The latest HYUNDAI HOME SHOPPING NETWORK CORPORATION earnings report for Q3 2025 presents a complex picture for investors. On the surface, the company delivered an impressive operating profit that significantly surpassed market consensus, triggering a wave of short-term optimism. However, a deeper dive into the financials reveals persistent structural headwinds and deteriorating balance sheet health that demand cautious consideration. This comprehensive analysis will unpack the recent performance, explore the underlying challenges, and provide a strategic outlook for anyone monitoring HYUNDAI HOME SHOPPING NETWORK CORPORATION stock.

Q3 2025 Earnings Highlights: A Surprising Upside

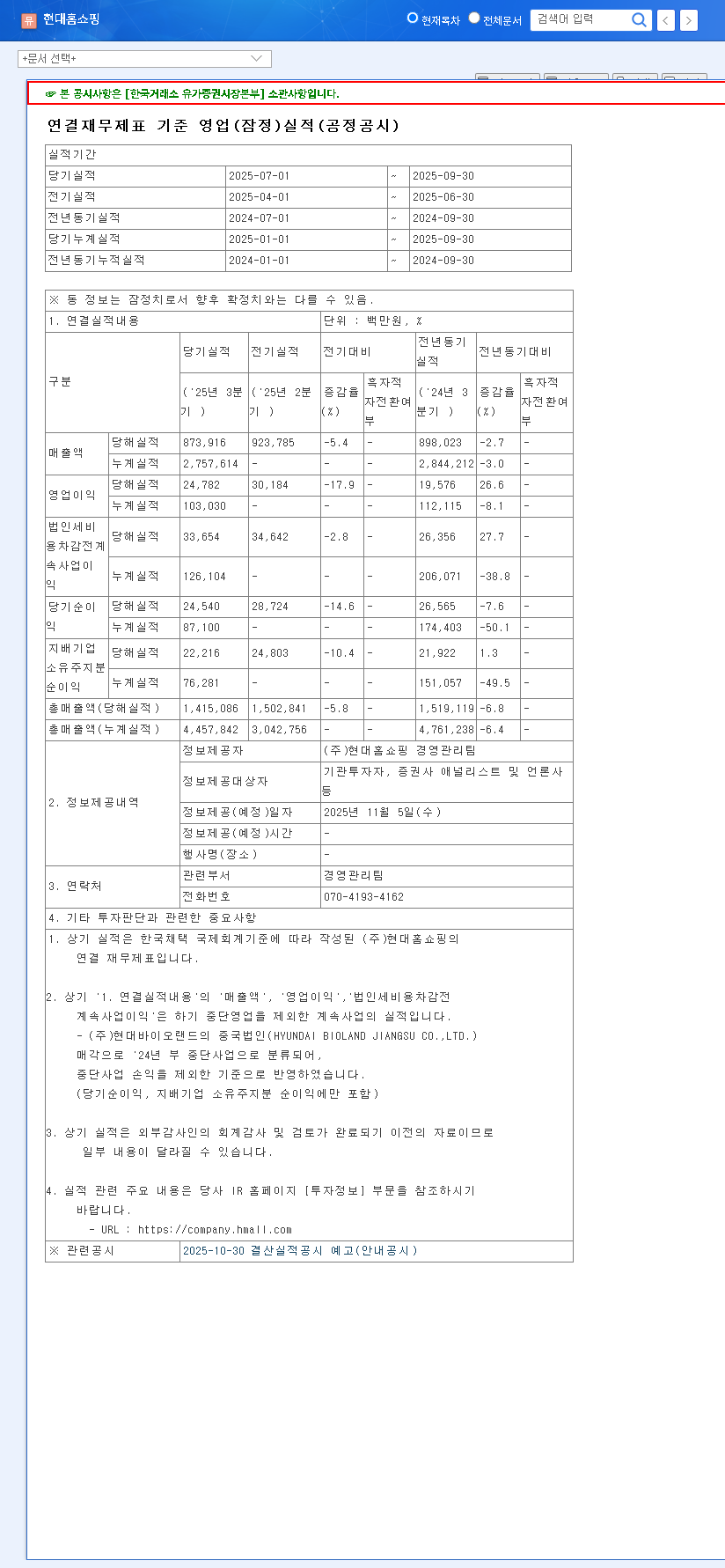

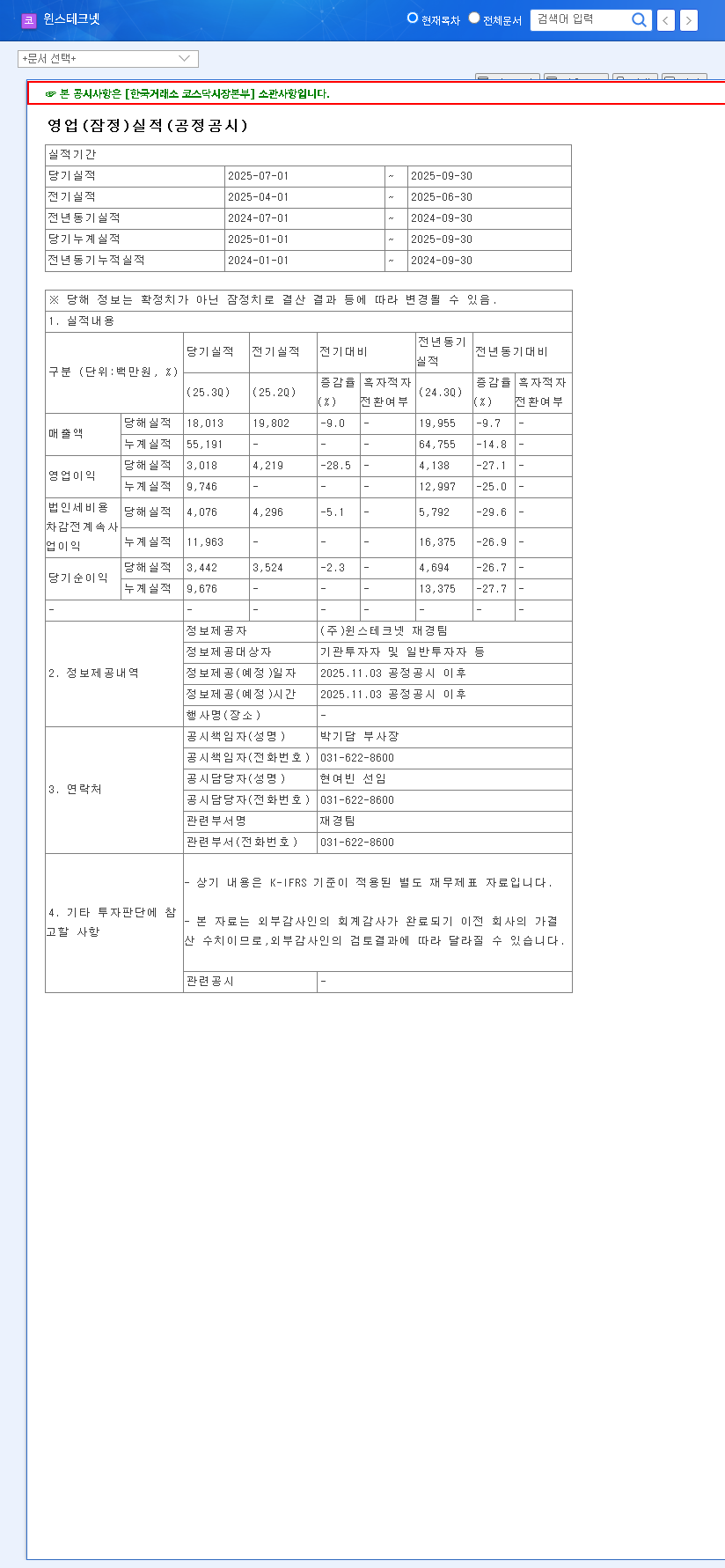

On November 5, 2025, HYUNDAI HOME SHOPPING NETWORK CORPORATION released its preliminary consolidated financial results, which caught many analysts by surprise. The numbers, based on the Official Disclosure on DART, painted a picture of resilience in profitability.

