The ongoing saga of Winia Aid (377460) and its potential delisting from the stock market has taken a significant turn. For investors watching the suspended stock, a recent decision has provided a glimmer of hope. The Korea Exchange’s Corporate Review Committee has granted the company a 10-month improvement period, temporarily halting the immediate Winia Aid delisting threat. This decision raises a critical question: is this a genuine lifeline for a corporate turnaround, or merely a delay of the inevitable? This comprehensive analysis will explore the implications of this new development, the company’s deep-seated financial issues, and what investors should monitor over the coming months.

A Decisive Moment: The 10-Month Improvement Period

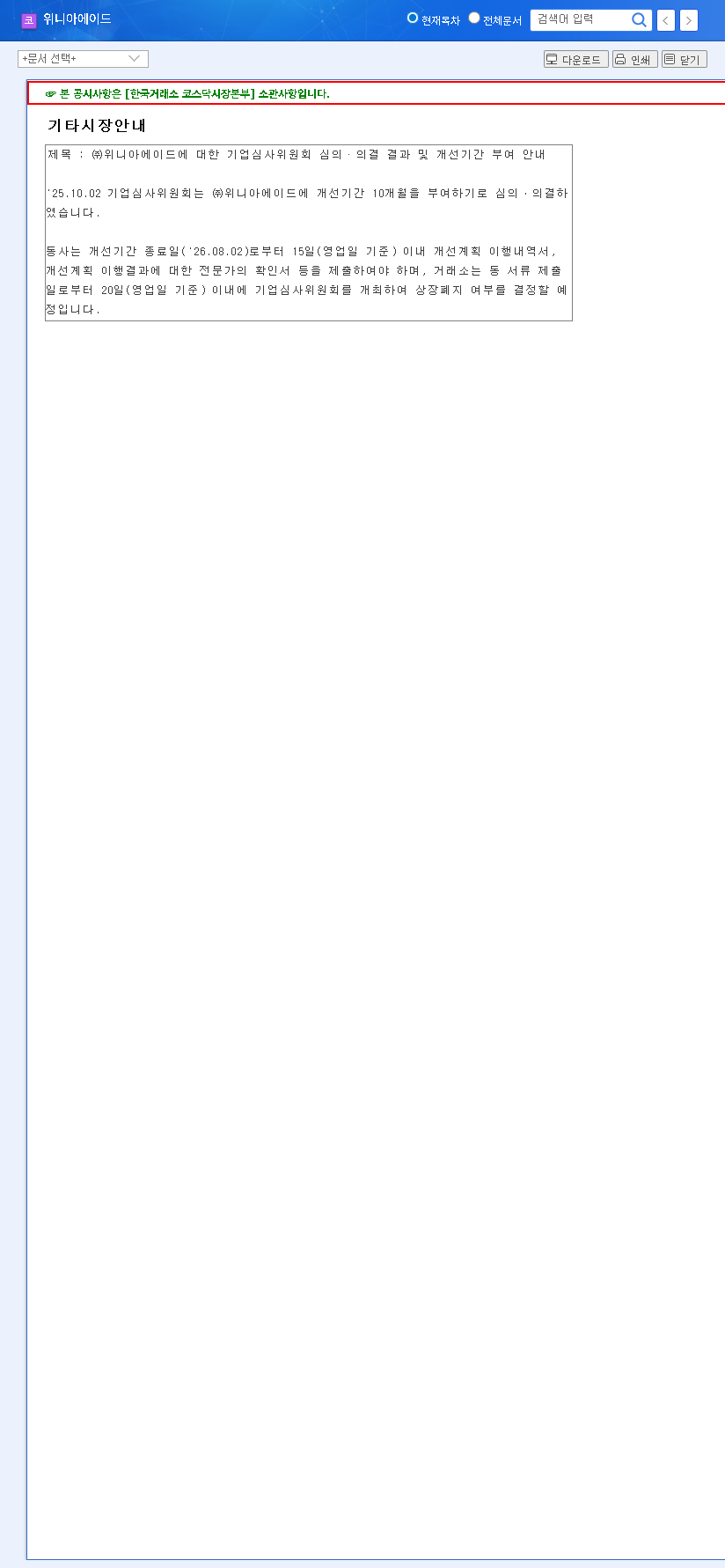

On October 2, 2025, the Korea Exchange made its long-awaited resolution. As detailed in the Official Disclosure (DART), Winia Aid was granted a crucial Winia Aid improvement period lasting 10 months. This means the company has until August 2, 2026, to implement a comprehensive recovery plan. Following this period, Winia Aid must submit a detailed report on its progress, which will be the basis for the Exchange’s final verdict on its listing status. This provides a structured path forward but keeps the stakes incredibly high.

