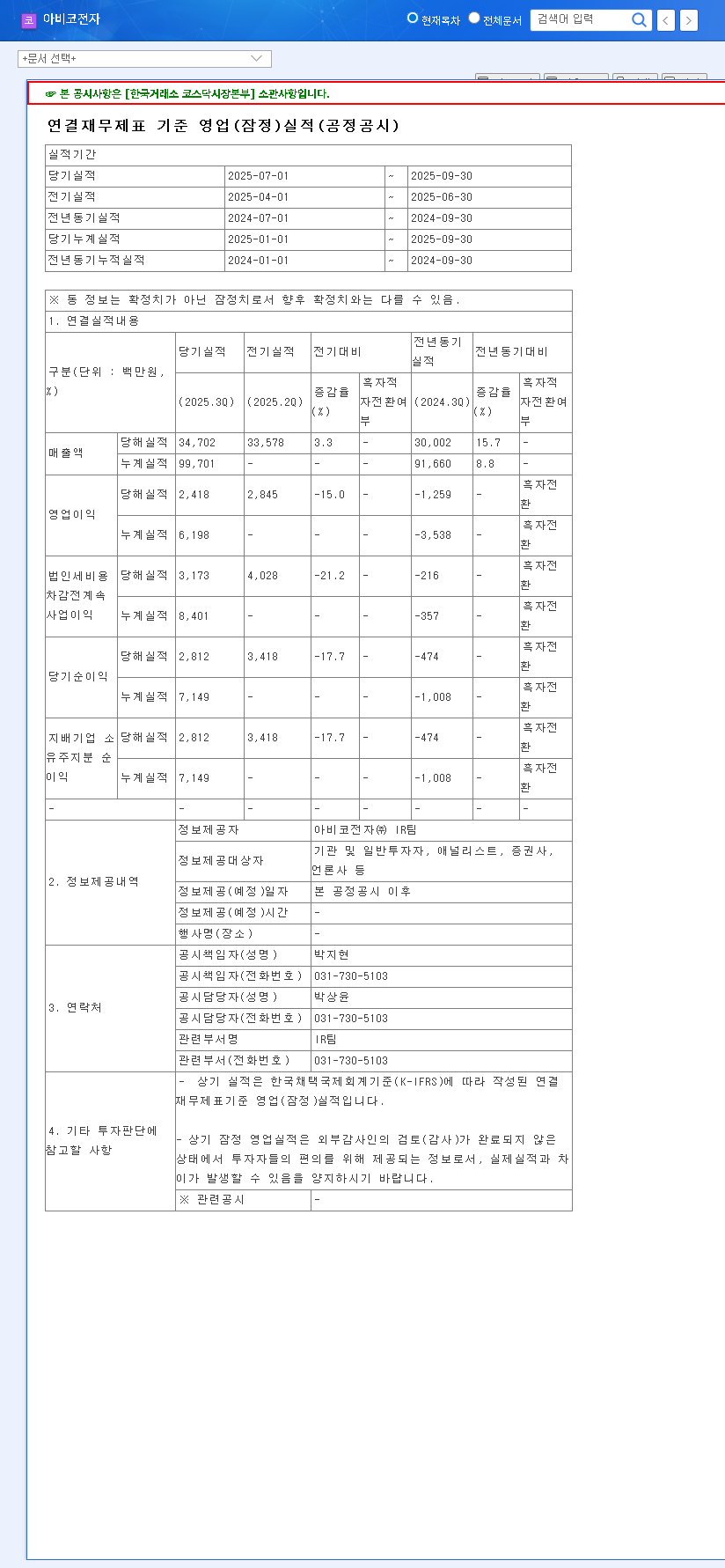

The initial analysis of the KOLON ENP Q3 2025 earnings report reveals a stunning performance that has significantly outpaced market expectations. In an economic climate fraught with uncertainty, KOLON ENP, INC. has delivered a powerful ‘earnings surprise,’ showcasing robust fundamentals and strategic prowess. This report provides a comprehensive KOLON ENP stock analysis, exploring the drivers behind this success and outlining a clear investment strategy for the future.

How did the company achieve such a monumental leap in profitability, and what does this signal for its trajectory in the rapidly evolving electric vehicle (EV) market? Let’s dissect the numbers and uncover the core strengths driving this impressive growth.

