In a challenging global market, WONIK IPS CO., LTD. has delivered a remarkable performance in its preliminary Q3 2025 earnings report, creating a significant buzz within the investment community. The semiconductor equipment manufacturer didn’t just meet expectations; it shattered them, particularly with a substantial ‘earnings surprise’ in net income. This report has solidified investor confidence and highlighted the company’s resilient growth trajectory.

This in-depth WONIK IPS investment analysis will dissect the key figures from the Q3 2025 report, explore the fundamental drivers behind this success, evaluate potential risks, and provide a clear outlook for investors considering WONIK IPS stock.

Deconstructing the Q3 2025 Earnings Surprise

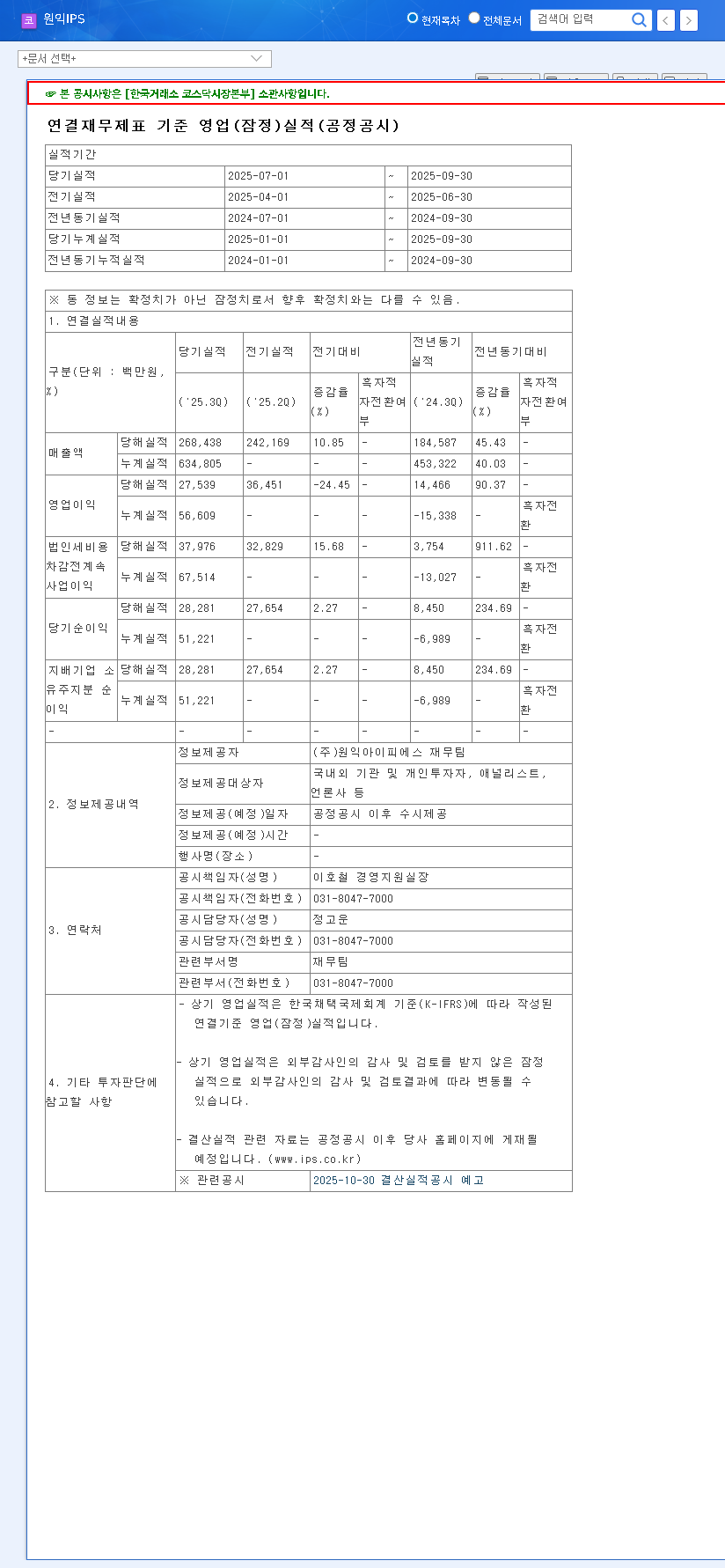

The preliminary results, announced on November 7, 2025, painted a picture of robust health and operational excellence. The figures, sourced from the company’s Official Disclosure, reveal a company firing on all cylinders.

