The story of SEERS TECHNOLOGY (458870) has become a focal point for investors, pitting staggering operational growth against a challenging stock performance. As the company prepares for a crucial Investor Relations (IR) event for domestic institutional investors, the market is buzzing with one question: can its explosive Q3 performance finally trigger a positive reversal for its stock? With revenue soaring by over 1,000% and a successful shift to operating profitability, the fundamentals appear robust. However, critical concerns loom. This comprehensive analysis dives into the company’s Q3 results, core growth drivers, the significant risks investors are monitoring, and a strategic outlook for SEERS TECHNOLOGY stock.

A Financial Turning Point: Deconstructing Q3’s Remarkable Performance

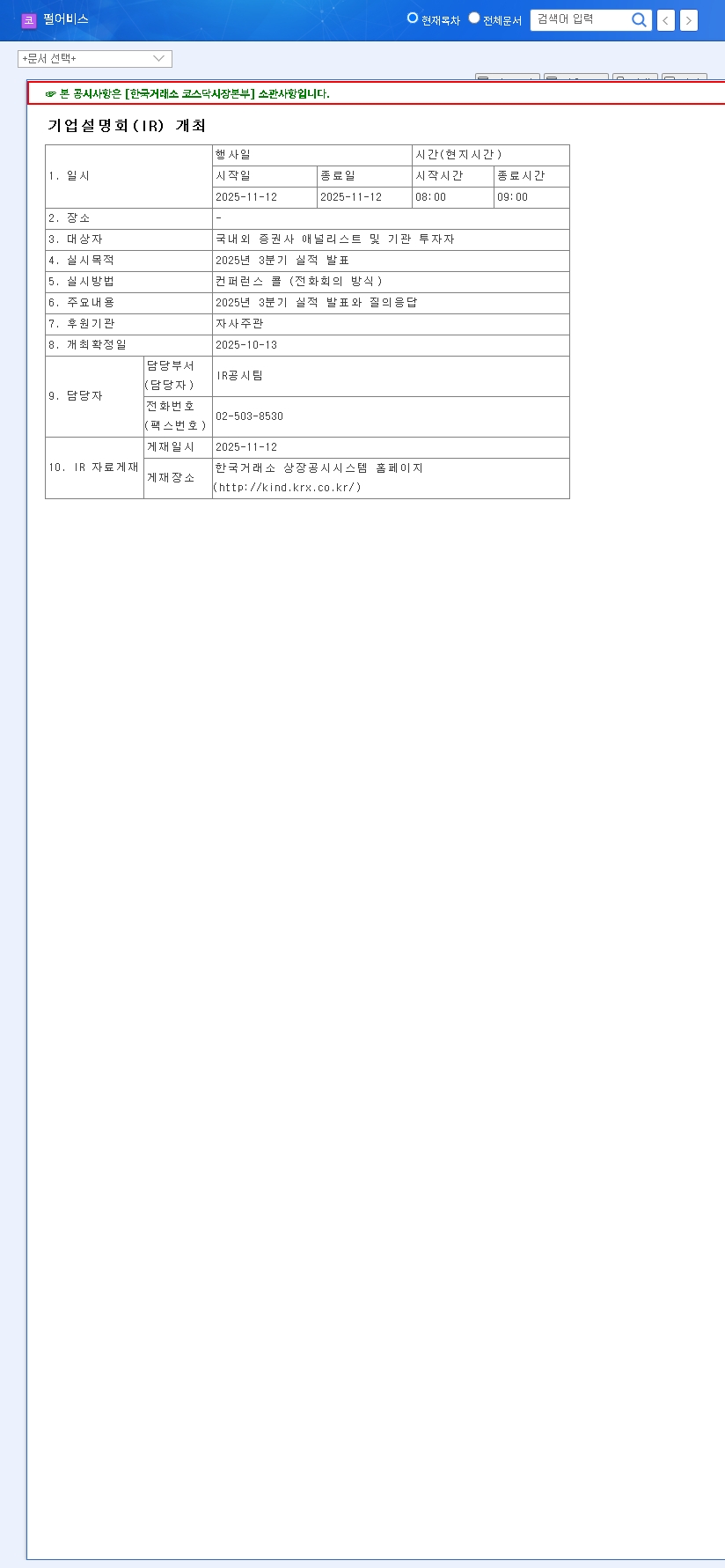

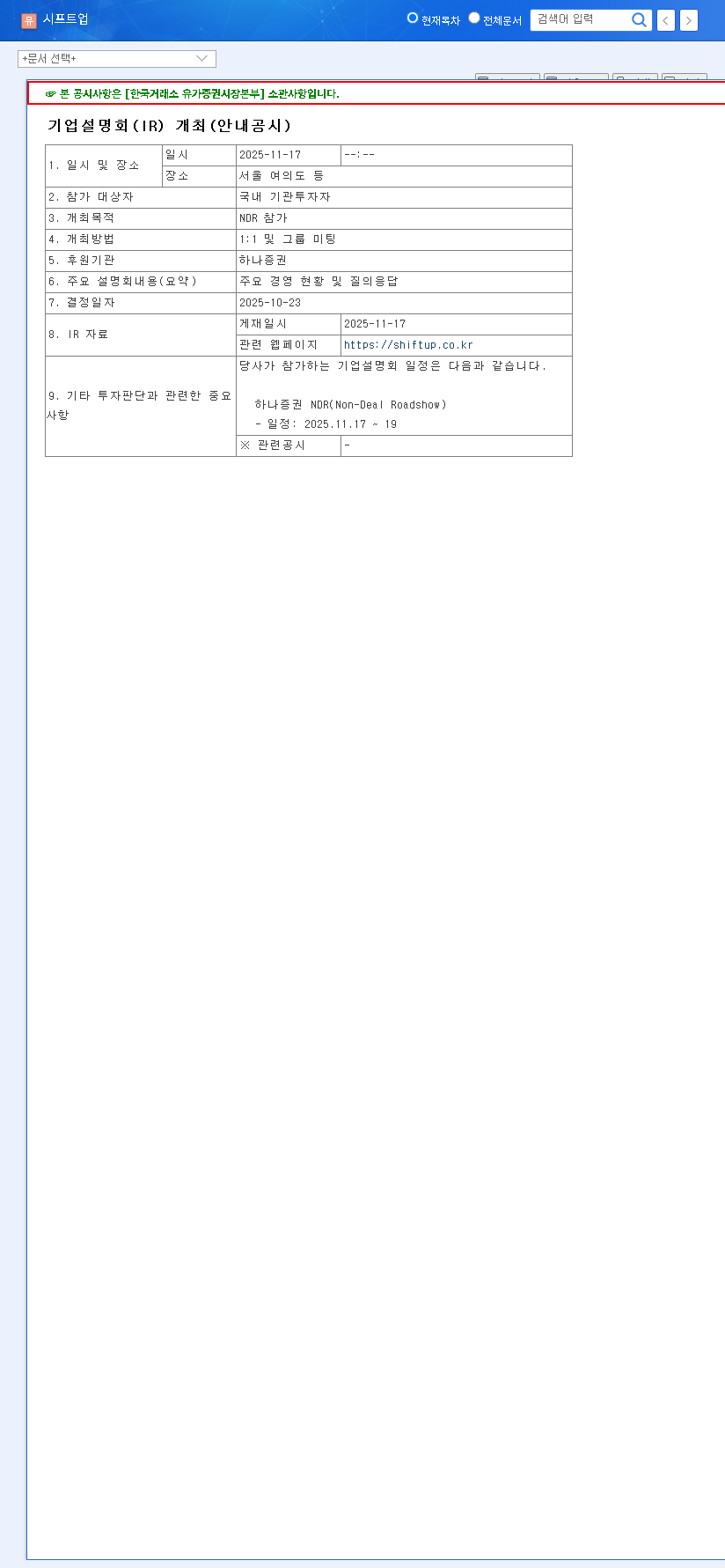