Unpacking the KOLON ENP Q3 2025 Earnings Surprise

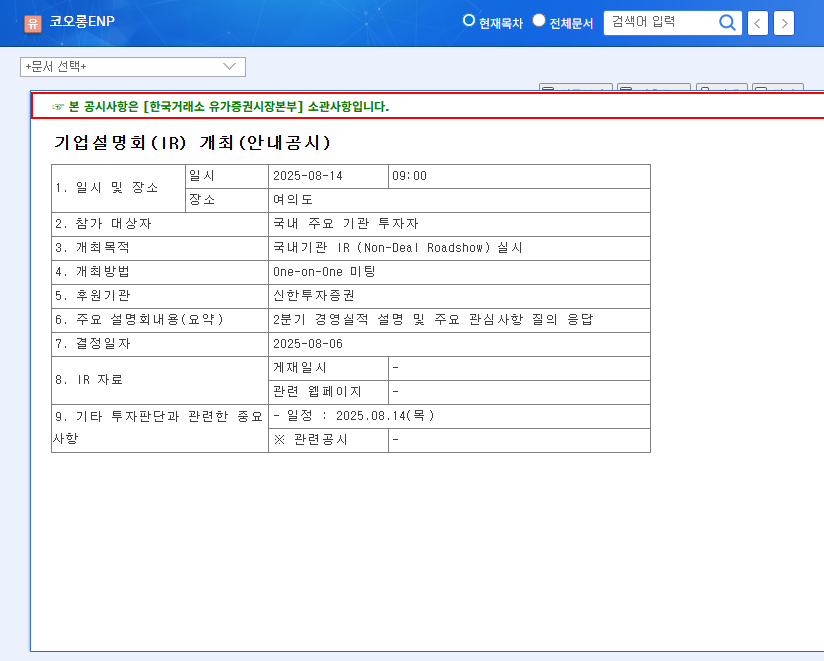

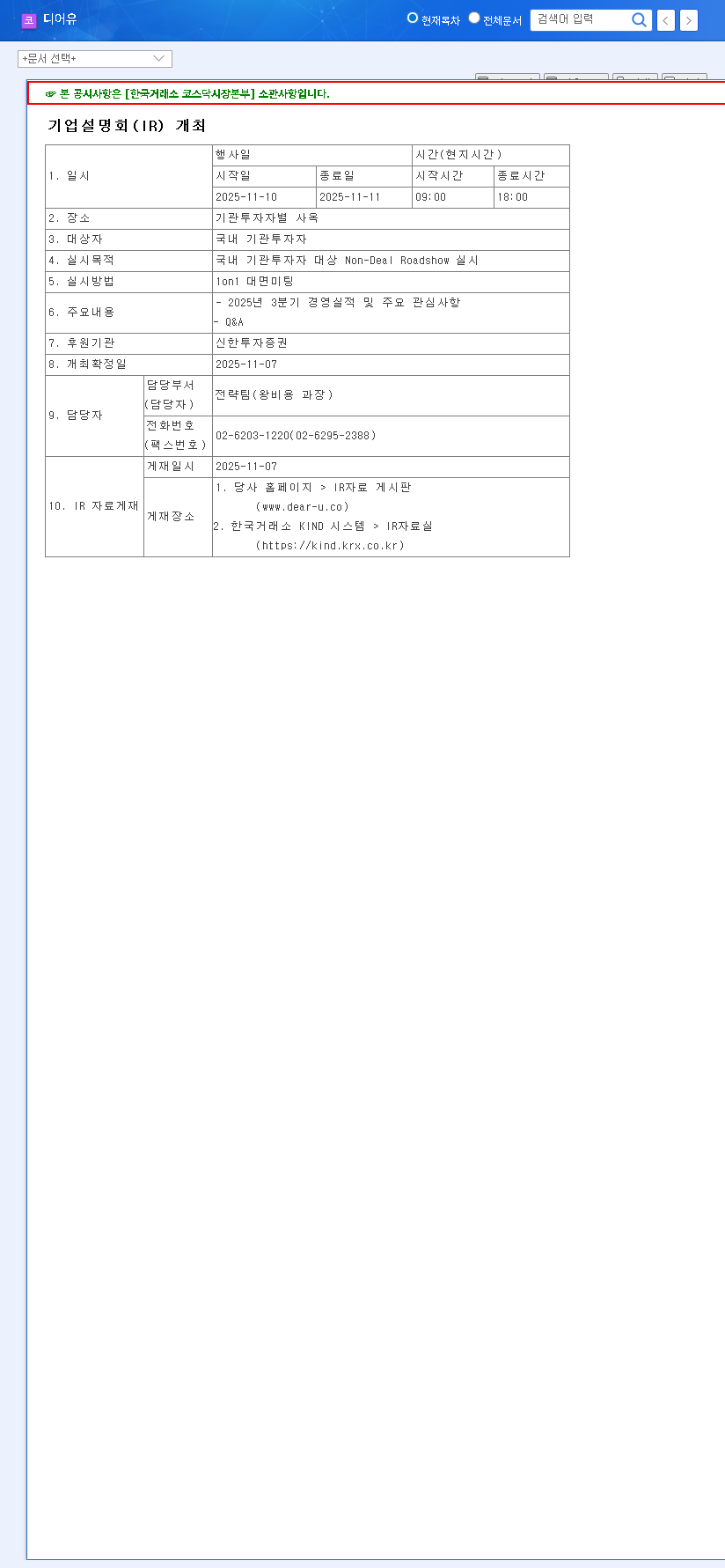

According to the preliminary results announced on November 10, 2025, and detailed in the Official Disclosure (DART), KOLON ENP’s financial health is stronger than ever. While revenue remained stable, the real story lies in the explosive growth of its profit metrics.

- •Revenue: KRW 120.2 billion (in line with KRW 119.8 billion forecast).

