The latest SILICON 2 earnings report for Q3 2025 has sent a definitive signal to the market: the K-Beauty titan is not just growing, it’s accelerating. SILICON 2 Co.,Ltd. has once again demonstrated its formidable position in the global market by delivering an ‘earnings surprise’ that significantly outpaced analyst expectations. This performance raises critical questions for investors: What are the core drivers behind this sustained momentum? And what does this outstanding report mean for the future of SILICON 2’s stock valuation? This in-depth analysis will dissect the Q3 results, explore the company’s robust fundamentals, and provide a clear investment perspective.

A Stunning Q3 2025 ‘Earnings Surprise’

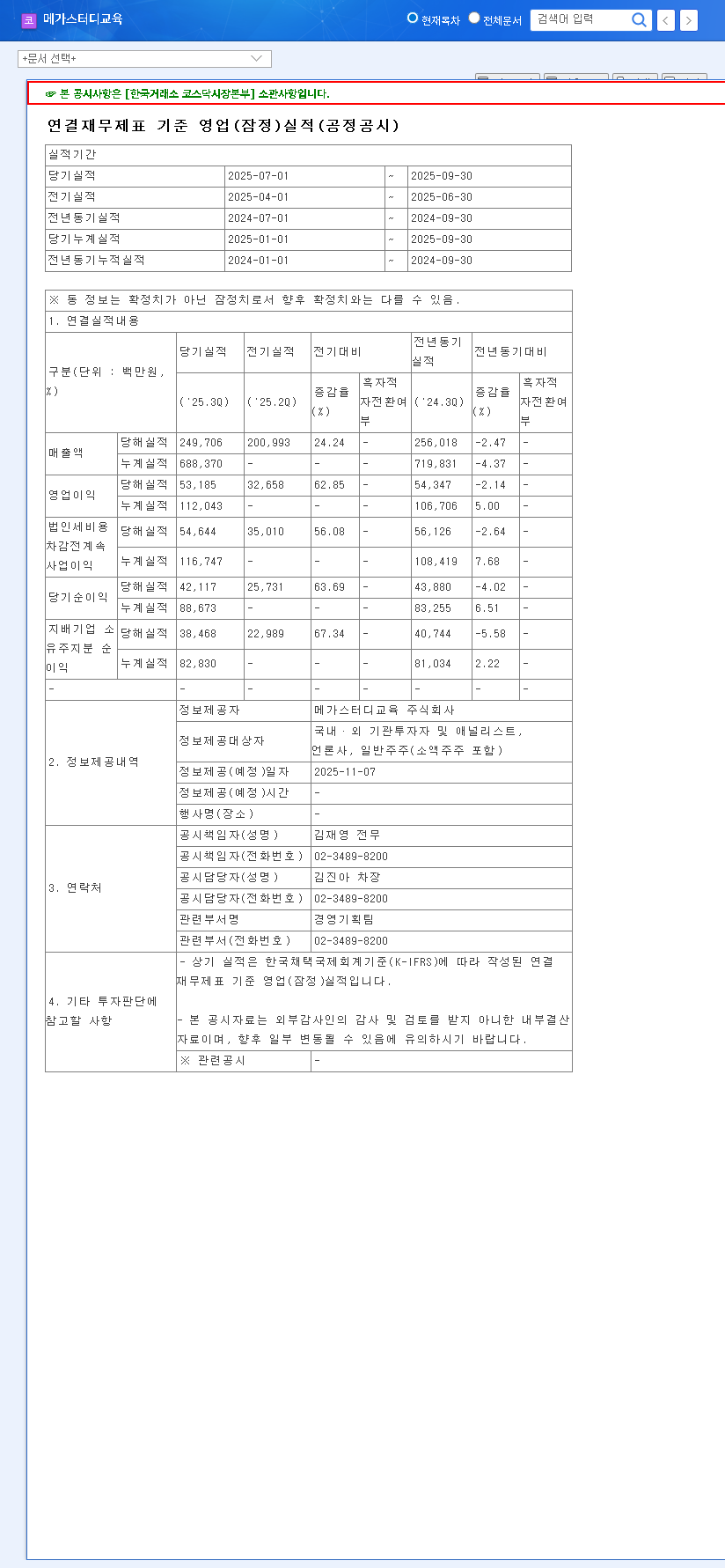

On November 10, 2025, SILICON 2 Co.,Ltd. unveiled its provisional Q3 results, creating a wave of optimism among investors. An earnings surprise occurs when a company’s reported profits are significantly different from Wall Street analysts’ consensus estimates. In this case, SILICON 2 didn’t just beat expectations; it shattered them, particularly in net income. The official data, available in the company’s Official Disclosure (Source: DART), highlights a company firing on all cylinders.