- •Revenue: KRW 873.9 billion, a marginal 0.1% above the estimate of KRW 873.0 billion.

- •Operating Profit: KRW 24.8 billion, a significant 15.3% above the estimate of KRW 21.5 billion.

- •Net Profit: KRW 22.2 billion (no consensus estimate was provided for comparison).

The key takeaway is the robust operating profit. This performance suggests that the company’s internal measures, such as stringent cost controls, supply chain optimization, or a strategic focus on higher-margin products, have been effective in defending profitability against a challenging economic backdrop.

Fundamental Analysis: Reading Between the Lines

While the headline numbers are positive, a prudent investor must look beyond a single quarter. The long-term trend for the Korean retail market, particularly for traditional players, remains a concern, and this is reflected in the company’s broader financial trajectory.

The Structural Decline in Growth

Despite this quarter’s result, the overarching narrative is one of a growth slowdown. Analysis reveals a consistent decline in both revenue and operating profit since 2022. Projections even indicate a potential shift to an operating loss for the full year of 2025. This trend points to intense competitive pressure from more agile e-commerce giants and a fundamental shift in consumer shopping behavior away from traditional home shopping channels.

The core challenge for the company is not just navigating a single quarter, but reversing a multi-year trend of declining top-line growth and shrinking margins in a rapidly evolving retail landscape.

Deteriorating Financial Health Indicators

More alarming than the growth slowdown are the red flags in the company’s financial health. The debt-to-equity ratio has been steadily rising, indicating increased reliance on borrowing. Simultaneously, the current ratio—a key measure of liquidity—has plummeted from a healthy 340.96% in 2022 to just 58.09% in 2024. This sharp drop raises serious questions about the company’s ability to meet its short-term obligations and signals potential financial instability if not addressed. For more details on how to interpret these figures, you can read our guide on Understanding Financial Health Ratios.

Macroeconomic and External Pressures

The company also operates within a challenging global economic climate. Persistently high interest rates and volatile exchange rates, particularly a strong US dollar and euro, create significant headwinds. These factors increase the cost of sourcing products from overseas and put upward pressure on import prices, which can directly erode profit margins. According to global economic reports from Reuters, these conditions are expected to persist, posing an ongoing threat to profitability.

Investor Outlook: Strategy for HYUNDAI HOME SHOPPING NETWORK CORPORATION Stock

Given the conflicting signals, how should investors approach the HYUNDAI HOME SHOPPING NETWORK CORPORATION stock? The short-term sentiment boost from the Q3 earnings beat may create a temporary rally, but a long-term investment decision must be based on the company’s ability to address its fundamental weaknesses.

Key Factors to Monitor for a Turnaround:

- •Digital Transformation: Watch for concrete progress in expanding and enhancing online and mobile commerce channels to capture a new generation of shoppers.

- •Profitability Initiatives: Look for evidence of sustainable margin improvement, not just one-off cost cuts. This could include developing high-margin private label brands or securing exclusive product deals.

- •Balance Sheet Repair: The most critical element will be a clear, actionable plan to reduce debt and improve liquidity. Any future HYUNDAI HOME SHOPPING NETWORK CORPORATION earnings call should address this directly.

In conclusion, the Q3 2025 results are a welcome, positive data point. However, they represent a battle won in a much larger, ongoing war. Until the company demonstrates a clear path to sustainable revenue growth and fortified financial health, investors should remain cautious, weighing the short-term operational wins against the significant long-term structural risks.