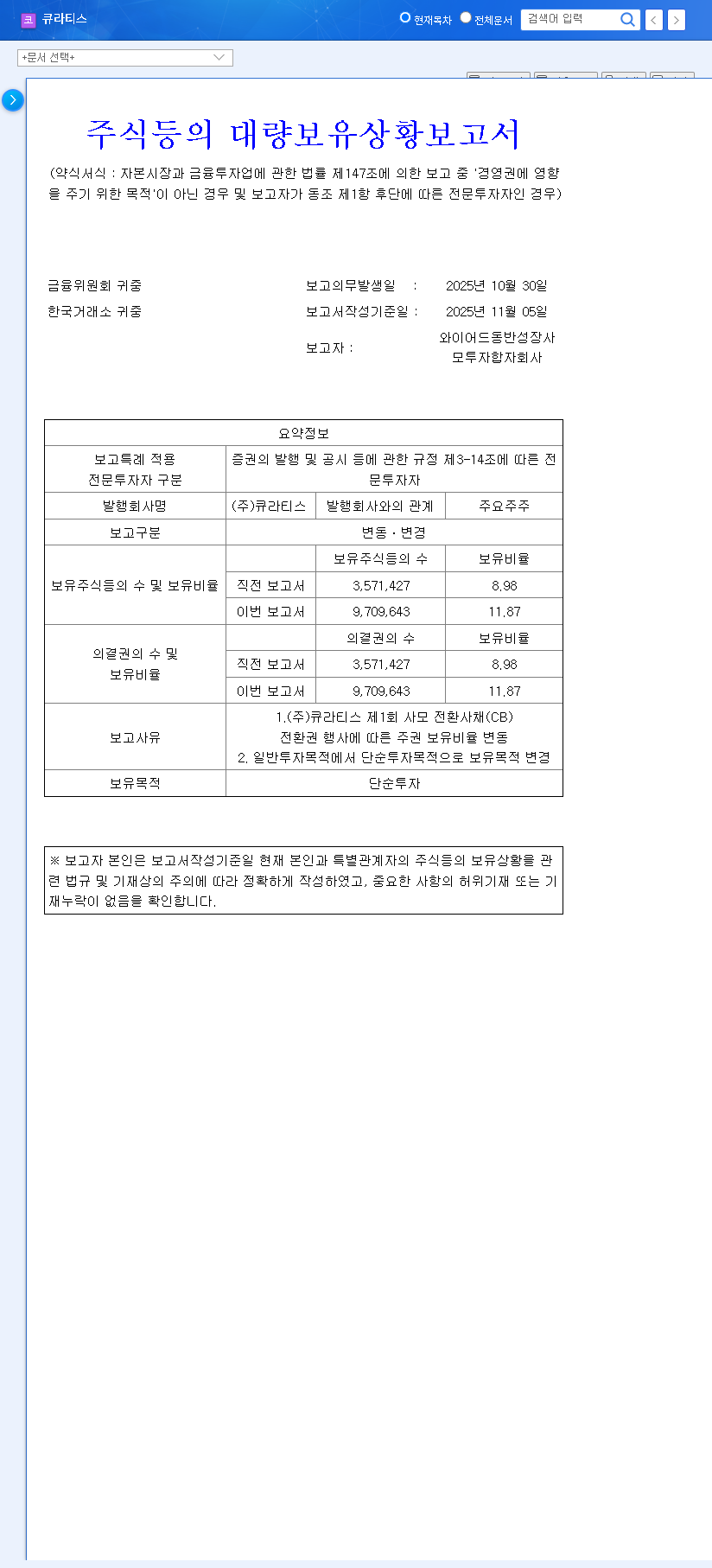

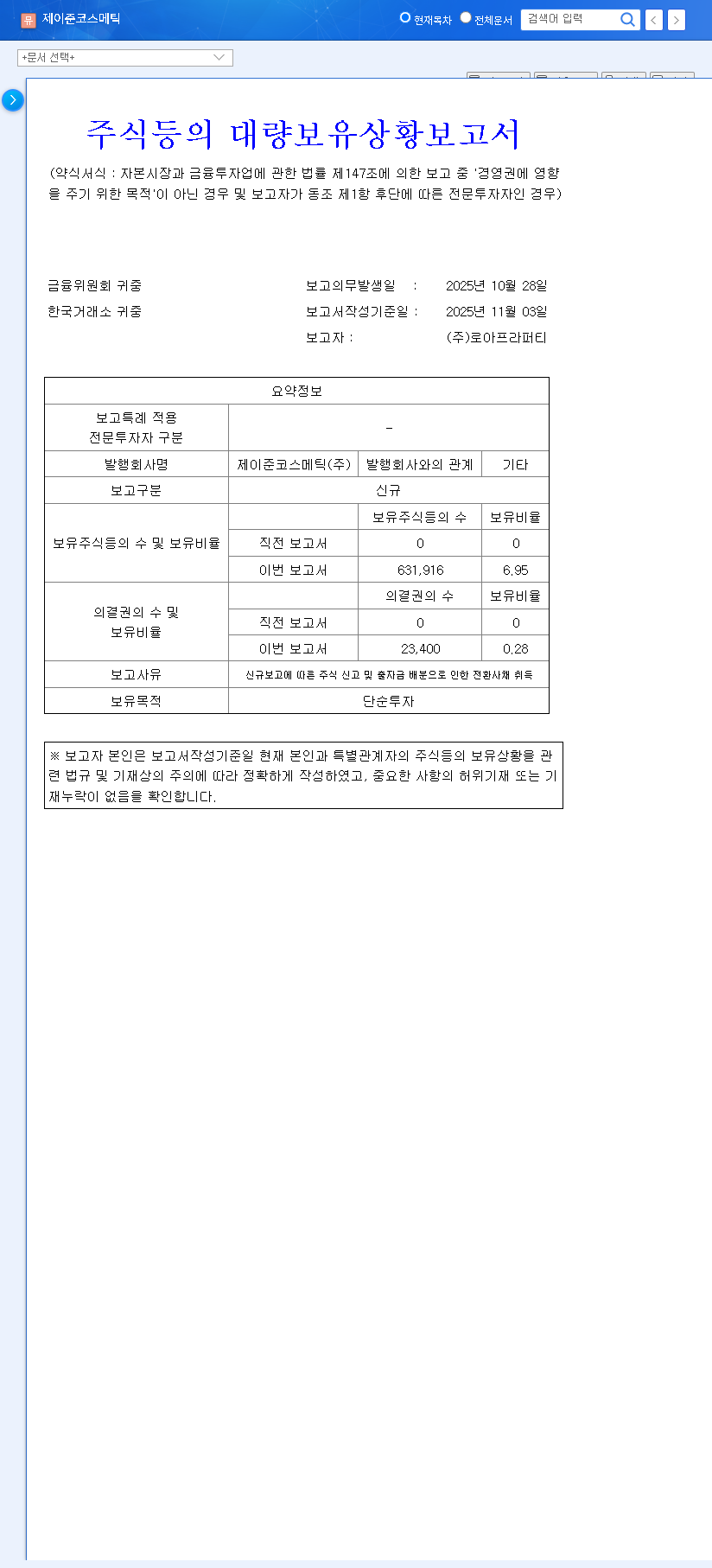

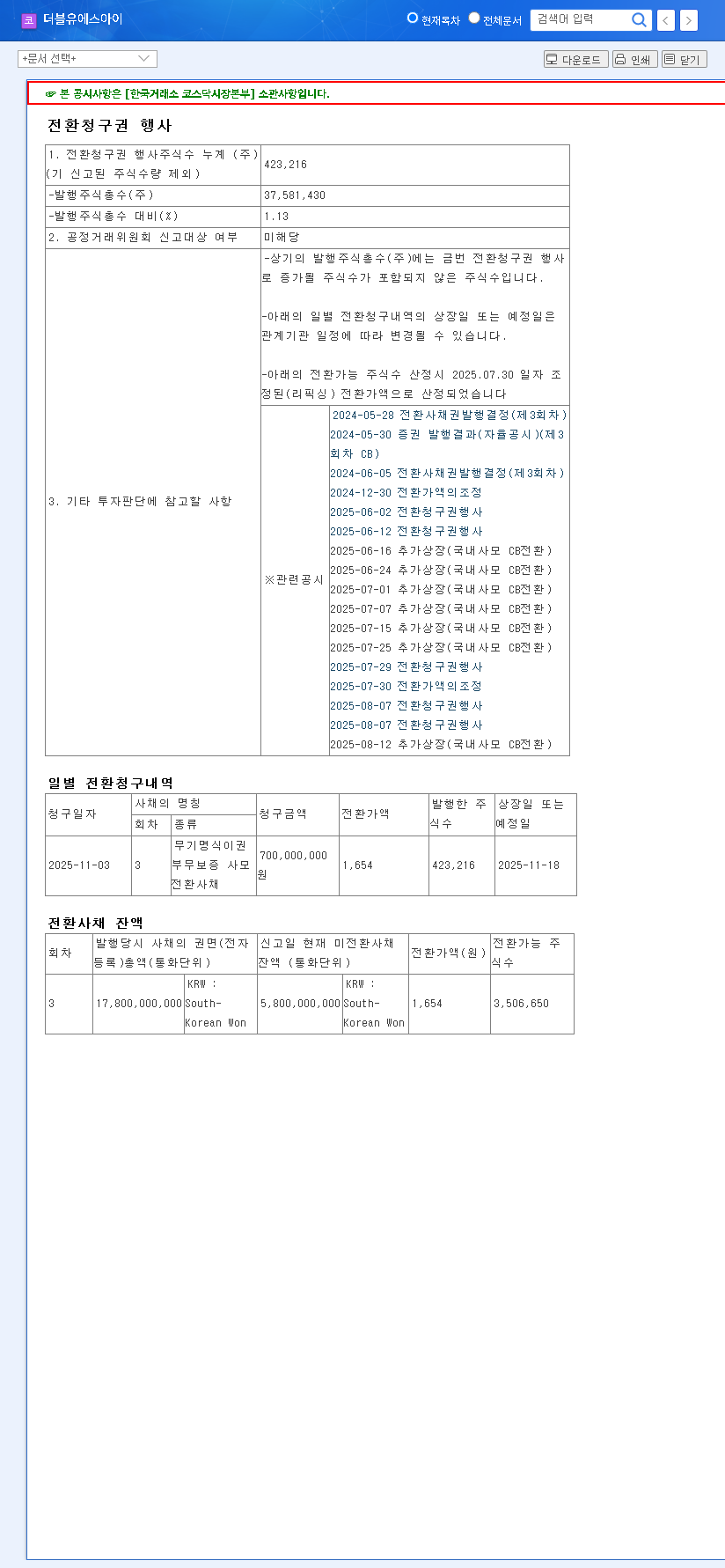

The recent Quratis CB conversion event has sent ripples through the investor community, prompting a critical re-evaluation of Quratis Inc.’s stock potential. On November 5, 2025, Wired Dongban Growth Private Equity Fund made a significant move by exercising its conversion rights on private convertible bonds (CBs), boosting its stake in the biotech firm from 8.98% to 11.87%. This action, coupled with a strategic shift in investment purpose, signals strong confidence but also raises questions about future stock volatility. For investors, understanding the nuances of this development is crucial for making informed decisions.

This comprehensive Quratis investor analysis will dissect the event, explore the company’s underlying fundamentals, and provide a strategic outlook on what this means for the Quratis stock price and your investment portfolio.