- •Operating Profit: KRW 13.3 billion (a massive +30% beat vs. KRW 10.2 billion forecast).

- •Net Income: KRW 13.3 billion (an astonishing +93% beat vs. KRW 6.9 billion forecast).

The staggering 93% surge in net income is the headline figure, confirming a significant ‘earnings surprise’. This result isn’t just a number; it’s a testament to the company’s high-margin business structure and astute financial management.

Strategic Excellence: The ‘Why’ Behind the Numbers

KOLON ENP’s performance transcends mere market conditions. It’s the result of a deliberate and well-executed strategy that has turned macroeconomic headwinds into tailwinds. This success is built on three core pillars.

1. Mastery of High-Margin Engineering Plastics

The 33% year-over-year growth in operating profit points directly to an enhanced product mix focused on high-margin engineering plastics. As the automotive industry shifts towards EVs, the demand for lightweight, durable, and heat-resistant materials has skyrocketed. KOLON ENP is perfectly positioned to capitalize on this trend, supplying critical components for battery systems, vehicle interiors, and structural parts. This specialization allows for premium pricing and insulates the company from the commoditized segments of the market.

2. Astute Financial and Risk Management

The company has demonstrated exceptional foresight in managing financial risks. By proactively reducing its exposure to variable-rate borrowings, it mitigated the impact of rising interest rates, leading to lower financial costs. Furthermore, with a high export ratio, KOLON ENP strategically leveraged favorable KRW/USD and KRW/EUR exchange rates in Q3, turning currency fluctuations into a competitive advantage.

3. Capitalizing on the EV Revolution

The industrial landscape is a powerful tailwind for KOLON ENP. The global push for vehicle lightweighting and the exponential growth of the EV market create sustained demand for its core products. According to market analysts at leading industry research firms, the market for automotive plastics is expected to grow significantly over the next decade. These Q3 results are a clear indicator that KOLON ENP is effectively translating this macro trend into tangible financial performance. For more information, you can read our guide on the role of advanced materials in modern manufacturing.

Investment Thesis & Stock Analysis for KOLON ENP

The KOLON ENP Q3 2025 earnings report provides a compelling case for investors. The significant outperformance in profitability is expected to act as a powerful catalyst for the stock price, reinforcing the upward momentum seen since the first half of the year.

Given the robust improvement in fundamentals, a favorable industry outlook, and strong profitability metrics, a ‘BUY’ recommendation is considered a highly effective KOLON ENP investment strategy in the near to medium term.

Key Factors for Investors to Monitor

- •Future Guidance: Watch for upward revisions to Q4 and full-year 2025 earnings forecasts from market analysts.

- •EV Market Penetration: Track new contracts and order expansion within the EV parts sector.

- •Margin Defense: Monitor the company’s ability to sustain high margins amidst raw material price volatility.

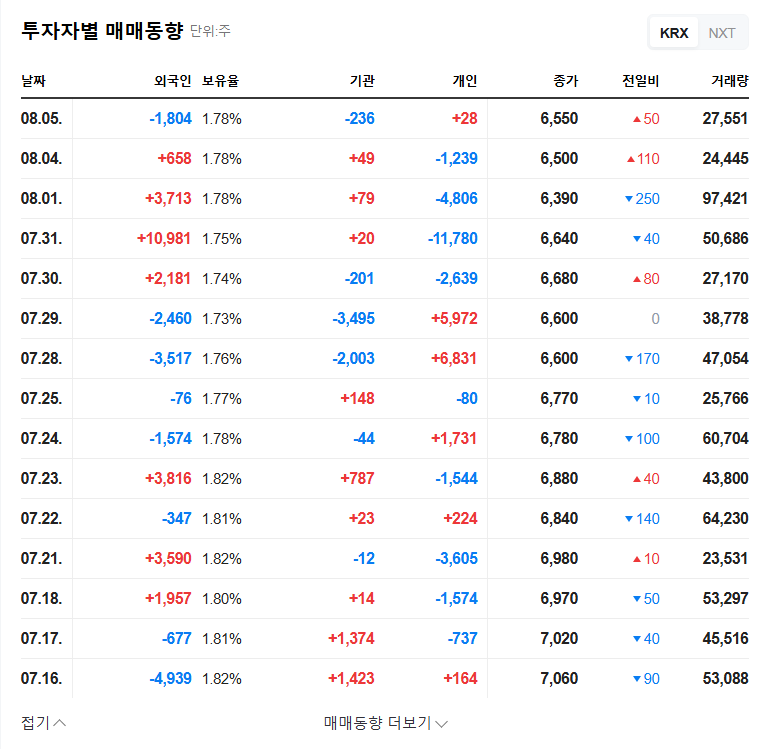

- •Investor Sentiment: Observe changes in foreign ownership, which currently sits in the low-to-mid 1% range, as a proxy for growing institutional interest.

Acknowledging Potential Risks

While the outlook is overwhelmingly positive, a prudent investment strategy must consider potential risks. These include a global economic slowdown impacting automotive demand, sharp and unforeseen spikes in raw material costs, adverse exchange rate movements, and intensified competition within the advanced materials sector.