This comprehensive analysis of the SAVEZONE I&C Corp. Q3 2025 earnings report unpacks the mixed signals sent to the market. While the headline figures reveal a sales slowdown and an operating loss, a surprising positive net income suggests a more complex story. For investors, understanding the nuances behind these numbers is paramount to assessing the company’s true value and future potential in a rapidly evolving retail landscape.

We’ll explore the core challenges facing this offline retail veteran, from weakened consumer sentiment to fierce online competition, and evaluate the sustainability of its financial stability. Is this a temporary downturn or a sign of deeper structural issues? Let’s delve into the data to formulate a clear investor action plan.

Breaking Down the SAVEZONE I&C Corp. Q3 2025 Earnings Report

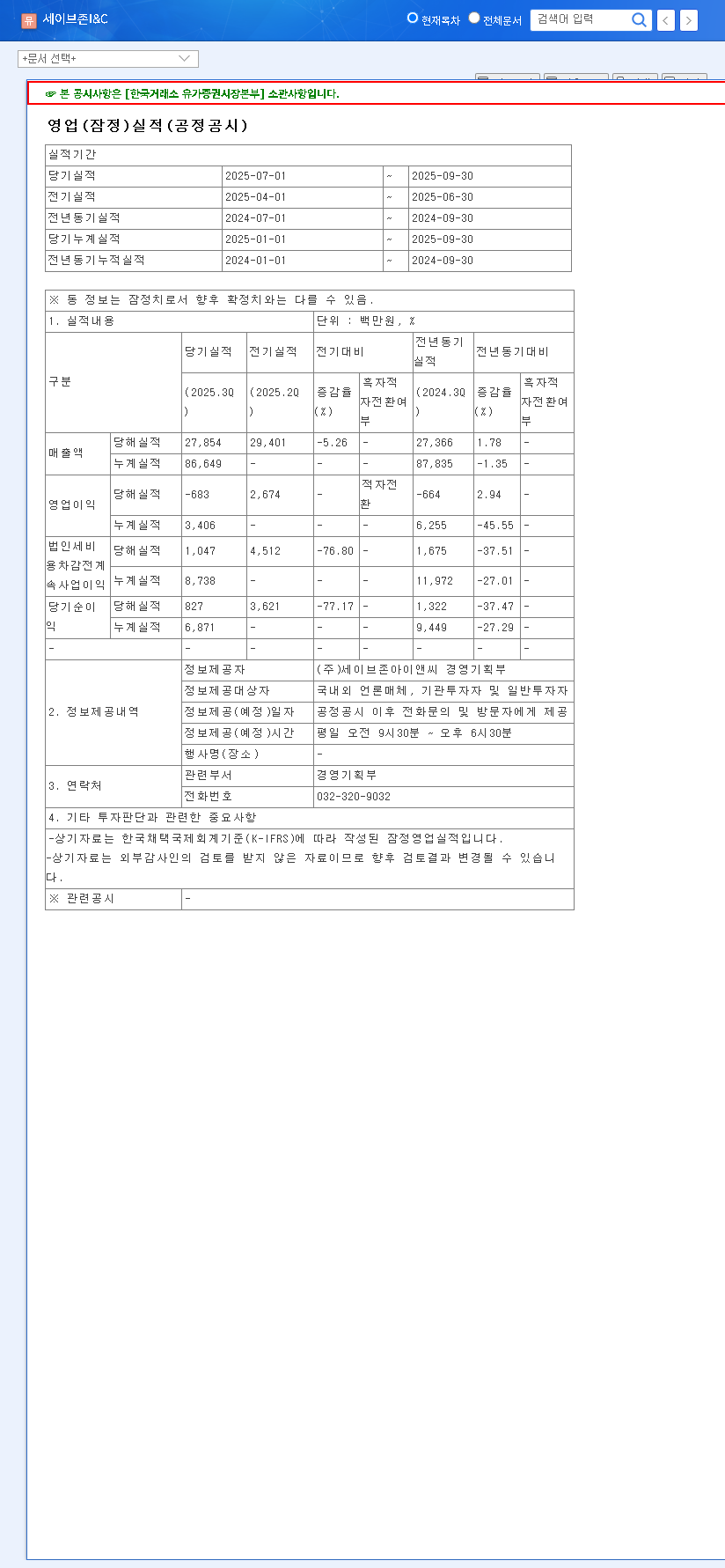

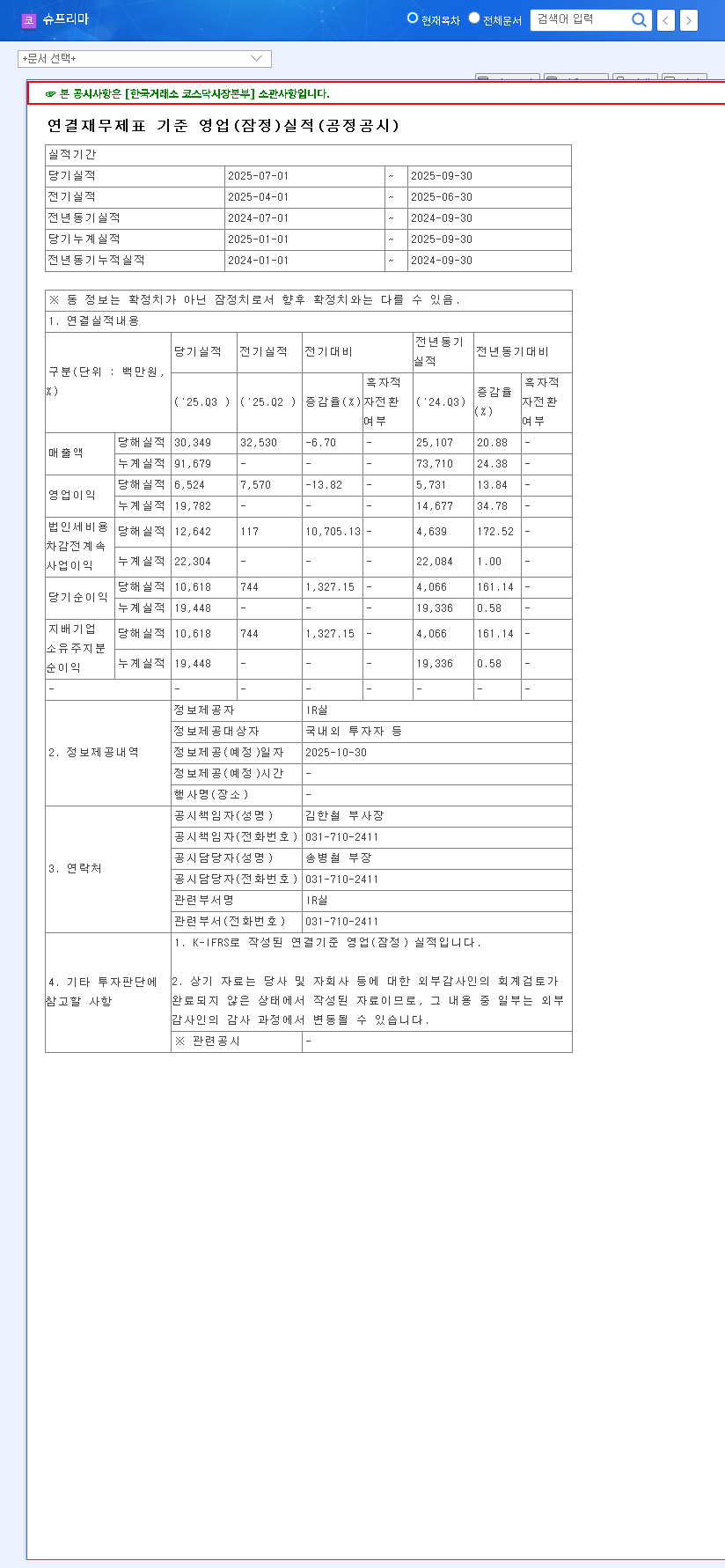

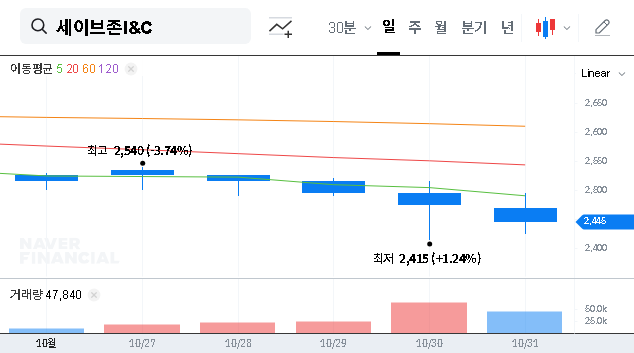

The provisional Q3 2025 results for SAVEZONE I&C Corp. presented a challenging picture for its core operations. The decline from the previous quarter highlights escalating pressures on the business. Here are the key financial metrics, as detailed in the Official Disclosure (DART).

Key Performance Indicators (Q3 2025)

- •Sales Revenue: KRW 27.9 Billion. This represents a 5.1% decrease from Q2, signaling a tangible impact from weakening consumer spending.

- •Operating Income: KRW -0.7 Billion. A significant reversal from the KRW 2.7 billion profit in Q2, this shift to an operating loss underscores deteriorating profitability in the core offline retail business.

- •Net Income: KRW 0.8 Billion. Despite the operating loss, the company remained profitable on a net basis. This paradox is key to understanding the current financial situation.