Decoding the Quratis CB Conversion Event

The core of the news revolves around a major shareholder, Wired Dongban Growth Private Equity Fund, converting its debt instrument (convertible bonds) into equity (company shares). This move is significant for two primary reasons: the substantial increase in their shareholding and the change in their stated investment purpose from ‘general investment’ to ‘simple investment’. You can view the Official Disclosure on the DART system for full transparency. This signals that the fund is not seeking to influence company management but is focused purely on the investment’s financial return, which could imply an eventual sale for profit.

What are Convertible Bonds (CBs)? In simple terms, a convertible bond is a type of debt security that the holder can convert into a specified number of shares of the issuing company’s common stock. Companies use them to raise capital at a lower interest rate, while investors are attracted by the potential for higher returns if the company’s stock price increases.

Quratis Inc. Fundamentals: A Look Under the Hood

To understand the context of the Quratis CB conversion, we must assess the company’s core business and financial health.

Promising Vaccine Pipeline

Quratis’s long-term value is heavily tied to its research and development. Key pipelines are showing steady progress:

- •QTP101 (Tuberculosis Vaccine): A next-generation vaccine for adults, a crucial area in global health, is progressing smoothly through clinical trials. Success here could tap into a significant and underserved market.

- •QTP104 (mRNA COVID-19 Vaccine): Development continues, positioning Quratis within the advanced field of mRNA technology, which has applications beyond COVID-19. You can learn more in our guide on mRNA Vaccine Technology Explained.

Stable CDMO Business Growth

Beyond its own R&D, Quratis’s Contract Development and Manufacturing Organization (CDMO) business, operating from its Osong bioplant, provides a stable revenue stream. This segment has shown consistent growth in service revenue, offering a financial cushion and validating the company’s manufacturing capabilities.

Financial Health Check

Recent rights offerings have successfully shored up the company’s balance sheet, increasing cash reserves and improving liquidity. However, a notable concern remains the surge in derivative liabilities associated with its convertible bonds. While the conversion reduces debt, the accounting for these complex financial instruments requires careful and continuous monitoring by investors.

Impact Analysis: The Road Ahead for Quratis Stock

The Quratis CB conversion introduces both opportunities and risks that could influence its stock price in the short and long term.

- •Positive Signal & Market Confidence: An institutional investor increasing its stake is a powerful vote of confidence in Quratis Inc.’s future. This can attract other investors and build positive momentum, potentially driving up the Quratis stock price.

- •Improved Financial Structure: By converting debt to equity, the company’s debt-to-equity ratio improves. This strengthens the balance sheet, making Quratis appear more financially stable and attractive to fundamentally-driven investors.

- •Risk of Short-Term Volatility: The ‘simple investment’ purpose suggests the fund may sell its shares to realize a profit if the stock price rises significantly. This potential for a large block of shares to hit the market could create downward pressure and short-term price volatility.

- •Share Dilution Concern: The creation of new shares to facilitate the conversion dilutes the ownership stake of existing shareholders. While the impact here is somewhat contained, it is a factor that can weigh on investor sentiment.

Strategic Guide for Quratis Investors

Given these factors, a prudent investment strategy is essential. The global macroeconomic environment, with shifting interest rate policies as reported by sources like Bloomberg, adds another layer of complexity. Investors should therefore align their approach with their risk tolerance and investment horizon.

For the Long-Term Investor:

Focus on the fundamentals. The success of the QTP101 and QTP104 clinical trials and the continued growth of the CDMO business are the true long-term value drivers. View the CB conversion as a positive validation of this potential but stay focused on R&D milestones and quarterly financial reports.

For the Short-Term Trader:

Be prepared for volatility. The ‘simple investment’ clause creates an overhang risk. Monitor trading volumes and be aware of potential price swings. The positive sentiment could create short-term buying opportunities, but a clear exit strategy is crucial to manage the risk of the major shareholder cashing out.

In conclusion, the Quratis CB conversion is a multifaceted event, best viewed as a bullish signal from a major institutional investor. It strengthens the company’s financial standing and boosts confidence. However, investors must remain vigilant, monitoring for short-term volatility while keeping a close eye on the fundamental progress that will ultimately determine the long-term success of Quratis Inc.