Here’s a breakdown of the impressive figures:

- •Revenue: KRW 299.4 billion, exceeding the estimate of KRW 293.9 billion by 2.0%.

- •Operating Profit: KRW 63.1 billion, a solid 5.0% above the KRW 60.0 billion forecast.

- •Net Income: KRW 58.4 billion, surging an astonishing 19.9% past the expected KRW 48.8 billion.

The nearly 20% beat on net income is a powerful indicator of enhanced profitability and efficient cost management. Furthermore, the quarter-over-quarter growth is remarkable: revenue climbed 12.8%, operating profit jumped 20.9%, and net income soared by 64.0% compared to Q2 2025, showcasing powerful growth momentum heading into the year’s end.

The Pillars of Success: Strong Fundamentals Driving Growth

This exceptional performance is not a fluke. It’s the result of a meticulously executed strategy built on solid fundamentals. The successful SILICON 2 earnings are a direct outcome of the company’s core strengths.

Unrivaled K-Beauty Global Distribution

As a premier e-commerce platform, SILICON 2 distributes K-Beauty products to over 160 countries. This vast network allows it to capitalize on the global demand for Korean cosmetics. The first half of 2025 saw exports accounting for 88.5% of total revenue, with the European Union being a major growth engine. This geographical diversification insulates the company from regional downturns.

Financial Fortitude and Strategic Investments

The company’s financial structure has significantly improved. A key highlight is its negative net debt of KRW 37.72 billion, meaning it holds more cash than debt—a powerful sign of financial health and operational efficiency. This strong balance sheet empowers SILICON 2 to invest in future growth, such as the KRW 10 billion injection into automated logistics systems (AGV), which will enhance efficiency, lower costs, and accelerate order fulfillment.

Expansion and Diversification Across K-Culture

SILICON 2 is intelligently expanding beyond cosmetics into the broader K-Culture phenomenon, adding business objectives in IT, management, and entertainment. This strategic pivot aims to create a synergistic ecosystem around the ‘Korean wave’. Furthermore, new subsidiaries in Dubai, Mexico, and Italy are set to unlock significant growth in the Middle East, Latin America, and European luxury markets, strengthening its global footprint.

SILICON 2 Stock Analysis: A Balanced View for Investors

The impressive earnings report undoubtedly paints a bullish picture, but a thorough SILICON 2 stock analysis requires examining both the opportunities and potential headwinds.

SILICON 2’s Q3 results confirm its status as a high-growth leader. The combination of market-beating performance, improving profitability, and strategic global expansion presents a compelling long-term investment case.

Potential Risk Factors to Monitor

- •Exchange Rate Volatility: With a high percentage of foreign-denominated assets, fluctuations in the KRW/USD exchange rate can significantly impact reported earnings and profitability.

- •Performance of Associates: The semi-annual report noted potential impairment losses from underperforming associate companies, which could pose a risk to overall financial health.

- •Market Competition: The global cosmetics market is fiercely competitive. For more insight, you can read our complete guide to investing in the K-Beauty market.

Investment Thesis & Recommendation

The Q3 2025 SILICON 2 earnings report is a significant positive catalyst. The company has proven its ability to execute effectively and deliver both top-line growth and bottom-line profitability. In the short term, positive stock price momentum is highly likely. In the long term, SILICON 2 is well-positioned to continue capitalizing on the global K-Culture trend.

Our recommendation is a cautious but optimistic ‘Buy’. Investors should consider initiating or adding to positions while remaining vigilant about the external risks, particularly exchange rate trends. Careful position management is advised to navigate potential volatility while capturing the company’s substantial long-term growth potential.

Disclaimer: This report is based on publicly available information. Investment decisions are the sole responsibility of the investor.