- •Revenue: KRW 268.4 billion, a solid 6.9% above the consensus estimate of KRW 251.0 billion.

- •Operating Profit: KRW 27.5 billion, beating the estimated KRW 26.3 billion by 4.6%.

- •Net Income: KRW 28.3 billion, a staggering 47.4% above the market’s expectation of KRW 19.2 billion.

While top-line revenue growth is impressive, the dramatic outperformance in net income is the key takeaway. It signals exceptional cost management, high-margin product sales, and a powerful profit generation engine at WONIK IPS.

Core Strengths: The Pillars of Growth for WONIK IPS

This stellar quarter isn’t a fluke. It’s built upon a foundation of strong fundamentals and strategic positioning within a dynamic market. The broader semiconductor industry continues to see tailwinds from AI and Big Data, a trend analyzed by major outlets like Bloomberg.

Strategic R&D and Technological Leadership

With an R&D expense ratio of nearly 21% of revenue (as of H1 2025), WONIK IPS demonstrates an aggressive commitment to innovation. This investment is crucial for developing next-generation deposition and etching technologies required for advanced 3D NAND, DRAM, and foundry processes. This focus on technology ensures the company remains a preferred supplier for major chipmakers.

Diversified Revenue Streams

The company’s revenue growth is directly tied to expanded capital expenditures in both the semiconductor and display markets. The increasing demand for OLED panels in smartphones, TVs, and automotive displays provides a complementary and robust revenue stream, mitigating some of the cyclicality inherent in the semiconductor sector alone.

Impeccable Financial Health

A low debt-to-equity ratio of just 38.02% provides significant operational flexibility and reduces financial risk for investors. This strong balance sheet allows WONIK IPS to navigate economic downturns and fund its ambitious R&D agenda without being overly reliant on debt financing.

Investor Alert: Potential Risks and Considerations

Despite the overwhelmingly positive WONIK IPS earnings report, prudent investors must remain aware of potential headwinds.

- •Factory Utilization Rates: Persistently low utilization rates (19% for semiconductor, 15% for display in H1) are a point of concern. While these numbers can be lumpy, they indicate a need for a more consistent flow of large-scale orders to improve production efficiency and absorb fixed costs.

- •Macroeconomic Volatility: The semiconductor industry is sensitive to global economic health. Geopolitical tensions, trade disputes, or a broad economic slowdown could dampen capital spending from chipmakers, impacting the order book for WONIK IPS.

- •Currency and Interest Rate Fluctuations: With a high dependency on exports, the company’s profitability can be affected by adverse movements in foreign exchange rates and rising global interest rates.

Final Verdict: Investment Outlook for WONIK IPS Stock

The Q3 2025 results serve as powerful validation of the company’s strategy and operational capabilities. The massive beat on net income, coupled with a solid growth foundation and a stable financial structure, paints a very bullish picture for the future of WONIK IPS.

Our investment outlook remains firmly Positive with a BUY recommendation. Investors should consider this a core holding within a technology-focused portfolio. For more information on this sector, you can read our Guide to Investing in Semiconductor Stocks. Moving forward, key metrics to monitor will be improvements in factory utilization and the size of the forward order book in the upcoming Q4 and subsequent reports.

Disclaimer: This analysis is for informational purposes only and is based on publicly available data. It does not constitute financial advice or a direct recommendation for any investment decision. All investment decisions should be made based on an individual’s own judgment and risk tolerance.