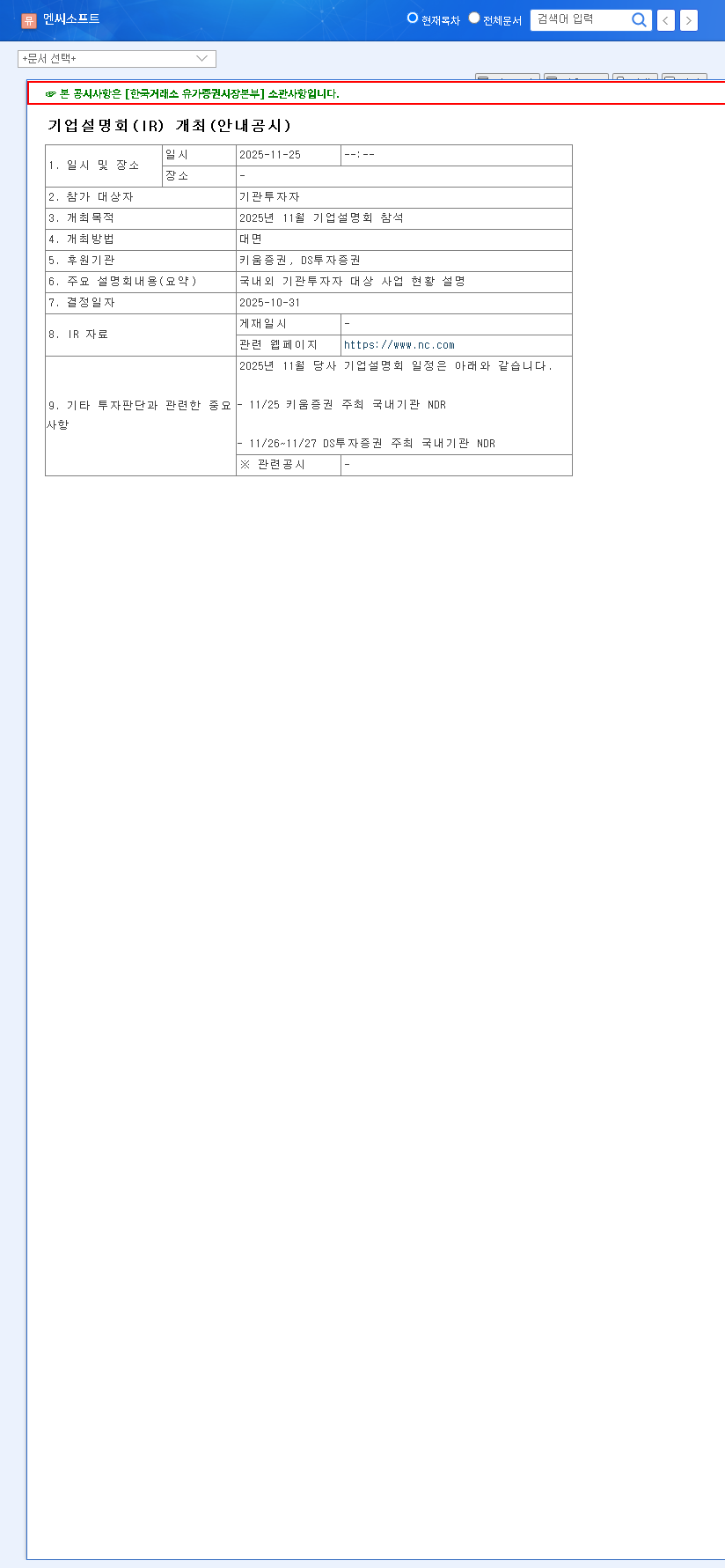

Ahead of its scheduled IR event on November 17, 2025, SEERS TECHNOLOGY released accumulated Q3 results that can only be described as extraordinary. These figures, which form the basis of their presentation to institutional investors, paint a picture of a company hitting a major inflection point. The official disclosure for this event can be viewed here: Official Disclosure.