Analysis: Why the Disconnect Between Operations and Net Profit?

The divergence between a negative operating income and a positive net income can be attributed to several distinct factors—some cyclical, some structural, and some unique to SAVEZONE I&C’s financial management.

1. Macroeconomic Headwinds and Online Competition

The primary driver of the operational decline is the challenging market environment. Broad-based consumer sentiment has soured due to inflation and economic uncertainty, as reported by sources like global economic analysts. This disproportionately affects brick-and-mortar retailers like SAVEZONE I&C, particularly in discretionary spending categories like apparel and miscellaneous goods. Simultaneously, the relentless growth of e-commerce continues to siphon market share, putting immense pressure on pricing and margins.

2. The Role of Non-Operating Income

The positive net income is almost entirely due to non-operating activities. This includes items like valuation gains on financial assets (stocks, bonds, etc.) held by the company. While providing a temporary cushion, this type of income is volatile and not indicative of the core business’s health. Relying on market fluctuations rather than operational excellence is not a sustainable long-term strategy and can mask underlying weaknesses.

While a stable balance sheet is commendable, the Q3 results signal an urgent need for business model innovation. The company’s future hinges on its ability to evolve beyond traditional retail, not just manage its investment portfolio.

3. A Silver Lining: Financial Stability

A significant positive for the SAVEZONE I&C Corp. stock is its robust financial structure. With a low debt-to-equity ratio of 18.54% (as of H1 2025), the company is not burdened by heavy interest payments and has the flexibility to navigate downturns or invest in strategic initiatives. Furthermore, a history of consistent cash dividends and an 8.18% holding of treasury shares demonstrate a commitment to enhancing shareholder value, which should not be overlooked.

What’s Next? An Investor Action Plan

Given the mixed signals from the SAVEZONE I&C Corp. Q3 2025 earnings, investors should adopt a cautious yet watchful approach. The immediate market reaction may be negative, but the company’s future trajectory depends on management’s response to these challenges.

Key Strategic Imperatives for Management

- •Embrace an Omnichannel Strategy: The line between offline and online retail is gone. Integrating digital platforms with physical stores through services like ‘click-and-collect’ and ‘in-store returns for online orders’ is no longer optional; it’s essential for survival.

- •Aggressive Cost Optimization: A swift return to operating profitability requires a rigorous review of all operational costs. This includes supply chain efficiencies, store layout optimization, and energy management.

- •Differentiate the In-Store Experience: Physical stores must offer what e-commerce cannot: experience. This could mean exclusive in-store products, personalized customer service, or community events that transform stores into destinations.

For investors, the key is to monitor whether the company takes decisive action in these areas. While the stock’s valuation may seem attractive after a potential price drop, it’s crucial to distinguish between a true value opportunity and a value trap. For more on this, read our guide on How to Value Retail Stocks in a Changing Market. Vigilance and a focus on fundamental business improvements will be the key to making an informed investment decision in the coming quarters.