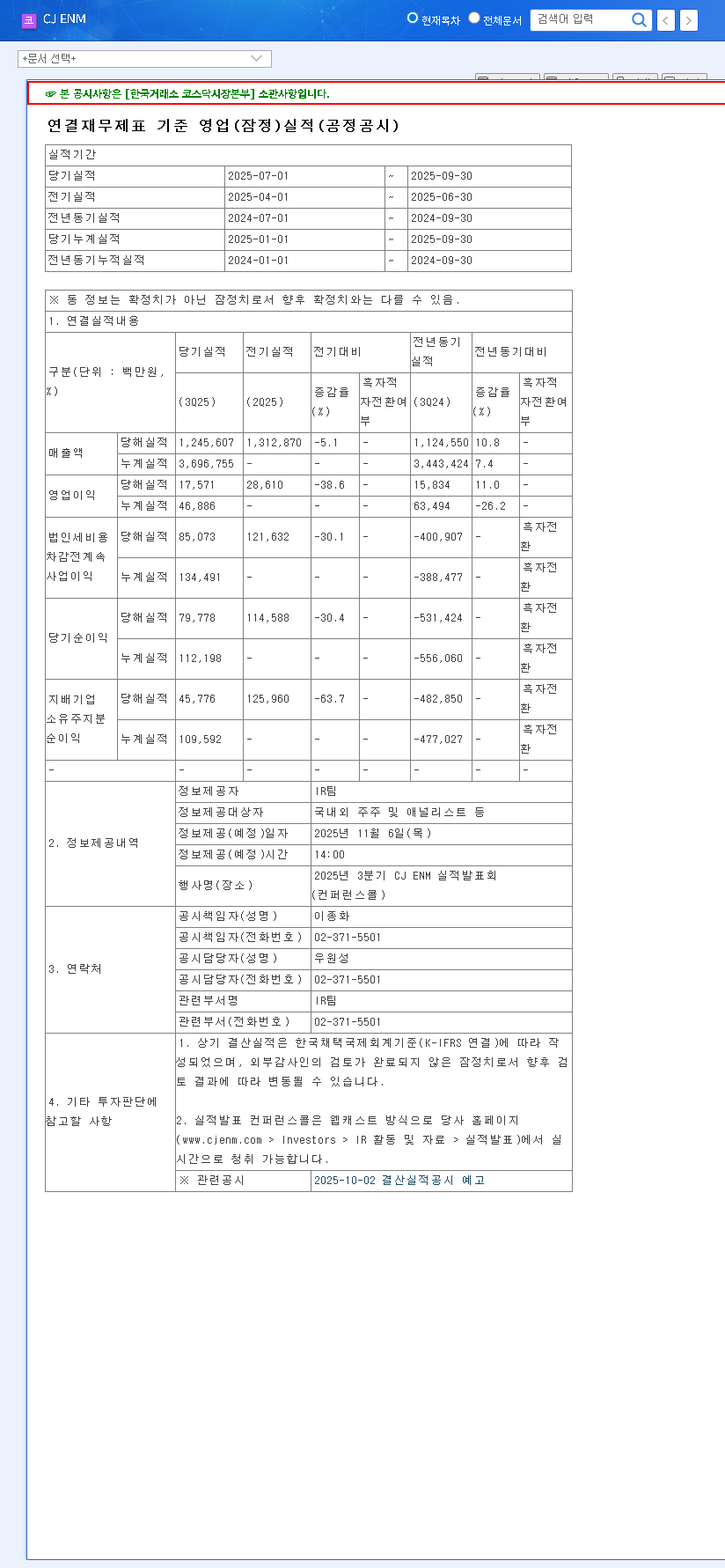

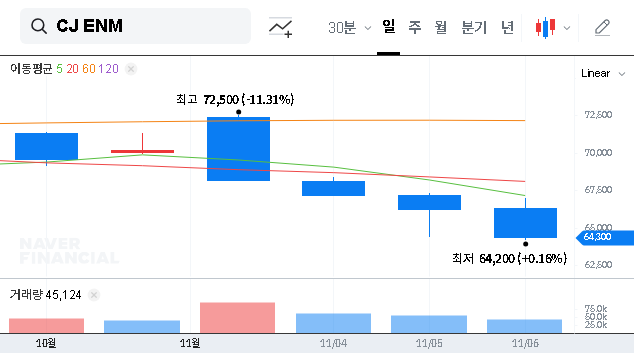

CJ ENM CO., Ltd. (035760) released its Q3 2025 preliminary consolidated financial statements, revealing a stark contrast between its operational performance and bottom line. The market’s reaction has been mixed, reflecting the dual nature of the report. The complete data can be reviewed in the company’s Official Disclosure on DART.

- •Revenue: KRW 1,245.6 billion. This figure was perfectly in line with market consensus, showing a 0% variance from estimates.

- •Operating Profit: KRW 17.6 billion. A significant disappointment, falling short of expectations by a staggering 34% and signaling trouble in core operations.

- •Net Profit: KRW 45.8 billion. The highlight of the report, delivering a massive earnings surprise by exceeding estimates by over 690%.

The core issue for investors is clear: Is the net profit surprise a sustainable sign of recovery, or a one-time event masking a deteriorating CJ ENM operating profit margin?

Why Did It Happen? A Deeper Analysis

To understand the future, we must dissect the past. The divergence in profit metrics stems from different parts of the business pulling in opposite directions. The poor CJ ENM operating profit performance points to persistent challenges within its primary business segments.

The Pressure on Core Operations

The operating profit miss appears to be a continuation of trends seen earlier in the year. The primary culprits are the Media Platform and Film & Drama divisions. The Media Platform continues to grapple with a sluggish global advertising market, a trend affecting media companies worldwide (Source: Bloomberg). Even with growth from its streaming service, TVING, the decline in high-margin ad revenue has proven difficult to offset. Concurrently, the Film & Drama segment, despite producing global hits, is contending with soaring production costs and marketing expenses, which compress profit margins even on successful projects.

The Truth Behind the Net Profit Surprise