Key Q3 2025 Financial Highlights:

- •Explosive Revenue Growth: Accumulated revenue hit KRW 27.759 billion, a staggering 1,060% increase year-over-year, primarily driven by its flagship inpatient monitoring solution, thynC™.

- •Profitability Achieved: The company successfully transitioned from a loss to an accumulated operating profit of KRW 7.624 billion, showcasing significant operational leverage and cost management.

- •Strengthened Balance Sheet: Total assets grew by 45% to KRW 40.68 trillion, and total equity rose by 42% to KRW 30.39 trillion, indicating enhanced financial stability.

- •Commitment to Innovation: R&D investment remained strong at 14.65% of revenue, signaling a continued focus on securing future growth engines and maintaining a technological edge with 124 intellectual property rights.

While the top-line growth is impressive, the 3.5x surge in accounts receivable is a critical point of concern that requires a transparent and convincing explanation during the upcoming IR event.

Analyzing the Engines of Growth

The phenomenal results from SEERS TECHNOLOGY are not accidental. They are rooted in powerful products aligned with major global healthcare trends. For more on market trends, you can read our analysis on the digital healthcare sector.

Growth Driver 1: The IoMT Platform thynC™

The star of the show is thynC™, an inpatient monitoring solution that generated KRW 23.991 billion in revenue. This platform perfectly captures the shift towards smart hospitals. As facilities seek to improve efficiency and patient outcomes, remote monitoring becomes essential. The global smart hospital market is projected by experts like Grand View Research to reach hundreds of billions of dollars, and the expansion of national health insurance coverage for such services provides a powerful tailwind for market penetration and adoption.

Growth Driver 2: mobiCARE™ and the ECG Market

While smaller, the mobiCARE™ ECG monitoring solution also contributed significantly with KRW 3.582 billion in revenue. The global ECG market is on a steady growth trajectory, with wearable patches—the company’s specialty—experiencing particularly high demand. This aligns SEERS TECHNOLOGY with another lucrative and expanding segment of the healthcare technology market.

Investor Scrutiny: Risks and The IR Litmus Test

Despite the stellar performance, investors are rightfully cautious. The upcoming IR event is a critical test of management’s transparency and ability to address lingering concerns that have weighed on the SEERS TECHNOLOGY stock price.

- •Surging Accounts Receivable: The massive jump in receivables is the biggest red flag. Management must provide a clear breakdown of their collection timeline and assure investors about cash flow health.

- •Addressing Past Issues: Past sanctions and equity method losses need to be addressed head-on, with concrete explanations of measures taken to prevent recurrence and rebuild trust.

- •Future Cost Management: Investors will want to understand the strategy for balancing aggressive R&D spending with sustainable SG&A expenses to protect future profitability.

- •Stock Price Disconnect: A compelling narrative is needed to explain how these strong fundamentals will translate into shareholder value and reverse the stock’s downward trend since its listing.

Investment Outlook: A Positive but Cautious Stance

The fundamental shift at SEERS TECHNOLOGY is undeniable. The Q3 earnings surprise and profit turnaround demonstrate a healthy, growing business. The IR event is an opportunity to amplify this positive message and build institutional confidence.

Investment Thesis: “Positive Wait-and-See”

Our outlook is cautiously optimistic. The growth potential, especially from thynC™, is significant. If management successfully allays investor fears during the IR, the stock could find a bottom and begin a new upward trend. However, the risks are real and require monitoring. Therefore, a prudent strategy is to observe the market’s reaction following the IR before making any investment decisions. Keep a close watch on institutional reports and trading volumes in the days following the event.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Investors are solely responsible for their own investment decisions.