The Core of the Crisis: Financial Deterioration and Past Failures

Understanding the Winia Aid Delisting Risk

Winia Aid’s troubles are not new. The company’s stock trading has long been suspended due to severe issues, most notably the submission of an audit report with a ‘disclaimer of opinion’. In the world of finance, this is a major red flag, indicating that auditors could not obtain sufficient evidence to form an opinion on the company’s financial statements. This, combined with persistent operational losses, pushed the Winia Aid stock to the brink of delisting.

The December 2024 business report painted a grim picture: a staggering debt-to-equity ratio of 909.2% and a fragile current ratio of just 26.1%. Sales had plummeted by 57.6% year-over-year, and the company posted a significant operating loss. These figures highlight a company in deep financial distress, making the path to recovery a monumental challenge.

Rehabilitation and a New Beginning?

In response to the crisis, Winia Aid initiated rehabilitation proceedings in late 2023. A pivotal step came in August 2025 with the confirmation of its acquisition by the UAMCO-Hyundai Rental Care consortium. This M&A process introduced new leadership and the potential for a capital injection, signaling a fundamental shift in the company’s structure. The success of this corporate rehabilitation now hinges entirely on the new management’s ability to execute a viable turnaround strategy.

The 10-month improvement period is not a guarantee of success, but rather a final opportunity. The new management’s execution over this period will be the sole determinant of Winia Aid’s future.

Investment Implications: A High-Risk, High-Stakes Scenario

For current and potential investors, the situation remains precarious. While the Winia Aid improvement period is a positive development that removes immediate delisting risk, the underlying fundamentals are still weak. The path to maintaining its listing requires tangible proof of recovery. For more information on general delisting procedures, investors can consult authoritative resources like the Korea Exchange (KRX) official guidelines.

Key Factors to Monitor

Navigating this period requires careful observation. Investors should focus on the following critical areas:

- •The Improvement Plan’s Viability: The company must present a clear, actionable plan. Vague promises won’t suffice; it needs detailed strategies for improving financial health, boosting profitability, and strengthening its core business.

- •New Management’s Performance: The UAMCO-Hyundai Rental Care consortium’s expertise will be under a microscope. Their ability to steer the company away from past failures and build a sustainable model is paramount.

- •Tangible Financial Turnaround: Monitor quarterly reports for concrete signs of improvement. Look for reduced debt, positive cash flow, and revenue growth. These metrics will be the ultimate proof of recovery.

- •Communication and Transparency: How the company communicates its progress to the market will be crucial for rebuilding trust. Regular, transparent updates are a must.

In conclusion, while the threat of an immediate Winia Aid delisting has been paused, the journey ahead is arduous. This is a chance to restart, not a guaranteed revival. For a deeper dive into the mechanics of such situations, you can read our guide on understanding corporate rehabilitation processes.

Frequently Asked Questions (FAQ)

Q1: What does the 10-month improvement period mean for Winia Aid (377460)?

It is a grace period granted by the Korea Exchange for Winia Aid to rectify the issues that led to its delisting risk. The company must execute a recovery plan to improve its financial and operational health. At the end of the period, the Exchange will review its progress to make a final decision on its listing status.

Q2: When can trading of Winia Aid stock resume?

There is no set date for trading resumption. It can only occur if Winia Aid successfully completes its improvement plan within the 10 months and the Corporate Review Committee decides to maintain its listing. Significant uncertainty remains until that final decision is made after August 2, 2026.

Q3: Is investing in Winia Aid a good idea now?

Investing in Winia Aid currently carries extremely high risk. The stock remains suspended and the possibility of delisting still exists if the turnaround fails. The improvement period is an opportunity, not a guarantee. Any investment decision should be made with extreme caution and a thorough understanding of the risks involved.