The exceptional net profit figure is highly likely attributable to non-operating, one-off events. This could include gains from the sale of assets, foreign exchange gains, or other forms of financial income that are not related to the company’s day-to-day business. While beneficial for the quarterly bottom line, these gains do not reflect a fundamental improvement in profitability or operational efficiency. Therefore, investors should view this ‘surprise’ with caution, as it is not indicative of a sustainable trend.

What’s Next? Financial Health & CJ ENM Stock Outlook

Looking ahead, the focus must shift to the company’s financial stability and its strategy for a turnaround. The current financial indicators from the CJ ENM Q3 2025 report suggest several areas of concern. The company’s debt-to-equity ratio remains elevated at over 138%, imposing a significant financial burden through interest payments. Furthermore, key profitability metrics like Return on Equity (ROE) have been weak, signaling that the company is struggling to generate adequate returns for its shareholders.

For a more detailed perspective on how CJ ENM fits into the market, you can read our broader analysis of the Korean media industry landscape. The path forward for CJ ENM requires a clear and decisive strategy to address these foundational issues.

Investor Action Plan & Recommendations

Sustainable growth will hinge on successful execution in several key areas:

- •Profitability Over Growth: A strategic pivot from pure revenue growth to establishing a stable profit structure in the Film & Drama segment is crucial. This means tighter budget controls and a more selective content investment strategy.

- •Media Platform Reinvention: The company must accelerate its efforts to monetize its digital platforms beyond advertising, perhaps through innovative subscription tiers or strategic partnerships for TVING.

- •Financial Discipline: Addressing the high debt-to-equity ratio through improved capital efficiency and potential debt restructuring should be a top priority to improve financial health.

Overall Opinion: The Q3 2025 CJ ENM earnings report warrants a conservative approach. While a short-term stock price bounce on the net profit news is possible, the underlying weakness in operating profit cannot be ignored. Until the company demonstrates a tangible turnaround in its core business profitability and financial health, the stock’s long-term upward momentum will likely remain constrained.